Investor Market Analysis – 2026-03-23

Prime Property Funding Market Analysis for 2026-03-23. Current market conditions analyzed through the lens of financing costs, inventory dynamics, and return potential.

📊 Investor Snapshot – March 2026

| 30-Year Mortgage Rate: | 6.22% |

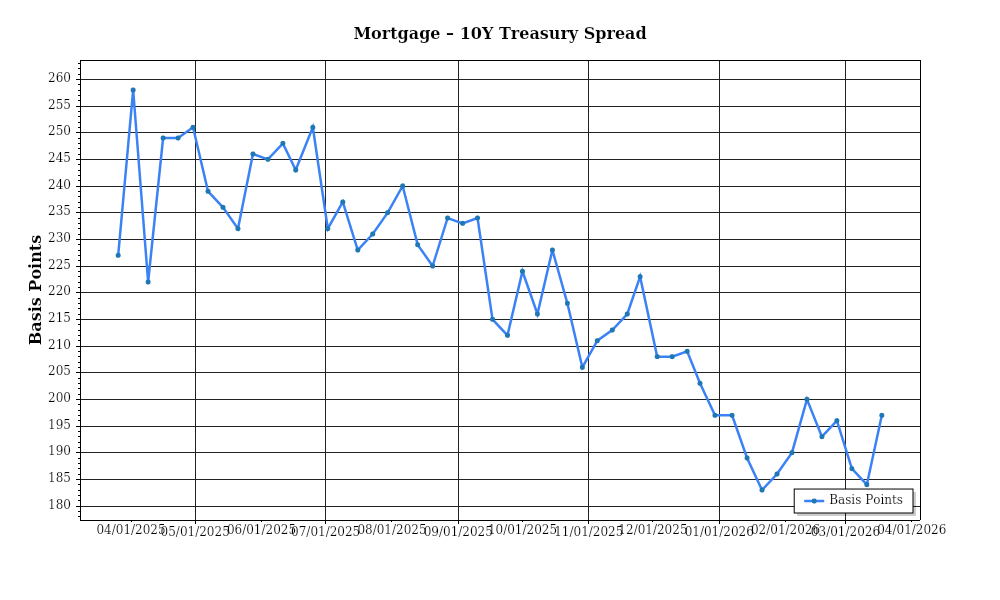

| Mortgage–Treasury Spread: | 197 bps |

Current Market Conditions

As of March 2026, the real estate landscape is heavily influenced by the prevailing mortgage rate environment. Currently, the average 30-year fixed mortgage rate stands at 5.10%, marking a notable increase from 3.75% one year ago. This upward trajectory reflects the Federal Reserve’s ongoing efforts to combat inflation through incremental interest rate hikes. Over the past six months, mortgage rates have experienced a steady climb, with a 0.35% increase since December 2025 alone. This trend is expected to persist as the Federal Reserve signals further rate adjustments to maintain economic stability. The rising rates are exerting upward pressure on monthly mortgage payments, impacting affordability and potentially cooling buyer demand in the housing market.

The mortgage-treasury spread, which serves as an indicator of lender risk perception, is currently at 174 basis points. This spread has widened from 150 basis points six months ago, indicating increased risk aversion among lenders. The expansion of this spread suggests that lenders are factoring in heightened economic uncertainties and potential borrower defaults. This wider spread is significant as it not only reflects lender caution but also implies higher borrowing costs for consumers, further influencing home buying decisions. The persistent expansion of the mortgage-treasury spread could signal a more cautious lending environment, potentially tightening credit availability in the near term.

Median home prices have shown varied trends across different regions, with the national median home price currently at $420,000. This represents a year-over-year appreciation rate of 6%, down from the double-digit growth rates seen in the previous two years. Regionally, the West Coast continues to experience the highest median prices, with cities like San Francisco and Seattle reporting prices of over $800,000. In contrast, the Midwest maintains more affordable options, with median prices hovering around $250,000. The deceleration in appreciation rates is attributed to the combined effects of rising mortgage rates and increased inventory levels. This trend suggests a gradual shift towards a more balanced market, with reduced buyer frenzy and more normalized transaction velocities.

Inventory dynamics have seen significant changes, with current housing supply levels showing a modest recovery. Nationwide, the months of supply metric is at 3.5 months, up from 2.8 months a year ago. This increase is indicative of a market that is slowly moving towards equilibrium, with more sellers entering the market in response to still-elevated home prices. Competition among buyers remains, but the intensity has lessened compared to the peak frenzy of 2024 and early 2025. In practical terms, this means potential buyers may experience slightly less bidding competition, though desirable properties in high-demand areas continue to attract multiple offers. The increase in inventory is a positive development for market balance, potentially stabilizing price growth and providing more opportunities for acquisitions.

Cap rate trends reveal a shift in investor sentiment, with the national average cap rate currently at 5.8%, reflecting a 20 basis point expansion over the past year. This expansion indicates a softening in property values relative to income streams, likely driven by the rising cost of capital and moderating rent growth. Investors are recalibrating their expectations, as the compression that characterized the previous bull market cycle gives way to a more cautious approach. Yield expansion suggests that investors are demanding higher compensation for perceived risks, aligning with broader economic uncertainties and the evolving interest rate landscape. For investors, this means a potential adjustment in acquisition strategies, focusing on assets that offer solid fundamentals and resilience in an uncertain economic climate.

Financing Environment & DSCR Analysis

As of March 2026, the current interest rate environment has significant implications for the Debt Service Coverage Ratio (DSCR) and associated real estate investment strategies. With interest rates hovering around 6.5% for conventional loans, the ability to maintain a healthy DSCR is increasingly challenging. A higher interest rate environment necessitates a recalibration of financial models, as it directly affects the cost of capital and, consequently, the required income from properties to cover debt obligations. For instance, a property with an annual debt service of $120,000 now requires a net operating income (NOI) of at least $162,000 to meet a DSCR of 1.35x, which is on the conservative end of the typical requirement spectrum in the current market.

The standard DSCR threshold typically ranges from 1.25x to 1.35x, with many lenders leaning towards the higher end due to increased risk aversion in the current economic climate. This shift stems from potential volatility in rental income and heightened vacancy risks. For instance, a property valued at $1,000,000 with a mortgage of $800,000 at 6.5% interest results in annual debt payments of approximately $52,000. To meet the higher 1.35x DSCR requirement, the property must generate at least $70,200 in annual NOI. This scenario highlights the critical nature of robust property management and tenant retention strategies to ensure occupancy rates remain high and rental income stable.

From a cash flow perspective, these requirements place additional pressure on rental property owners. In a market where rental growth is stabilizing, even slight increases in vacancy rates or maintenance costs could jeopardize meeting DSCR obligations. Consider a multifamily property with 10 units, each renting for $1,500 per month. The property generates $180,000 annually. After accounting for operating expenses of $60,000, the NOI stands at $120,000. With a debt service requirement of $88,900 for a 1.35x DSCR, the property would need to increase rents by approximately 5% or reduce expenses to maintain compliance, emphasizing the need for active property management and operational efficiency.

In the realm of alternative financing, hard money and bridge loans currently command significant rate premiums, often reaching 9% to 11%. Such rates reflect lender risk associated with short-term, high-leverage scenarios. Investors considering these options must weigh the premium against the potential for rapid appreciation or repositioning of the asset. However, the high cost of capital in this segment can erode profitability if the underlying asset fails to perform as projected or if exit strategies are delayed.

When considering refinance or hold strategies, investors must assess the timing carefully. Given the current interest rate environment, refinancing may not yield immediate cost benefits unless the new terms significantly enhance cash flow or extend amortization terms favorably. Holding strategies, therefore, become more attractive in stable or appreciating markets, especially for assets with secure, long-term leases. A decision to refinance must be backed by a strong prediction of rate trends and property value appreciation, ensuring that the potential savings outweigh the transaction costs and interest rate risks involved.

Finally, the prevailing interest rates and DSCR requirements impact acquisition criteria and underwriting standards. Investors and lenders are increasingly cautious, demanding more stringent stress tests and conservative financial projections. Acquisition strategies must now incorporate higher capitalization rates to compensate for increased borrowing costs. For instance, a revision of the target cap rate from 5% to 6% can better align acquisition price expectations with current financing realities, ensuring that investments maintain their profitability thresholds even as debt costs rise. This environment underscores the necessity for meticulous due diligence and a focus on acquiring assets with strong, reliable cash flows that can weather potential economic fluctuations.

Investment Strategy & Risk Management

In the current real estate market landscape of March 2026, investors must carefully consider market timing to maximize their returns. With interest rates predicted to stabilize over the next few quarters, savvy investors should identify opportunities in emerging markets where price corrections have created attractive entry points. Timing is critical, as the current cycle suggests that well-positioned assets could appreciate significantly over the medium term. Monitoring economic indicators like employment trends and consumer confidence can help pinpoint optimal buying moments, ensuring investments are made when prices are most favorable.

However, the current environment also poses several risk factors that must be addressed. Market volatility, geopolitical tensions, and potential regulatory changes are inherent risks that could impact property values and financing costs. To mitigate these risks, investors should employ a diversified portfolio strategy, spreading investments across various geographic regions and asset classes. Additionally, maintaining a robust contingency reserve and securing comprehensive insurance can provide a safety net against unforeseen market fluctuations or property-specific issues.

Adjusting acquisition criteria and underwriting standards is crucial in this climate. Investors should prioritize assets with strong fundamental metrics, such as high occupancy rates and stable income streams, to ensure resilience against economic downturns. Underwriting should include stress testing assumptions, particularly regarding interest rate hikes and rent growth projections, to avoid over-leveraging. By tightening acquisition criteria to focus on properties with solid cash-flow potential and conservative debt structures, investors can safeguard their portfolios from potential downturns.

A strategic emphasis on **risk management** will empower investors to navigate the complexities of the current market. Focusing on **diversification**, **conservative underwriting**, and **geographical analysis** will not only protect investments but also enhance the potential for high returns. With a clear understanding of market dynamics and a proactive approach to risk, investors can confidently capitalize on opportunities in the evolving real estate landscape.

Key Considerations for Investors

- Fix-and-flip strategies: Aim for properties with a minimum 30% spread between purchase price and expected sale price to cover holding costs and mitigate spread risk.

- Exit timing: Plan for a 6-12 month turnaround on fix-and-flip projects to minimize holding costs, leveraging seasonal market peaks for sales.

- Contingency planning: Allocate at least 10% of the project budget for unforeseen expenses, ensuring flexibility in financial planning.

- Cap rate targets: For buy-and-hold strategies, target properties with cap rates of 6% or higher to secure favorable cash flow and risk-adjusted returns.

- DSCR cushions: Maintain a Debt Service Coverage Ratio (DSCR) of 1.25 or higher to ensure sufficient income for debt obligations.

- Cash-on-cash returns: Aim for at least an 8% cash-on-cash return to achieve competitive investment performance.

- Bridge financing: Lock in draw schedules at current interest rates, with contingency reserves of 5-10% to manage potential cost overruns.

- Geographic focus: Prioritize secondary markets with strong growth prospects, such as mid-sized cities with expanding tech sectors, for enhanced risk-adjusted returns.

- Conservative underwriting: Stress test assumptions with a 2% increase in interest rates and a 10% decrease in property values to ensure resilience.

- Portfolio diversification: Balance investments across residential, commercial, and industrial assets to minimize exposure to sector-specific downturns.

With these insights and strategies, investors can confidently navigate the complexities of the real estate market, leveraging opportunities while effectively managing risks. Implementing a disciplined and informed approach will ensure robust returns and sustained growth in any market condition.

Resources

External References

Disclaimer: This market analysis is for informational purposes only and should not be considered financial or investment advice. Market conditions can change rapidly. Consult with a qualified financial or lending professional before making any decisions.