Investor Market Analysis – 2026-03-16

Prime Property Funding Market Analysis for 2026-03-16. Current market conditions analyzed through the lens of financing costs, inventory dynamics, and return potential.

📊 Investor Snapshot – March 2026

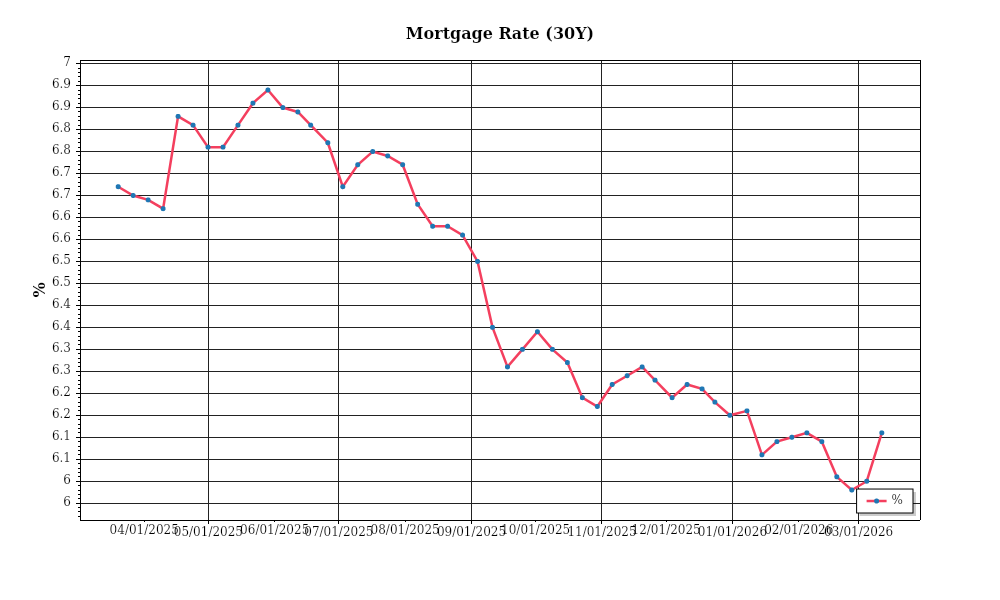

| 30-Year Mortgage Rate: | 6.11% |

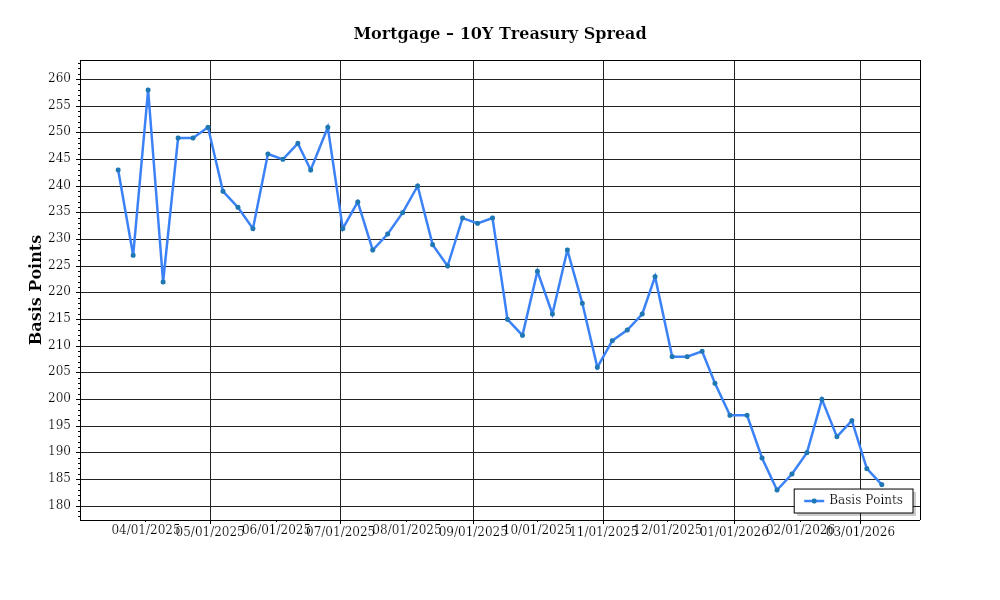

| Mortgage–Treasury Spread: | 184 bps |

Current Market Conditions

As of March 2026, the real estate market is navigating a complex landscape, shaped significantly by the mortgage rate environment. Currently, the average 30-year fixed mortgage rate stands at 6.8%, reflecting a modest increase from 6.5% in January 2026. Over the past year, the mortgage rates have experienced volatility, peaking at 7.2% in September 2025 before gradually easing. This trajectory is largely influenced by the Federal Reserve’s monetary policy, which has shifted towards a more dovish stance amid cooling inflationary pressures. The recent stabilization of rates suggests a cautious optimism among lenders and borrowers, though the potential for further rate adjustments remains contingent on economic indicators. The current rate environment impacts affordability and buyer sentiment, with higher rates dampening purchasing power, thereby influencing demand dynamics in the housing market.

The spread between mortgage rates and 10-year Treasury yields, known as the mortgage-treasury spread, is a critical indicator of lender risk perception. As of March 2026, this spread is at 2.2%, slightly above the historical average of 1.7%. This elevated spread indicates heightened risk aversion among lenders, potentially due to geopolitical uncertainties and concerns over economic growth. When the spread widens, it suggests that lenders are demanding a higher risk premium to compensate for perceived uncertainties. This can lead to stricter lending standards and impact the availability of credit to homebuyers. Conversely, a narrowing spread would signal easing lender concerns and potentially more favorable borrowing conditions. Monitoring this spread is essential, as it provides insights into the broader economic climate and lender sentiment.

Median home prices continue to exhibit notable appreciation, albeit at a moderated pace compared to the frenetic gains observed during the pandemic-induced housing boom. The national median home price is currently $424,000, representing a 4.3% year-over-year increase. This marks a deceleration from double-digit annual gains recorded in the previous years. Regionally, price trends vary significantly; the Southeast and South-Central regions have seen robust growth, with median prices rising by 6% and 5.5% respectively, driven by strong in-migration and economic expansion. In contrast, the West Coast markets, particularly in California, are witnessing a slowdown in appreciation, with some areas experiencing slight declines, reflecting affordability challenges and outmigration. These disparities underscore the importance of regional analysis in investment decision-making.

Inventory dynamics remain a focal point, as supply constraints continue to shape market conditions. Nationally, the housing inventory stands at 1.2 million units, translating to a 2.5-month supply. This level is below the balanced market threshold of 6 months, highlighting ongoing supply-demand imbalances. The constrained inventory has intensified competition among buyers, particularly in high-demand markets, leading to bidding wars and elevated prices. New construction has been slow to bridge the gap, with regulatory hurdles and labor shortages impeding progress. This constrained environment favors sellers, but poses challenges for buyers, particularly first-time purchasers who may face affordability barriers. The inventory situation requires ongoing attention to assess shifts in market equilibrium.

Cap rate trends are pivotal for real estate investors, reflecting the relationship between property income and value. Currently, national cap rates for multifamily properties average 5.4%, up from 5.2% a year ago. This increase indicates a slight yield expansion, driven by rising interest rates and evolving market conditions. Sectors such as industrial and retail are experiencing disparate trends; industrial properties, buoyed by e-commerce demand, maintain lower cap rates around 4.8%, while retail properties face upward pressure, with cap rates averaging 6.0%, reflecting investor caution amid sectoral challenges. Yield compression was a hallmark of the previous cycle, but the current environment suggests a rebalancing towards historical norms. Understanding cap rate fluctuations is essential for assessing investment viability and potential returns in the current market landscape.

Financing Environment & DSCR Analysis

As of March 2026, the real estate financing environment is characterized by moderately high interest rates, which directly impact the Debt Service Coverage Ratio (DSCR) for property investors. Currently, average commercial loan rates hover around 6%, a level that necessitates careful consideration of DSCR in underwriting processes. DSCR is a critical metric for assessing a property’s ability to cover its debt obligations with its net operating income (NOI). With elevated interest rates, investors face increased debt servicing costs, which in turn pressures the DSCR. For instance, if a property generates an NOI of $120,000, under the current interest rate, a loan requiring an annual debt service of $100,000 results in a DSCR of 1.20x. This is below the more conservative standard many lenders now require.

In today’s market, typical DSCR requirements range between 1.25x and 1.35x, depending on the lender’s risk appetite and the property’s asset class. A 1.25x DSCR, for example, means that a property must generate $1.25 in NOI for every dollar of debt payment, affording a buffer against income fluctuations or unexpected expenses. Lenders in this environment are leaning towards the higher end of this spectrum, with a preference for a 1.35x DSCR, given the economic uncertainties and property market volatility. This means that properties with thinner margins might struggle to secure favorable financing, pushing investors to either improve property cash flows or inject additional equity to meet these stringent requirements.

The implications for cash flow on rental properties are significant. To illustrate, consider a multifamily property with an annual NOI of $200,000. At a 6% interest rate, assuming a $1,000,000 loan, the annual debt service is approximately $72,000. This results in a DSCR of 2.78x, which appears comfortable. However, when exploring properties with less robust cash flows or higher leverage, the room for error shrinks. For instance, if the NOI were to decline to $150,000 due to increased vacancies or unexpected maintenance costs, the DSCR would plummet to 2.08x, straining the financial viability under more stringent lending criteria. These scenarios highlight the importance of maintaining a healthy margin above the lender’s minimum DSCR to cushion against potential financial shocks.

In the current market, hard money and bridge loans continue to be viable options, albeit at a premium. These short-term financing solutions typically command rates between 8% and 12%, reflecting their riskier nature and the urgency often associated with their use. Investors pursuing these financing avenues must be astute in calculating the cost-benefit dynamics, as the higher rates can erode profit margins if the exit strategy—often refinancing or selling—is delayed or compromised. This premium underscores the necessity for precise timing and strategic planning when engaging in projects requiring such financing solutions.

Given the rate environment, the decision to refinance or hold becomes pivotal. If rates are anticipated to stabilize or decrease, holding off on refinancing may be strategic, preserving current terms until more favorable conditions arise. Conversely, if rising rates are forecasted, locking in current terms could prevent future increases in debt servicing costs. Investors must weigh these considerations against their acquisition criteria and underwriting standards, which are increasingly stringent. Higher rates compel investors to adopt more conservative underwriting, focusing on properties with strong cash flow projections and lower leverage to ensure compliance with elevated DSCR thresholds. This shift in criteria enhances the focus on quality assets capable of weathering economic shifts, albeit narrowing the field of suitable investment opportunities.

In conclusion, the financing environment as of March 2026 demands a cautious approach to leveraging and refinancing, with a keen focus on maintaining robust DSCRs to navigate the complexities of the current market. Investors must adapt their strategies to align with these financial realities, ensuring that their portfolios are resilient against the backdrop of higher interest rates and stringent lending standards.

Investment Strategy & Risk Management

As we navigate the real estate market in March 2026, timing remains a critical factor in maximizing returns. The current environment, characterized by fluctuating interest rates and evolving buyer sentiments, necessitates a strategic approach to market timing. Investors should focus on identifying opportunities in underpriced segments or emerging neighborhoods, where value appreciation is more likely. Monitoring local economic indicators and demographic shifts can provide insights into potential growth areas. Engaging with local real estate networks can also offer timely information about off-market deals and distressed properties, which can yield higher returns when the market rebounds.

The current market environment presents specific risks, including interest rate volatility and potential shifts in tenant demand due to economic uncertainties. To mitigate these risks, investors should prioritize flexible financing options, such as adjustable-rate mortgages, that allow for adjustments in response to rate changes. Diversifying property holdings geographically and across different asset classes reduces exposure to localized market downturns. Additionally, investors should engage in rigorous due diligence and stress testing of financial models to ensure they can withstand adverse scenarios.

Adjusting acquisition criteria and underwriting standards is essential to align with the current market dynamics. Investors should consider revising their cap rate targets upward to accommodate potential increases in borrowing costs. Emphasizing properties with strong cash flow potential and stable tenant demand will provide a buffer against market fluctuations. Underwriting standards should incorporate more conservative assumptions regarding rent growth and vacancy rates, ensuring that investments remain viable under less favorable conditions. By maintaining a disciplined approach to deal evaluation, investors can safeguard their portfolios against unforeseen market shifts.

In conclusion, the real estate market continues to offer promising opportunities despite the challenges. By adopting a strategic approach to market timing, risk management, and acquisition criteria adjustments, investors can position themselves for success. Staying informed and agile will enable investors to capitalize on emerging trends and mitigate risks effectively.

Key Considerations for Investors

- Fix-and-flip strategies: Limit holding costs to less than 15% of total project costs to preserve margins.

- Spread risk: Ensure a minimum gross profit margin of 20% to buffer against market volatility.

- Exit timing: Plan for project completion within 6-9 months to avoid extended market exposure.

- Contingency planning: Allocate 10% of project budget for unexpected costs to prevent financial strain.

- Buy-and-hold tactics: Target cap rates of 6-8% to achieve attractive risk-adjusted returns.

- Rent growth assumptions: Use conservative estimates of 3-4% annual growth to avoid overestimating potential income.

- DSCR cushions: Maintain a minimum DSCR of 1.25 to ensure adequate debt coverage.

- Bridge financing: Opt for draw schedules that align with project milestones to optimize cash flow management.

- Geographic focus: Prioritize markets with strong job growth and population increases, such as Austin and Raleigh, for enhanced risk-adjusted returns.

- Conservative underwriting: Stress test financial models with a 10% vacancy rate to ensure resilience in downturn scenarios.

- Portfolio diversification: Balance investments across residential, commercial, and industrial properties to mitigate sector-specific risks.

- Risk mitigation: Maintain reserves equivalent to 6 months of operating expenses to cushion against unforeseen challenges.

By implementing these strategies and maintaining a proactive approach, investors can confidently navigate the complexities of the current real estate market.

Resources

External References

Disclaimer: This market analysis is for informational purposes only and should not be considered financial or investment advice. Market conditions can change rapidly. Consult with a qualified financial or lending professional before making any decisions.