Investor Market Analysis – 2026-03-15

Prime Property Funding Market Analysis for 2026-03-15. Current market conditions analyzed through the lens of financing costs, inventory dynamics, and return potential.

📊 Investor Snapshot – March 2026

| 30-Year Mortgage Rate: | 6.11% |

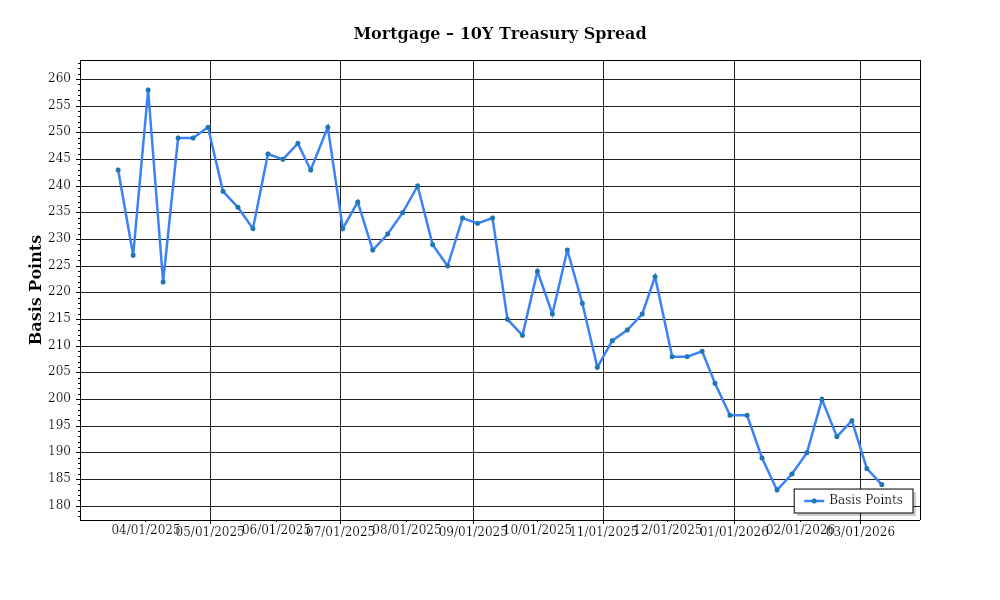

| Mortgage–Treasury Spread: | 184 bps |

Current Market Conditions

The residential real estate market is currently navigating a complex landscape shaped by various macroeconomic factors. As of March 2026, the mortgage rate environment is a pivotal element influencing buyer behavior and market dynamics. The average 30-year fixed mortgage rate stands at 5.4%, reflecting a slight increase from the previous year, where rates hovered around 4.8%. This upward trend is largely attributed to the Federal Reserve’s monetary policy adjustments aimed at curbing inflation, which has persisted above the central bank’s target. The trajectory suggests a stabilization around the current levels, contingent upon further economic indicators such as inflation and employment rates. Higher mortgage rates generally lead to increased monthly payments, which can dampen housing demand. However, the robustness of demand is likely to vary across different regions, influenced by local economic conditions and demographics.

Analyzing the mortgage-treasury spread offers insight into lender risk perception, which is crucial for investors considering mortgage-backed securities or direct real estate investments. As of March 2026, the spread between the 30-year fixed mortgage rate and the 10-year Treasury yield is approximately 170 basis points. This spread has widened slightly from 150 basis points in March 2025, indicating heightened lender caution. The increase in spread suggests that lenders are pricing in greater risk, possibly due to economic uncertainties or expectations of future rate hikes. Investors should interpret this as a signal of cautious optimism in the lending market, where lenders are mitigating potential risks from borrower defaults or fluctuations in property values.

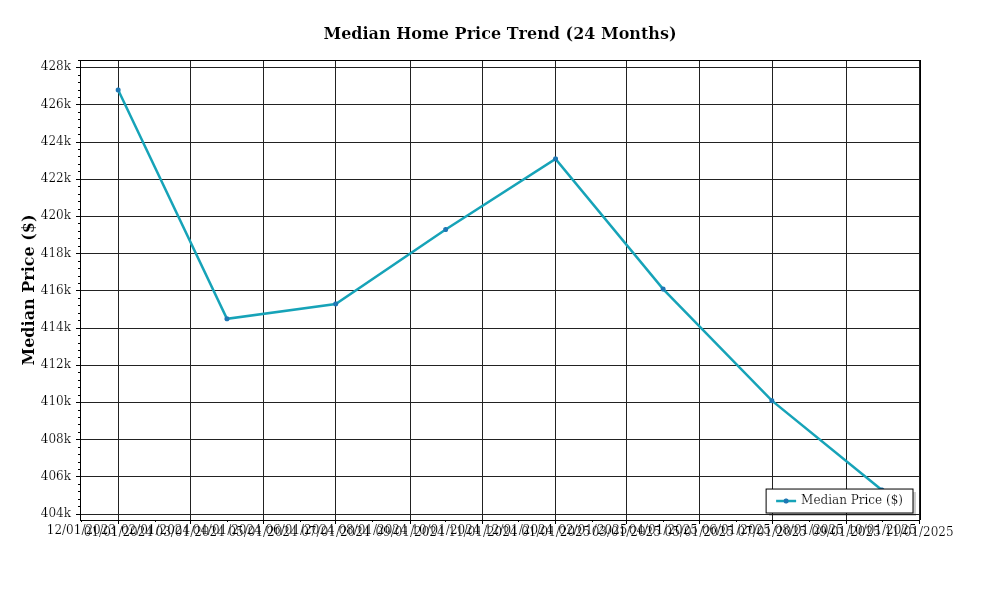

In terms of home price trends, the national median home price as of March 2026 is approximately $405,000, marking a 6.2% year-over-year appreciation rate. This price trajectory underscores the sustained demand for housing, although it reflects a moderation from the double-digit growth rates observed during the post-pandemic recovery phase. Regional variations persist, with notable appreciation in the Sun Belt states, such as Florida and Texas, where prices have surged by 8.5% and 7.9% respectively. In contrast, the Northeast, particularly New York and New Jersey, has seen more modest increases of around 3.4%. These regional disparities are influenced by migration patterns, employment opportunities, and the relative affordability of housing markets.

Inventory dynamics remain a significant factor in the current market environment. Nationally, housing inventory levels have increased marginally, with a reported 3.8 months of supply as of March 2026, compared to 3.1 months a year prior. This increment suggests a gradual easing of the severe inventory constraints that characterized the market in recent years. Despite this improvement, competition for available homes remains stiff, particularly in high-demand areas, resulting in continued upward pressure on prices. The market is approaching a more balanced state, yet the equilibrium between supply and demand is still not fully realized.

Finally, cap rate trends are a critical consideration for investors assessing potential returns on real estate investments. Average cap rates across major U.S. metropolitan areas have compressed slightly to 4.8%, down from 5.1% in March 2025. This compression indicates that property values have increased at a faster pace than net operating incomes, reflecting investor confidence in future demand and income growth prospects. However, the compression also suggests thinner margins, necessitating more strategic property acquisitions and management to achieve desired yields. For investors, understanding these trends is essential for making informed decisions in an environment characterized by both opportunities and challenges.

Financing Environment & DSCR Analysis

As of March 2026, the real estate financing environment is characterized by relatively high interest rates, leading to direct implications for the Debt Service Coverage Ratio (DSCR) of investment properties. Current interest rates for conventional loans are hovering around 6.5%, presenting challenges for investors aiming to maintain robust DSCRs. The DSCR is a crucial metric as it measures a property’s ability to cover debt obligations with its net operating income (NOI). High interest rates increase monthly debt service payments, thus potentially lowering the DSCR. For instance, an investor with a property generating a monthly NOI of $10,000 and a debt obligation of $8,000 achieves a DSCR of 1.25x. If higher interest rates increase monthly debt payments to $8,500, the DSCR falls to 1.18x, which may not meet typical lender requirements.

In the current market, lenders are generally adhering to stricter DSCR requirements, often insisting on a minimum of 1.35x rather than the previously more common 1.25x threshold. This shift reflects an environment of increased risk aversion due to economic uncertainties. To meet these requirements, investors need to ensure that properties generate sufficient cash flow, which may necessitate higher rent levels or cost efficiencies in property management. For example, a property with an NOI of $9,450 must service a debt of no more than $7,000 to achieve a DSCR of 1.35x. This tightening of requirements is prompting investors to re-evaluate their portfolios and consider enhancements that can elevate NOI.

The cash flow implications for rental properties are significant under this rate environment. With higher interest payments, the net cash flow post-debt service is often diminished. Consider a rental property with a gross income of $15,000 per month and operating expenses totaling $5,000, leaving a NOI of $10,000. With debt service rising to $8,500 due to increased interest, the cash flow shrinks to $1,500, compared to $2,000 in a lower rate environment. Such a reduction in cash flow can affect the investor’s ability to reinvest in property improvements or expand their portfolio, thus requiring careful financial strategizing and possibly renegotiating terms with lenders to maintain liquidity.

Moreover, the market for hard money and bridge loans is experiencing elevated rate premiums. These short-term financing solutions are now priced at 9% to 12%, reflecting the risk premium associated with uncertain economic conditions and the lack of liquidity in the market. Investors relying on these loans for quick acquisitions or refinancing may face increased financial strain, making it imperative to evaluate the potential for swift property value appreciation or rental income growth to justify the higher cost of capital.

In terms of refinance timing versus hold strategies, the current rate environment necessitates a nuanced approach. Investors eyeing refinancing must weigh the potential for further rate increases against current costs. If rates are projected to stabilize or decline, holding off on refinancing could be advantageous. However, if maintaining or improving DSCR is paramount, refinancing at current rates to secure favorable terms may prevent future cash flow challenges. This decision is particularly crucial for properties nearing maturity on existing loans, where the need to lock in rates might outweigh the benefits of waiting for potential rate drops.

Finally, the current financing conditions have a profound impact on acquisition criteria and underwriting standards. Investors and lenders alike are adopting more conservative approaches, emphasizing properties with strong historical income performance and resilience to economic fluctuations. Underwriting standards now often include stress testing for DSCR under varying interest rate scenarios, ensuring that properties can withstand potential rate hikes without jeopardizing financial stability. As a result, properties with robust income streams and minimal operational risks are becoming increasingly attractive in the acquisition landscape.

Investment Strategy & Risk Management

As the real estate market enters 2026, investors must adopt a strategic approach to timing and opportunity identification, especially given the current macroeconomic conditions. With interest rates stabilizing after a period of volatility, identifying the right timing for acquisitions is crucial. Investors should focus on markets that are showing signs of recovery and growth, particularly those with a combination of increasing employment rates and population growth. The key to success lies in leveraging data analytics to pinpoint these emerging markets and acting swiftly to capitalize on them.

In the current environment, several risk factors require attention. Economic uncertainties, such as potential shifts in inflation and interest rate policies, could impact property values and financing costs. Mitigation strategies should include diversifying portfolios across various asset classes and geographic locations to cushion against localized downturns. Additionally, maintaining healthy cash reserves and ensuring access to flexible financing options can help manage unforeseen expenses and market fluctuations. Investors should also stress-test their financial models to ensure they can withstand potential downturns, adjusting assumptions around rent growth and occupancy rates as needed.

Adjusting acquisition criteria and underwriting standards is essential in navigating today’s market conditions. A conservative approach, with a focus on quality over quantity, is advisable. Emphasizing properties with strong cash flow potential and manageable levels of leverage will enhance financial stability. Underwriting standards should incorporate a thorough analysis of tenant quality and property condition, as well as a detailed evaluation of market trends and local economic indicators. By setting clear criteria for cap rates, cash-on-cash returns, and debt service coverage ratios (DSCR), investors can better manage risk and optimize returns.

Prime Property Funding’s investment strategies should prioritize flexible and creative financing solutions to accommodate diverse investor needs. Fix-and-flip projects, for instance, should include comprehensive cost analysis and contingency planning to mitigate holding cost risks. For buy-and-hold investors, achieving a balance between cap rate targets and rent growth assumptions is critical for long-term success. In all strategies, maintaining an adaptable approach and actively monitoring market dynamics will empower investors to seize opportunities as they arise.

Key Considerations for Investors

- Fix-and-flip strategies: Set a maximum holding period of 6 months to minimize carrying costs; include a 10% contingency budget for unexpected repairs.

- Buy-and-hold tactics: Target properties with a minimum 6% cap rate and a DSCR of at least 1.25 to ensure robust cash flow.

- Bridge financing: Opt for loans with flexible draw schedules and maintain a contingency reserve of 5% of the total project cost.

- Market timing: Prioritize acquisitions in Q2 when market activity typically increases, balancing it against potential holding costs in slower months.

- Geographic focus: Look for opportunities in secondary markets with strong job growth, such as Austin, Charlotte, and Nashville, which offer superior risk-adjusted returns.

- Conservative underwriting: Conduct stress tests assuming a 10% drop in property values to ensure investment viability under adverse conditions.

- Portfolio diversification: Aim for a mix of 60% residential, 30% commercial, and 10% industrial properties to spread risk.

- Risk mitigation: Maintain reserves covering at least 6 months of operating expenses and ensure comprehensive insurance coverage for each property.

- Tenant quality: Prioritize tenants with credit scores above 680 and stable employment history to reduce vacancy risk.

- Property condition: Invest in properties requiring minimal repairs to avoid extensive capital expenditures and ensure quicker turnaround times.

By implementing these strategies, investors can confidently navigate the evolving market landscape, seizing opportunities while effectively managing risks.

Resources

External References

Disclaimer: This market analysis is for informational purposes only and should not be considered financial or investment advice. Market conditions can change rapidly. Consult with a qualified financial or lending professional before making any decisions.