Investor Market Analysis – 2026-03-24

Prime Property Funding Market Analysis for 2026-03-24. Current market conditions analyzed through the lens of financing costs, inventory dynamics, and return potential.

📊 Investor Snapshot – March 2026

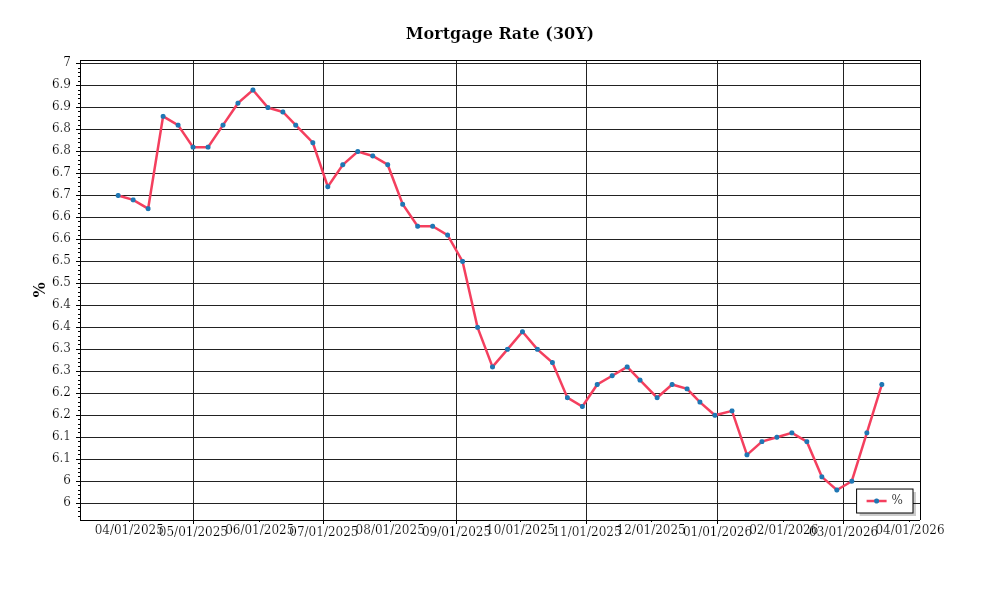

| 30-Year Mortgage Rate: | 6.22% |

| Mortgage–Treasury Spread: | 183 bps |

Current Market Conditions

The mortgage rate environment is currently a focal point for real estate investors, with rates as of March 2026 hovering around 5.75% for a 30-year fixed mortgage. This represents a slight increase from the beginning of 2026, where rates were approximately 5.50%, reflecting a general upward trend since late 2025. This increase is largely attributed to the Federal Reserve’s monetary policy adjustments aimed at curbing inflation, which stood at 3.8% year-over-year last month. The trajectory suggests a cautious upward movement, with expectations of rates reaching 6% by the third quarter if inflationary pressures persist. For investors, higher mortgage rates might translate to increased borrowing costs, potentially influencing investment decisions towards properties with higher yield prospects to offset these costs.

In terms of the mortgage-treasury spread, this crucial metric currently stands at 1.75%, having widened from 1.60% in late 2025. This spread, which is the difference between mortgage rates and the 10-year Treasury yield (now at 4%), indicates heightened risk perception among lenders. Typically, a widening spread suggests lenders are factoring in greater risks, possibly due to economic uncertainties or expectations of further rate hikes. For investors, this spread can signal more stringent lending standards or increased scrutiny on loan applications, affecting the ease of financing real estate acquisitions. Furthermore, such spreads could suggest a cautious approach by lenders, potentially leading to more conservative valuations on properties.

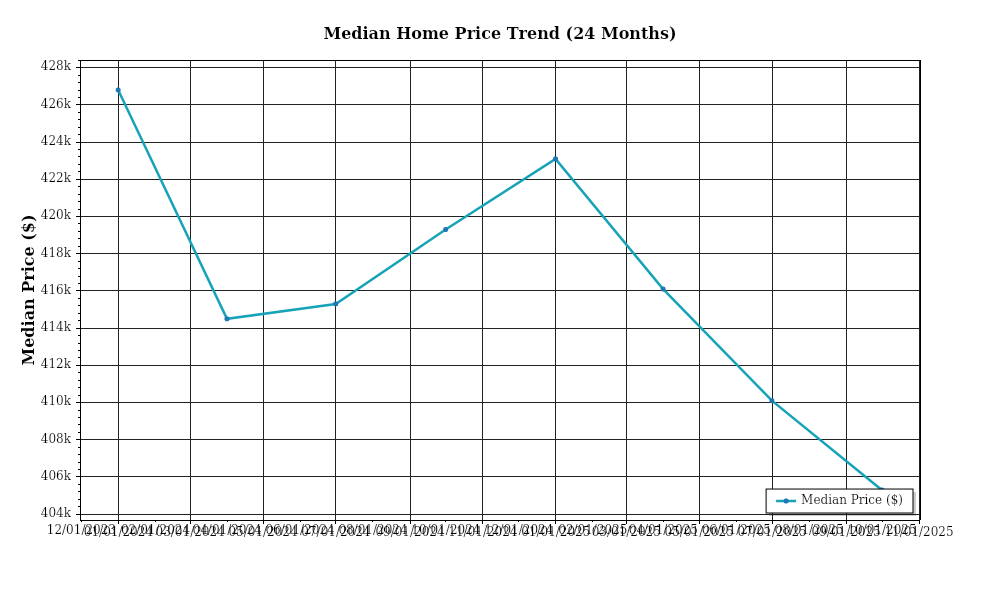

Median home prices have continued to appreciate, albeit at a moderated pace. The national median home price in March 2026 is $420,000, reflecting an annual appreciation rate of 5%. This is a deceleration from the previous year’s 7% increase, indicating a cooling off in some overheated markets. Notably, regional variations are pronounced; the Southeast, particularly cities like Tampa and Charlotte, has seen a robust appreciation rate of 8%, driven by strong population growth and economic expansion. Conversely, the West Coast markets, such as San Francisco and Los Angeles, are witnessing subdued growth, with appreciation rates around 2% due to affordability constraints and outmigration trends. Investors should consider these regional dynamics when evaluating potential for capital growth in different areas.

Inventory dynamics are experiencing a shift, with the national housing inventory currently at 2.2 months of supply, slightly up from the 2.0 months recorded at the end of 2025. This increment indicates a marginal easing in the tight supply conditions that have characterized the market recently. However, the market remains firmly in seller’s territory, as a balanced market is typically considered to be around 6 months of supply. The competition for acquisitions remains intense, particularly in high-demand areas where new listings are quickly absorbed. This sustained competition suggests continued upward pressure on prices, albeit less pronounced than in previous years, providing investors with opportunities for capital appreciation while also necessitating strategic acquisition approaches.

Cap rate trends are showing signs of stabilization, with the national average cap rate currently at 5.2%. This is a slight compression from last year’s 5.4%, reflecting sustained investor demand and limited inventory in high-demand markets. Yield compression is particularly evident in multifamily and industrial sectors, where cap rates have dropped to 4.8% and 4.5% respectively, driven by strong rent growth and resilient occupancy rates. Conversely, retail and office sectors are seeing a slower compression or even slight expansion, with cap rates at 5.7% and 6.1%, due to ongoing structural challenges. For investors, these trends imply that while opportunities for yield compression exist, particularly in sectors with robust fundamentals, careful consideration of sector-specific dynamics is crucial to optimize return on investments.

Financing Environment & DSCR Analysis

As of March 2026, the financing environment continues to see elevated interest rates, hovering around 6.5% for 30-year fixed-rate mortgages. This heightened rate environment has a direct impact on Debt Service Coverage Ratios (DSCR), a crucial metric for evaluating the financial feasibility of rental property investments. DSCR is calculated by dividing net operating income (NOI) by total debt service. With higher interest rates, monthly mortgage payments increase, thus requiring a higher NOI to achieve the same DSCR level as in lower rate environments. Consequently, properties that previously met a lender’s DSCR requirements might now fall short, compelling investors to either increase rental income or seek properties with lower purchase prices to maintain acceptable DSCR levels.

In the current market, lenders are typically insisting on stricter DSCR requirements. While historically, a DSCR of 1.25x was deemed acceptable by many financial institutions, the current climate has shifted preferences towards a threshold of 1.35x. This shift is primarily due to lenders’ increased risk aversion, aiming to ensure that properties can comfortably cover debt obligations even amidst economic volatility. For investors, this means that properties with lower cash flow margins might struggle to secure financing, pushing them to either negotiate better purchase terms or enhance property performance through strategic improvements or rent adjustments.

The implications for cash flow on rental properties are significant. Consider a scenario where a property generates a monthly NOI of $10,000. At a 1.25x DSCR, the monthly debt service would need to be $8,000 or less. However, under the more stringent 1.35x requirement, the maximum allowable debt service would drop to approximately $7,407. This tighter requirement can pose challenges for investors, particularly in high-demand markets where property prices are elevated. Investors must either find ways to increase NOI, perhaps by adding value through renovations or increasing rents, or they must reduce financing needs by injecting more equity at purchase.

The current market also sees a notable rise in hard money and bridge loan rate premiums, often ranging between 9% to 12%. These rates reflect the increased risk lenders perceive amidst economic uncertainties and higher base interest rates. Investors using such financing must carefully consider the short-term nature and higher costs of these loans, which can significantly impact profitability if not exited or transitioned to conventional financing promptly. For example, an investor utilizing a bridge loan at 10% interest must ensure that the property’s appreciation or income growth supports a rapid transition to lower-cost, long-term financing.

Given the current rate environment, investors are also reevaluating refinance timing versus hold strategies. With interest rates projected to remain elevated, the traditional logic of refinancing to reduce interest expenses may not be immediately viable. Instead, investors might opt for a hold strategy, focusing on maximizing existing cash flow and waiting for more favorable rate conditions. This approach necessitates a careful assessment of the property’s cash flow capabilities and potential appreciation over the holding period, balancing the cost of higher debt service against anticipated market gains.

The impact on acquisition criteria and underwriting standards is profound. Investors must adapt by incorporating more conservative underwriting assumptions, factoring in higher interest rates and DSCR requirements. This shift may mean recalibrating target acquisition prices or seeking properties with higher yield potentials to ensure compliance with lender standards. As a result, acquisition strategies might pivot towards markets with higher cap rates or properties with clear paths to value addition, such as those requiring renovations or located in emerging neighborhoods with growth potential.

In conclusion, the current financing environment demands strategic adaptability from investors, emphasizing the importance of thorough financial analysis and proactive cash flow management to navigate the challenges and opportunities presented by the prevailing economic conditions.

Investment Strategy & Risk Management

In the current real estate environment, strategic timing is pivotal for maximizing returns and minimizing risks. Market timing is particularly crucial as we see shifts in interest rates and potential fluctuations in property values. Investors should closely monitor macroeconomic indicators such as interest rate trends, employment statistics, and regional economic developments to identify optimal entry and exit points. For those engaged in fix-and-flip activities, timing the acquisition and sale of properties to coincide with seasonal peaks in buyer demand can significantly enhance profit margins. Conversely, buy-and-hold investors should prioritize securing properties in high-demand areas with robust rent growth prospects, ensuring a steady stream of income.

Risk factors in today’s market include economic volatility, fluctuating interest rates, and potential regulatory changes. Mitigation strategies should focus on diversification across geographic regions and property types to buffer against localized downturns. Investors should also implement conservative underwriting standards, stress-testing investment assumptions under various economic scenarios. For instance, ensuring that debt service coverage ratios (DSCR) remain comfortably above 1.2 even in downturn scenarios can safeguard against cash flow shortfalls. Additionally, maintaining liquidity through ample cash reserves and contingency planning will allow investors to navigate unforeseen challenges.

Adjusting acquisition criteria and underwriting standards is essential in this environment. Investors should prioritize properties with strong fundamentals, such as location, demand, and potential for appreciation. Underwriting standards should incorporate more stringent criteria, such as higher threshold cap rates and lower leverage ratios, to account for potential market corrections. This conservative approach will not only reduce risk but also position investors to capitalize on opportunities that arise from distressed sellers or undervalued properties.

Prime Property Funding’s focus on providing hard money loans, fix-and-flip financing, and DSCR loans positions investors advantageously. By leveraging their expertise in these areas, investors can enhance their strategic planning and execution. Fix-and-flip investors, for example, can benefit from favorable loan terms that allow for quicker turnaround times, while buy-and-hold investors can secure competitive DSCR loans that enhance portfolio stability. Ultimately, by aligning investment strategies with current market realities and leveraging Prime Property Funding’s offerings, investors can confidently navigate the complexities of today’s real estate market.

Key Considerations for Investors

- Fix-and-flip strategies: Maintain holding costs below 10% of the total project budget to ensure profitability in case of market slowdowns.

- Spread risk: Aim for a minimum 20% profit margin on flips to cushion against unexpected costs or delays.

- Exit timing: Plan property sales to coincide with peak buying seasons, typically spring and early summer, to maximize buyer interest.

- Contingency planning: Allocate at least 5% of project costs for unexpected expenses or delays in the renovation process.

- Buy-and-hold tactics: Target cap rates of 6% or higher in growth markets to achieve desirable cash flow and appreciation potential.

- DSCR cushions: Ensure DSCR remains above 1.3 to withstand economic fluctuations and maintain positive cash flow.

- Bridge financing: Opt for flexible draw schedules that align with project timelines to minimize interest costs.

- Geographic focus: Prioritize investments in markets with at least 3% annual rent growth and stable economic indicators for best risk-adjusted returns.

- Conservative underwriting: Stress test assumptions with a 10% decline in property values to evaluate investment resilience.

- Portfolio diversification: Balance asset classes and geographic locations, ensuring no single market or asset class exceeds 25% of the portfolio.

- Risk mitigation: Maintain reserves covering at least six months of operating expenses and debt obligations to safeguard against tenant turnover or economic disruptions.

By embracing these strategic insights and detailed action points, investors can position themselves to seize opportunities and mitigate risks, ensuring sustained success in the dynamic real estate market.

Resources

External References

Disclaimer: This market analysis is for informational purposes only and should not be considered financial or investment advice. Market conditions can change rapidly. Consult with a qualified financial or lending professional before making any decisions.