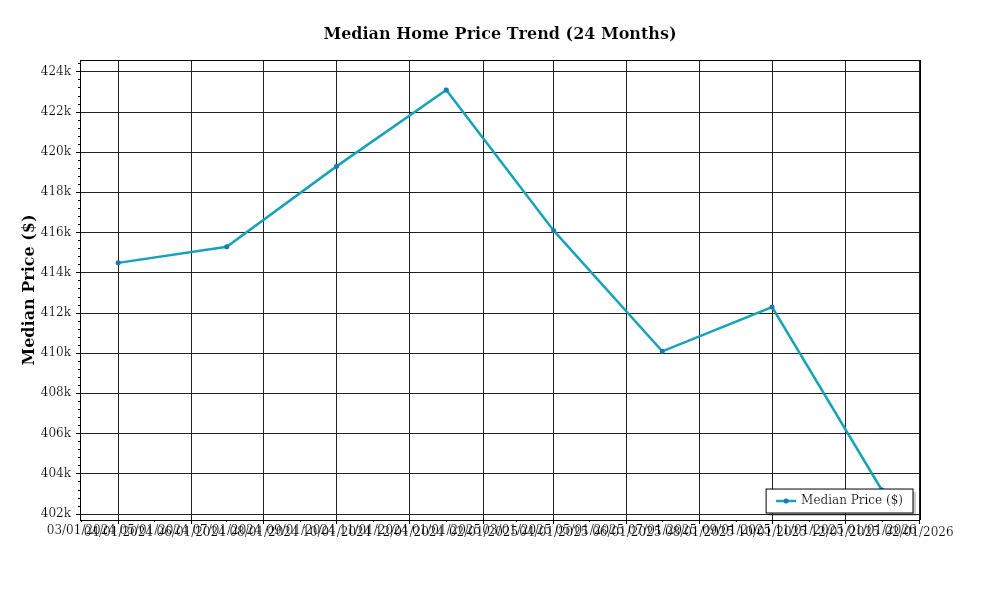

Investor Market Analysis – 2026-05-21

Key Considerations for Investors Fix-and-flip strategies: Set a maximum holding cost threshold of 10% of the expected sale price to safeguard profit margins.

Investor Market Analysis – 2026-05-20

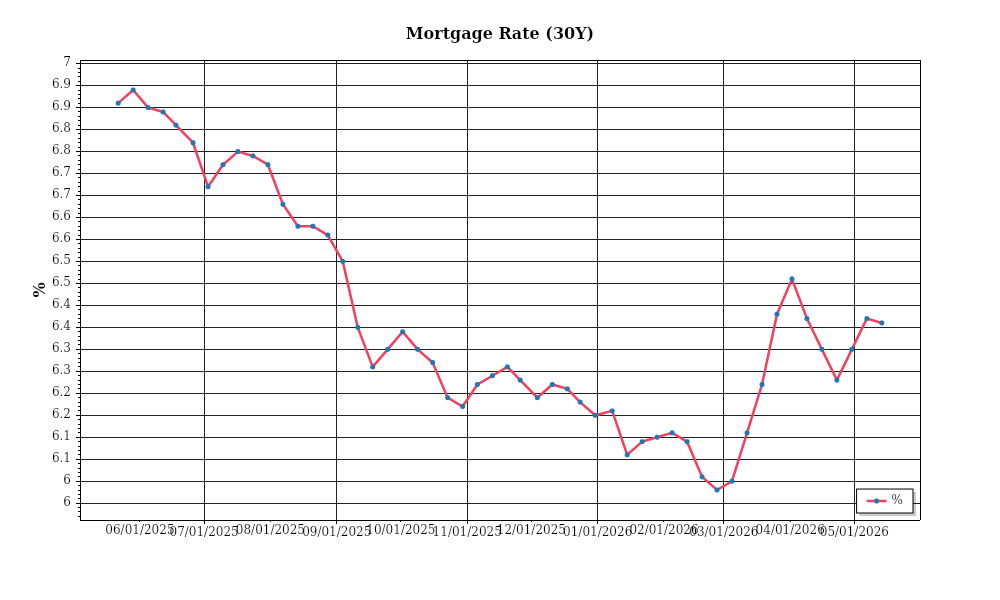

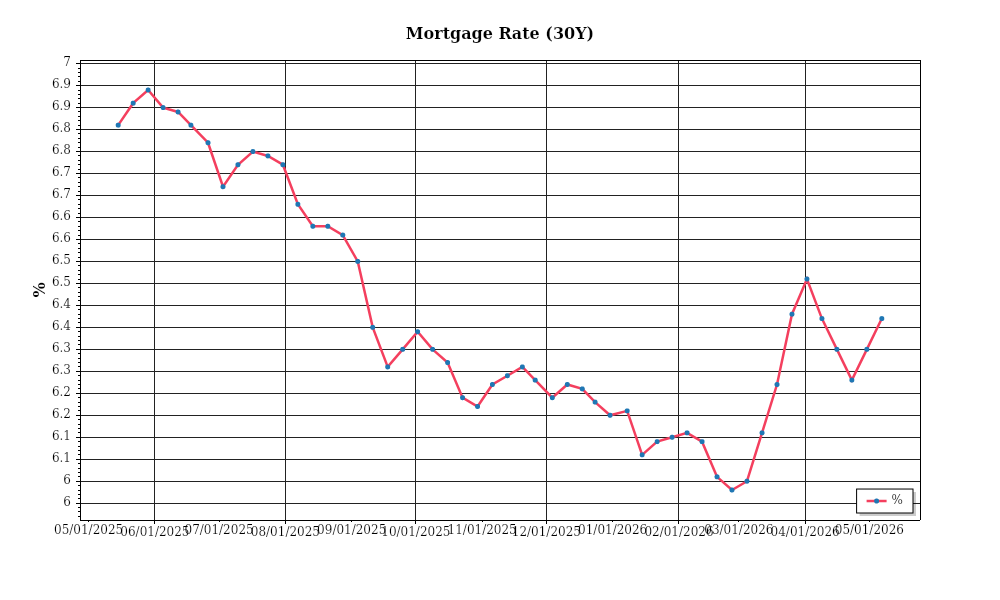

With interest rates hovering around 5.5% for conventional loans, this high-rate environment places pressure on DSCR calculations, making it more…

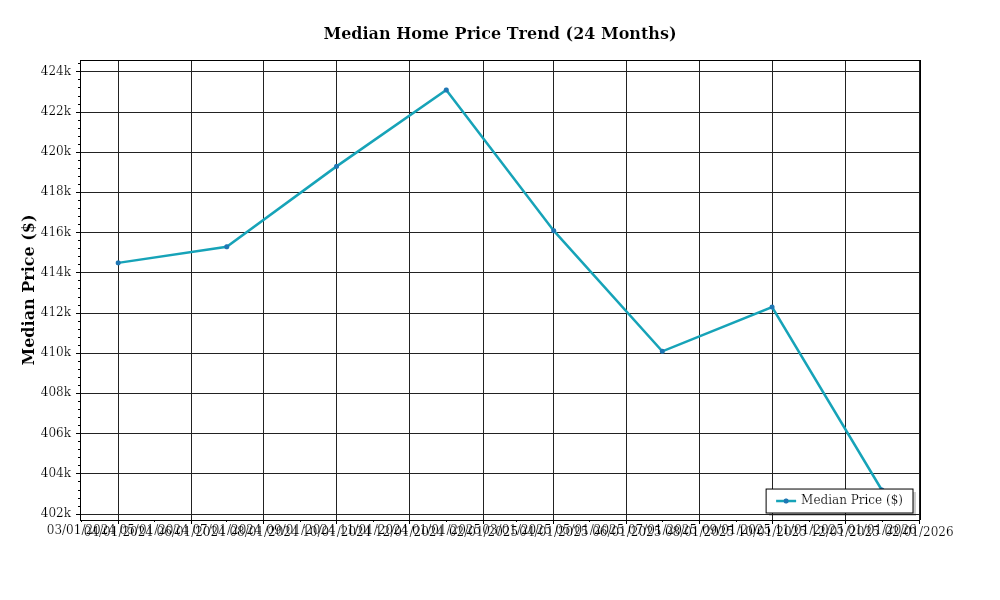

Investor Market Analysis – 2026-05-19

Key Considerations for Investors – **Fix-and-flip strategies**: Secure properties with at least a 20% spread between purchase price and projected sale…

Investor Market Analysis – 2026-05-18

The mortgage-treasury spread, a critical indicator of lender risk perception, is currently at 1.4% , down from 1.8% just three months ago.

Investor Market Analysis – 2026-05-17

Currently, the spread between the 30-year fixed mortgage rate and the 10-year Treasury yield is approximately 2.0% , a slight contraction from 2.

Investor Market Analysis – 2026-05-16

As of May 2026, the spread between the 30-year fixed mortgage rate and the 10-year treasury yield is approximately 2.0% .

Investor Market Analysis – 2026-05-15

The mortgage-treasury spread, which has been a critical indicator of lender risk perception, currently stands at 1.3%…

Investor Market Analysis – 2026-05-13

Currently, the spread between the 30-year fixed mortgage rate and the 10-year Treasury yield is at 2.25%…

Investor Market Analysis – 2026-05-12

Treasury yields has recently widened to 2.3% , up from 2.0% earlier in the…

Investor Market Analysis – 2026-05-11

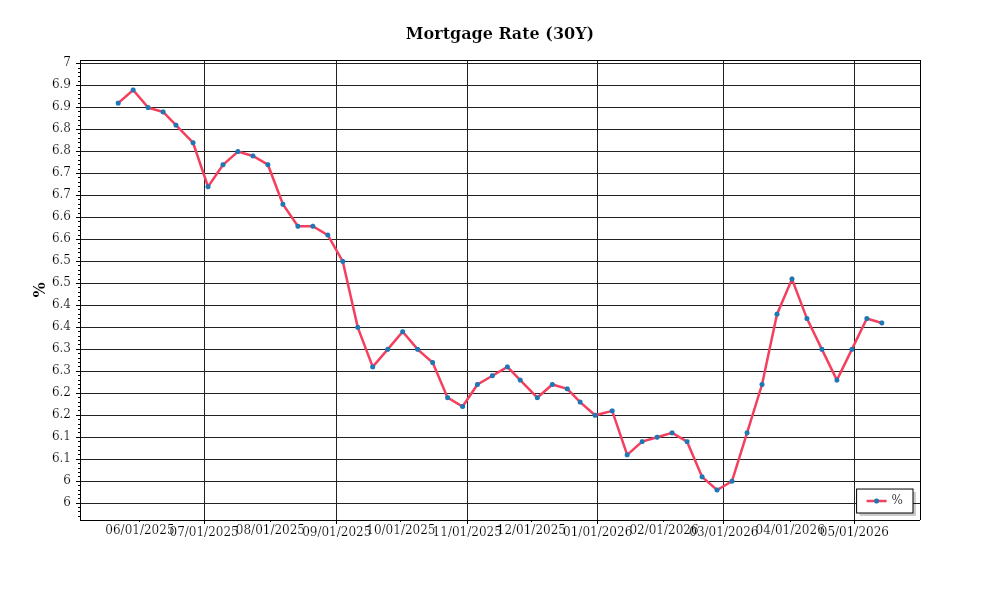

Key Considerations for Investors For fix-and-flip strategies , aim for a minimum spread of 20% between acquisition and after-repair values to accommodate…