Investor Market Analysis – 2026-06-10

Prime Property Funding Market Analysis for 2026-06-10. Current market conditions analyzed through the lens of financing costs, inventory dynamics, and return potential.

📊 Investor Snapshot – June 2026

| 30-Year Mortgage Rate: | 6.48% |

| Mortgage–Treasury Spread: | 192 bps |

Current Market Conditions

As of June 2026, the real estate market is navigating a complex landscape shaped by fluctuating mortgage rates, shifting home prices, and evolving inventory dynamics. The mortgage rate environment is a critical factor in this equation. Currently, the average 30-year fixed-rate mortgage stands at 5.75%, a slight decrease from the 6.10% observed in early 2026. This decline follows a broader trend since the Federal Reserve’s pivot towards a more accommodative monetary policy in late 2025. Over the last twelve months, mortgage rates have fluctuated between 5.5% and 6.8%, reflecting both macroeconomic uncertainties and central bank interventions. The trajectory of these rates indicates a potential stabilization around the current level if inflationary pressures continue to ease and economic growth remains moderate.

The mortgage-treasury spread, an essential indicator of lender risk perception, currently sits at approximately 220 basis points. This spread, which has widened from 185 basis points a year ago, suggests heightened risk aversion among lenders. Historically, a spread exceeding 200 basis points signals increased caution due to economic uncertainties or potential borrower defaults. The current spread is influenced by global economic conditions, including geopolitical tensions and volatile energy prices, which have introduced a higher degree of risk into the lending environment. This spread reflects lenders’ need to maintain profitability while accounting for increased risks, thereby affecting mortgage availability and affordability.

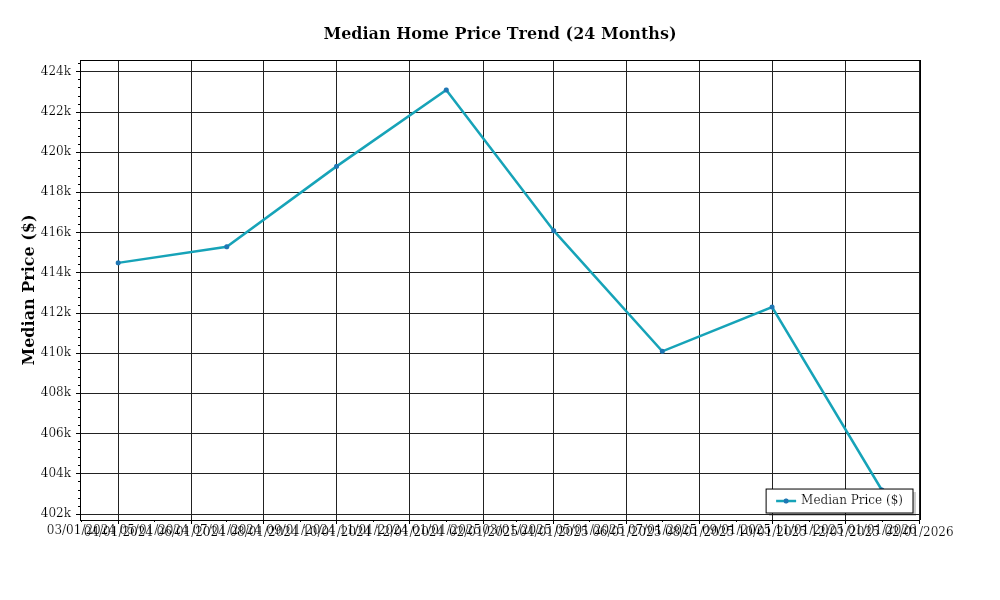

Median home prices continue their upward trajectory, albeit at a more modest pace compared to the past few years. As of June 2026, the median home price nationwide is $412,000, representing a 4.2% increase from June 2025. This rate of appreciation marks a slowdown from the double-digit gains experienced during the pandemic-induced housing boom. Regionally, variations are pronounced; for example, the West Coast continues to experience robust growth with cities like San Francisco reporting a 6.5% year-over-year increase, while the Midwest sees more tempered growth at 2.8%. These disparities highlight the influence of local economic conditions, population shifts, and housing demand on price dynamics.

Inventory levels remain a pivotal factor in market balance. As of this month, the national housing inventory is approximately 1.2 million units, marking a 15% increase from a year ago. This rise in supply is bringing the market closer to a balanced state, as the previous years were characterized by acute shortages driving intense buyer competition. The current inventory represents a supply of 3.5 months, still below the 5-6 months typical of a balanced market, indicating ongoing pressure in certain regions. However, the increased inventory levels are beginning to moderate price growth and provide more options for buyers, particularly in previously undersupplied markets.

Cap rate trends offer insights into investor sentiments and yield expectations. As of June 2026, the average cap rate for commercial real estate is 5.2%, a slight expansion from 4.9% in June 2025. This increase suggests that investors are demanding higher returns due to perceived risks and the aforementioned interest rate adjustments. Yield compression, which characterized the earlier part of the decade, has given way to a more cautious outlook. The slight expansion in cap rates reflects adjustments in investor strategies, as they balance the pursuit of income with the risks posed by economic volatility and rising operational costs. This shift may lead to more selective acquisition strategies, with investors prioritizing assets with strong income potential and lower exposure to market fluctuations.

Financing Environment & DSCR Analysis

As of June 2026, the financing environment is characterized by a nuanced interplay between interest rates and debt service coverage ratios (DSCR), crucial for real estate investors. The current interest rates have a significant impact on DSCR, which is a critical metric used by lenders to assess the risk of lending. Higher interest rates increase the cost of borrowing, thus affecting the ability of rental properties to generate sufficient net operating income (NOI) to cover debt obligations. With the Federal Reserve maintaining a steady interest rate of approximately 5.5%, up from 4.75% in early 2025, borrowing costs have increased, thereby tightening DSCR ratios.

In this environment, typical DSCR requirements are stricter. Most lenders now demand a DSCR of at least 1.35x rather than the previous 1.25x threshold. This shift underscores lenders’ heightened caution, ensuring that properties have a more substantial buffer to withstand economic fluctuations. For instance, a property with an annual debt obligation of $100,000 must now generate at least $135,000 in NOI to qualify for refinancing or new financing. This increase in the required DSCR means that investors must carefully evaluate potential acquisitions, ensuring that properties can not only meet these benchmarks but also sustain them over the loan term.

The implications for cash flow, particularly for rental properties, are considerable. To illustrate, consider a multifamily rental property with a monthly mortgage payment of $10,000. Under a 1.35x DSCR, the required monthly NOI would be $13,500. If the property currently generates $12,000 in NOI, it falls short by $1,500 monthly, necessitating either operational improvements to increase income or cost reductions to enhance profitability. Investors must scrutinize rental income projections, occupancy rates, and operational efficiencies more rigorously to meet these DSCR demands, often deploying enhanced asset management strategies to optimize cash flow.

The current market also witnesses notable premiums on hard money and bridge loan rates. With traditional financing becoming more restrictive, these short-term loan options are in high demand, often carrying interest rates as high as 9% to 12%, compared to traditional mortgages hovering around 5.5% to 6%. These rates reflect the increased risk perceived by lenders in a volatile market, and while they offer flexibility for acquisitions and renovations, they also necessitate careful consideration of the overall cost of capital and exit strategies to avoid eroding investment returns.

Given the current rate environment, the decision to refinance or hold is pivotal. For properties that secured financing at lower rates prior to recent hikes, holding may be advantageous to maintain favorable loan terms. Conversely, properties with high existing rates might benefit from refinancing, despite current higher rates, if it results in better DSCR management or aligns with strategic objectives such as unlocking equity for further investments. Investors must conduct a thorough cost-benefit analysis, considering both immediate cash flow impacts and long-term financial health.

The impact on acquisition criteria and underwriting standards is marked by a shift towards more stringent assessments. Lenders and investors are now placing greater emphasis on intrinsic property value, income stability, and market conditions. The focus has intensified on properties in robust markets with strong rental demand and limited supply, ensuring resilience against potential downturns. Underwriting standards have tightened, with more conservative income projections and higher reserve requirements to safeguard against unforeseen expenses.

In summary, the financing environment as of June 2026 demands a strategic approach, balancing interest rate risks with DSCR requirements to optimize real estate investment performance. Investors must adapt by enhancing operational efficiencies, reevaluating financing strategies, and rigorously analyzing acquisition opportunities to align with the evolving market conditions.

Investment Strategy & Risk Management

In the current real estate landscape, characterized by fluctuating interest rates and evolving market dynamics, strategic timing and decisive opportunity identification are crucial for maximizing investment returns. Investors need to remain vigilant in monitoring economic indicators and local market conditions to identify optimal entry points. The cyclical nature of real estate suggests that periods of market cooling can present lucrative acquisition opportunities, particularly for those prepared to act swiftly when prices stabilize. Timing should be closely aligned with both short-term trends and long-term market cycles to harness potential gains effectively.

Risk factors in today’s environment include rising interest rates, regulatory changes, and tightening lending standards, which could impact liquidity and borrowing costs. To mitigate these risks, investors should adopt a proactive approach, including maintaining a diverse portfolio and securing financing well ahead of planned acquisitions. Building strong relationships with lenders, like Prime Property Funding, can also provide access to flexible financing options such as hard money loans and DSCR loans, which are less sensitive to conventional banking constraints.

Adjusting acquisition criteria and underwriting standards is essential in navigating the present market uncertainties. Investors should emphasize conservative underwriting, incorporating stress tests to anticipate potential downturns. This includes setting higher cap rate targets to buffer against rental market fluctuations and ensuring DSCR cushions are substantial enough to withstand revenue variability. Additionally, investors should refine their property selection criteria, focusing on assets with strong fundamentals and growth potential in resilient markets.

Strategically managing risk through diversification and sound financial planning is paramount. By balancing asset classes, geographic locations, and investment strategies, investors can shield their portfolios from sector-specific downturns. Additionally, establishing robust contingency plans, including adequate reserves and insurance coverage, will further safeguard investments against unforeseen events. Ultimately, success in this environment hinges on a disciplined, informed approach to investment strategy, leveraging data-driven insights to capitalize on emerging opportunities.

Key Considerations for Investors

- For fix-and-flip strategies, maintain holding costs at or below 20% of total project costs to ensure profitability and manage spread risk effectively.

- Implement a contingency plan that allocates at least 10% of project budgets for unexpected expenses to prevent overruns.

- Set cap rate targets at a minimum of 6% for buy-and-hold properties to achieve favorable cash flow and account for potential rent stagnation.

- Ensure a minimum DSCR cushion of 1.25 to provide a safety net against fluctuating rental incomes and interest rate hikes.

- Optimize cash-on-cash returns to exceed 8% annually, ensuring investments yield substantial returns relative to initial capital outlay.

- In the current rate environment, lock in bridge financing at fixed rates to mitigate the impact of potential interest rate increases.

- Prioritize markets with risk-adjusted returns by focusing on areas with strong employment growth and stable population increases, such as Austin and Raleigh.

- Conduct stress testing on underwriting assumptions with scenarios projecting a 20% decline in property values to evaluate resilience in downturns.

- Enhance portfolio diversification by allocating no more than 40% of investments in any single asset class or geographic location.

- Maintain contingency reserves equivalent to six months of operating expenses to buffer against unexpected vacancies or economic shifts.

By adhering to these strategies and recommendations, investors can confidently navigate the complexities of the current real estate market, seizing opportunities while effectively managing risks.

Resources

External References

Disclaimer: This market analysis is for informational purposes only and should not be considered financial or investment advice. Market conditions can change rapidly. Consult with a qualified financial or lending professional before making any decisions.