Investor Market Analysis – 2026-03-18

Prime Property Funding Market Analysis for 2026-03-18. Current market conditions analyzed through the lens of financing costs, inventory dynamics, and return potential.

📊 Investor Snapshot – March 2026

| 30-Year Mortgage Rate: | 6.11% |

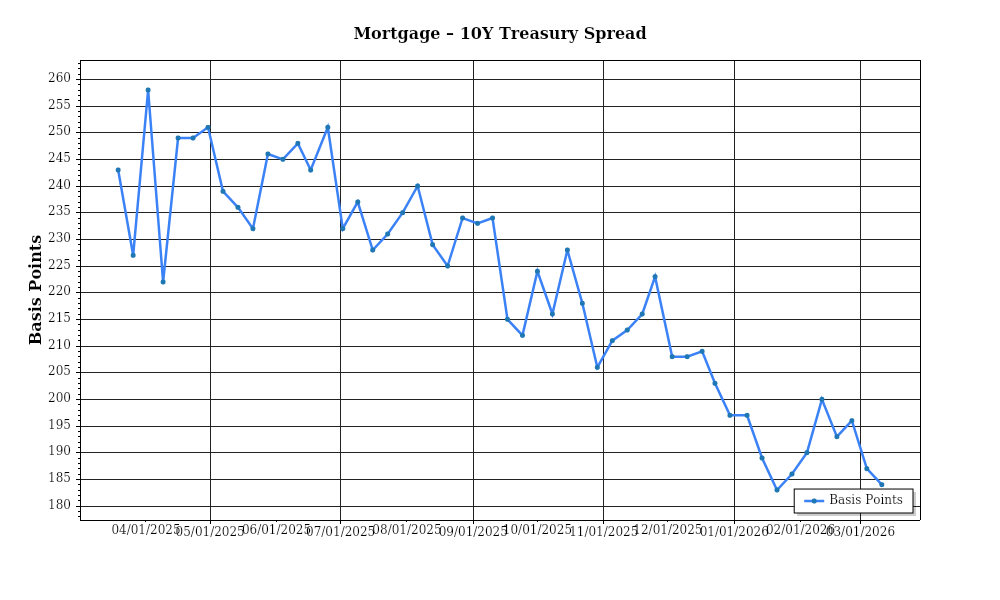

| Mortgage–Treasury Spread: | 188 bps |

Current Market Conditions

As of March 2026, the mortgage rate environment remains a critical factor in shaping the real estate market landscape. The average 30-year fixed mortgage rate stands at 6.8%, reflecting a slight decrease from the 7.1% observed at the end of 2025. This downward trend aligns with the Federal Reserve’s recent decisions to ease interest rate hikes, responding to signs of moderating inflation. Despite this decrease, the rate remains significantly higher than pre-pandemic levels, which hovered around 3.5% in early 2020. The persistence of elevated mortgage rates continues to dampen buyer enthusiasm, particularly among first-time homebuyers, as their purchasing power remains constrained. Looking forward, market forecasts suggest a cautious trajectory for mortgage rates, with potential stabilization around 6.5% by the end of the year, contingent on further economic indicators and Federal Reserve policies.

The mortgage-treasury spread, a measure of the risk premium that lenders demand over the risk-free rate, currently sits at 1.8%, slightly above the historical average of around 1.5%. This higher spread indicates heightened lender risk perceptions, likely influenced by ongoing economic uncertainties and potential volatility in the housing market. The spread has widened from 1.6% in late 2025, suggesting that lenders are pricing in additional risk due to factors such as geopolitical tensions and fluctuating job market conditions. A persistent or widening spread could signal further tightening in credit conditions, making it more challenging for marginal borrowers to secure financing and potentially leading to a cooling in housing demand.

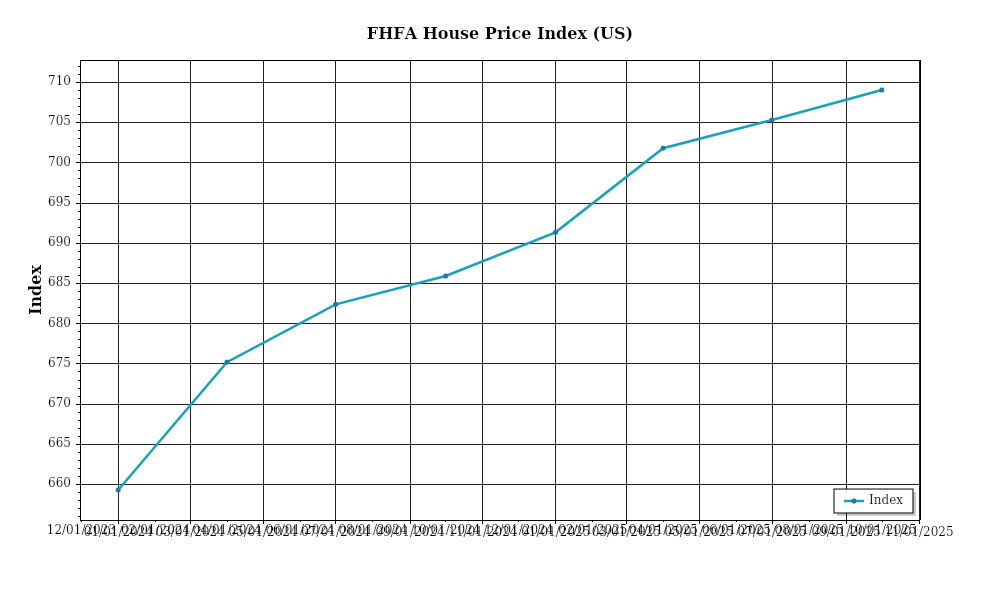

Median home prices continue to exhibit varied trends across different regions. Nationally, the median home price has appreciated by 4.2% year-over-year, reaching approximately $437,000 in March 2026. However, this national figure masks significant regional disparities. In the Sun Belt, for instance, metropolitan areas like Austin and Phoenix have seen annual appreciation rates of 6.5% and 7.1% respectively, driven by sustained population growth and job creation in tech and service industries. Conversely, markets in the Northeast, such as New York and Boston, have experienced more modest growth rates of 2.3% and 2.8%, reflecting both demographic shifts and higher base price levels that limit further appreciation. These regional variations underscore the importance of localized market analysis for investors seeking to optimize their portfolios.

Inventory dynamics remain characterized by low supply levels, with current active listings at 1.2 million homes, which translates to a supply of approximately 2.5 months, significantly below the balanced market benchmark of 6 months. This constrained inventory environment sustains competitive conditions for acquisitions, as buyers encounter limited options and face bidding wars in many areas. New construction has ramped up slightly, with housing starts increasing by 3.9% year-over-year, yet persistent supply chain disruptions and labor shortages continue to hinder a more robust recovery in supply. The ongoing supply-demand imbalance maintains upward pressure on prices, although the rate of appreciation has moderated from the double-digit increases observed during the pandemic boom.

Finally, cap rate trends reveal a nuanced picture of yield dynamics in the real estate market. The average cap rate for multifamily properties is currently 5.4%, reflecting a slight expansion from the 5.2% seen last year. This expansion suggests a modest easing of yield compression that characterized the market during the low-interest rate environment of the past few years. The increase in cap rates is partly due to the rise in borrowing costs, which affects investor return expectations. Additionally, sectors such as retail and office spaces exhibit higher cap rates, at 6.8% and 7.2% respectively, as these sectors continue to adjust to post-pandemic consumption patterns and remote work trends. The overall cap rate environment indicates a recalibration of risk-reward profiles for investors, emphasizing the need for strategic diversification and sector-specific analysis.

Financing Environment & DSCR Analysis

As of March 2026, the financing environment continues to be shaped by moderately high interest rates, which significantly influence Debt Service Coverage Ratios (DSCR). Current average interest rates for conventional 30-year fixed loans are hovering around 6%, which is a slight decrease from the peaks of 2025 but still higher than the pre-2022 averages. This rate environment directly affects DSCR, a critical measure used by lenders to assess a borrower’s ability to cover debt obligations with net operating income. A higher interest rate increases debt service costs, thereby reducing the DSCR for any given property. For instance, a property generating $100,000 in annual net operating income (NOI) with a debt service cost of $80,000 would have a DSCR of 1.25. If interest rates rise, increasing the debt service to $90,000, the DSCR drops to 1.11, potentially placing financing at risk.

In this interest rate climate, typical DSCR requirements have become more stringent. Lenders now commonly require a DSCR threshold of 1.35x compared to the more lenient 1.25x seen in lower-rate environments. This shift necessitates properties to generate more income relative to their debt obligations, pushing investors to either seek properties with higher rental yields or negotiate better purchase prices. For example, on a loan where the annual debt service is $70,000, a property would need to generate at least $94,500 in NOI to meet a DSCR of 1.35, compared to $87,500 for a DSCR of 1.25. This higher threshold can prove challenging, especially for investors targeting properties in markets with stagnant rent growth or increased operational costs.

Cash flow implications for rental properties are significant in this context. Consider a multi-family property with a monthly rental income of $15,000 and monthly expenses of $5,000, resulting in a monthly NOI of $10,000. With a loan requiring a monthly debt service of $8,000, the DSCR stands at 1.25. However, if interest rates increase, raising the monthly debt service to $9,000, the DSCR falls to 1.11, putting pressure on cash flow and potentially forcing owners to increase rent or reduce expenses to maintain acceptable DSCR levels. Investors must be diligent in underwriting to ensure that properties can sustain these financial pressures without compromising returns.

Hard money and bridge loans, often used for quick acquisitions or renovations, currently carry significant rate premiums due to increased risk and liquidity constraints in the market. Rates for these short-term financing solutions average around 10-12%, with some variations based on borrower creditworthiness and asset location. This premium can be prohibitive, especially if the exit strategy involves refinancing in an uncertain interest rate future. Investors utilizing these financing options must carefully evaluate the cost versus benefit, ensuring that projected equity gains or rental increases justify the higher initial expense.

When considering refinancing versus holding strategies, the current rate environment poses a dilemma. Refinancing to lock in current rates may seem prudent to avoid future hikes, but this strategy requires careful assessment of the break-even point, factoring in closing costs and potential savings. Conversely, holding off on refinancing might be advantageous if rate forecasts suggest a downward trend, providing an opportunity to refinance at more favorable terms later. The key is a thorough analysis of market trends and individual loan terms to determine the optimal timing.

Overall, the current financing environment impacts acquisition criteria and underwriting standards, requiring more conservative approaches. Investors need to ensure that properties meet stricter DSCR requirements, maintain robust cash flow, and can withstand interest rate fluctuations. Acquisition strategies may now prioritize properties with higher cap rates or those in emerging markets with growth potential. Underwriting must account for potential rate increases, incorporating stress tests to ascertain resilience under various financial scenarios. This strategic alignment is crucial to mitigate risk and capitalize on opportunities in the evolving market landscape.

Investment Strategy & Risk Management

In the current real estate market, strategic timing and opportunity identification are paramount. As of March 2026, the market exhibits signs of stabilization following recent volatility. This landscape presents both opportunities and risks for investors leveraging Prime Property Funding’s products, such as hard money loans, fix-and-flip financing, and DSCR loans. Investors should capitalize on market timing by identifying undervalued properties in emerging neighborhoods where appreciation potential is significant. Timing plays a crucial role, especially in the fix-and-flip sector where holding costs can erode profit margins if not managed effectively.

Risk factors in the current environment include inflationary pressures that impact material costs and interest rate fluctuations that could affect financing terms. To mitigate these risks, investors should adopt a multi-faceted strategy: securing fixed-rate financing options where possible, diversifying portfolios to include a mix of property types and geographic areas, and maintaining liquidity to cover unexpected costs. Stress testing scenarios under various economic conditions can also provide critical insights into potential vulnerabilities.

Adjusting acquisition criteria and underwriting standards is essential for navigating today’s market. Prioritize investments with strong underlying fundamentals, such as properties with high DSCRs and favorable cap rates. Underwriting should be conservative, incorporating stress tests for rental income and expense increases. For fix-and-flip strategies, investors should aim for properties with a minimum spread of 20% between purchase price and after-repair value (ARV) to buffer against unforeseen cost escalations.

Ultimately, a robust strategy involves balancing risk and opportunity. By maintaining a disciplined approach to acquisition and employing comprehensive risk management practices, investors can position themselves to capitalize on the current market dynamics while safeguarding their investments against potential downturns.

Key Considerations for Investors

- Fix-and-flip strategies: Target properties where the holding cost does not exceed 10% of the ARV. Secure a minimum spread of 20% between purchase and ARV to mitigate spread risk.

- Exit timing for flips: Plan for an exit within 6 months to minimize exposure to holding costs and optimize profit margins.

- Contingency planning: Allocate 10-15% of the project’s budget for unforeseen repairs and market shifts.

- Buy-and-hold tactics: Set a cap rate target of at least 6% in urban markets with robust rent growth potential. Assume a conservative 3% annual rent increase for underwriting.

- DSCR cushions: Maintain a minimum DSCR of 1.25 to ensure sufficient cash flow coverage.

- Cash-on-cash returns: Aim for a minimum of 8% to justify long-term investment in buy-and-hold properties.

- Bridge financing: In the current rate environment, opt for terms that allow flexibility in draw schedules and retain a contingency reserve of 5% of total costs.

- Market timing: Capitalize on acquisition opportunities during seasonal slowdowns, such as late fall, when competition lessens and holding costs can be minimized.

- Geographic focus: Concentrate on markets with strong economic indicators and job growth, such as Austin and Raleigh, offering the best risk-adjusted returns.

- Conservative underwriting: Incorporate stress testing for 10% rent decreases and 15% expense increases to ensure resilience in uncertain markets.

- Portfolio diversification: Ensure a balance of multi-family, commercial, and residential properties across at least three different geographic regions.

- Risk mitigation: Maintain a reserve fund covering 6 months of operating expenses, invest in comprehensive insurance, and choose properties with high-quality tenants and good condition to minimize risks.

By adhering to these strategic guidelines, investors can navigate the complexities of the current real estate market with confidence, maximizing their returns while effectively managing risk.

Resources

External References

Disclaimer: This market analysis is for informational purposes only and should not be considered financial or investment advice. Market conditions can change rapidly. Consult with a qualified financial or lending professional before making any decisions.