Investor Market Analysis – 2026-06-07

Prime Property Funding Market Analysis for 2026-06-07. Current market conditions analyzed through the lens of financing costs, inventory dynamics, and return potential.

📊 Investor Snapshot – June 2026

| 30-Year Mortgage Rate: | 6.48% |

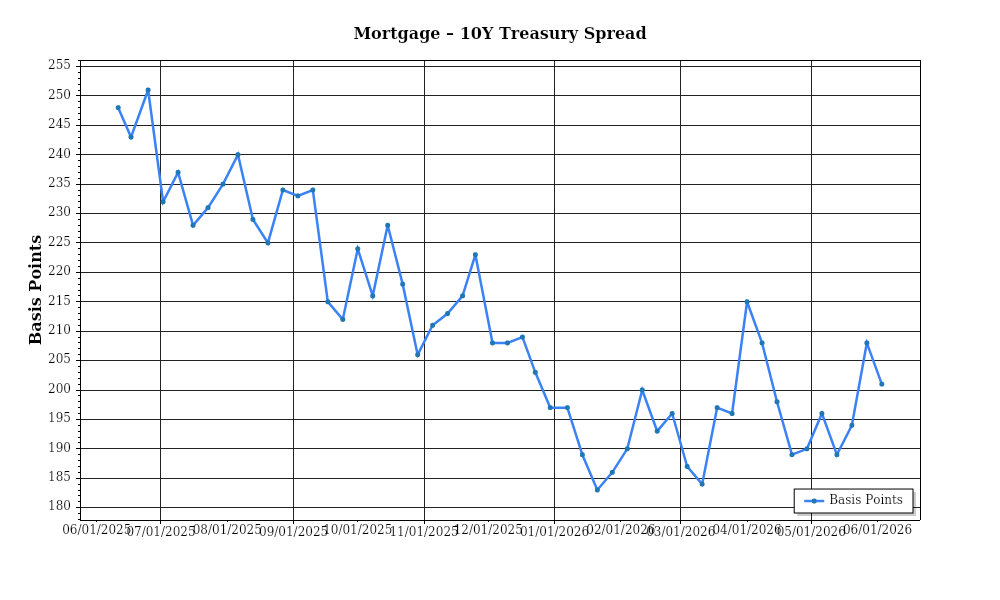

| Mortgage–Treasury Spread: | 201 bps |

Current Market Conditions

As of June 2026, the real estate market is navigating complex dynamics influenced by fluctuating mortgage rates, evolving inventory levels, and regional price disparities. The mortgage rate environment is particularly notable, with the average 30-year fixed mortgage rate currently standing at 6.8%. This marks a 0.5% increase from the beginning of the year, driven largely by the Federal Reserve’s ongoing efforts to counter inflation through incremental rate hikes. These hikes have created a cautious lending environment, where both lenders and borrowers are recalibrating expectations. In recent months, the trajectory of mortgage rates suggests a potential stabilization, as inflationary pressures begin to ease. However, the volatility remains a concern, with potential geopolitical events or economic shifts that could prompt further rate adjustments.

The mortgage-treasury spread, a critical indicator of lender risk perception, has widened to 2.0% compared to the historical average of 1.7%. This spread indicates a heightened risk aversion among lenders, who are compensating for perceived uncertainties by demanding higher premiums. The driving factors behind this widening spread include not only the aforementioned rate hikes but also concerns over economic slowdown and borrower creditworthiness. The larger spread reflects a period of cautious optimism where lenders are pricing in potential risks while remaining engaged in the market. For investors, this signals a need to carefully assess financing options and consider the implications of lender sentiment on borrowing costs and investment returns.

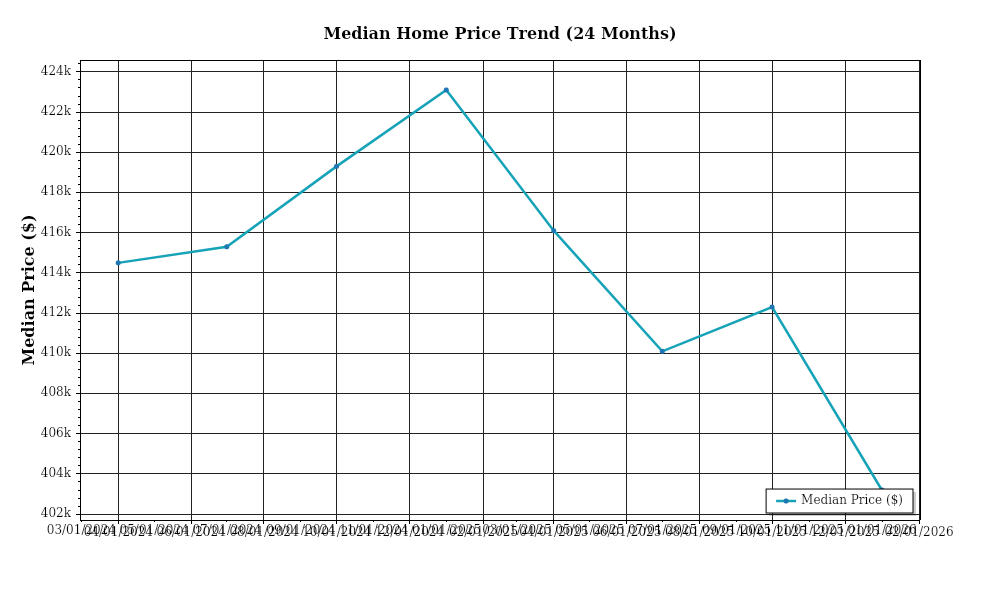

Median home prices have continued their upward trajectory, although the rate of appreciation has moderated. Nationwide, the median home price is approximately $395,000, representing a year-over-year increase of 4.5%. This is a deceleration from the double-digit growth rates observed in previous years, indicative of a market gradually returning to balance. Regional variations are pronounced, with the Sun Belt regions such as Florida and Texas experiencing higher appreciation rates of 6.5% and 7.2%, respectively. Conversely, markets in the Midwest are seeing more modest increases, with states like Ohio and Indiana recording appreciation rates of 2.8% and 3.1%. These disparities highlight the importance of localized market analysis when considering investment opportunities.

Inventory dynamics are a critical component of the current market conditions. As of June 2026, the national housing inventory has increased modestly, with supply levels at approximately 3.1 months, compared to the 2.5 months recorded a year ago. This shift towards a more balanced market is attributed to both increased new construction and a gradual slowdown in demand due to higher borrowing costs. Despite these improvements, competition for acquisitions remains intense in certain high-demand areas, particularly in urban centers and attractive suburban markets. As a result, while some markets are approaching equilibrium, others continue to experience competitive bidding scenarios, necessitating strategic planning for acquisitions.

Cap rate trends further illustrate the evolving market dynamics, with overall cap rates experiencing slight compression. Currently, the average cap rate for multifamily properties is 5.2%, down from 5.5% a year ago. This compression is indicative of sustained investor demand and confidence in income-producing assets, despite rising interest rates. The yield compression is more pronounced in high-growth areas, where investors are willing to accept lower returns in exchange for perceived long-term value appreciation. However, in less vibrant markets, cap rates have remained stable or even expanded slightly, reflecting a divergence in investor sentiment based on geographic and asset-specific factors.

These current market conditions underscore a period of adjustment and recalibration within the real estate landscape. As mortgage rates shift, inventory levels adjust, and regional disparities persist, investors must remain vigilant and data-driven in their approach to capitalize on opportunities amidst the evolving economic backdrop.

Financing Environment & DSCR Analysis

The financing environment as of June 2026 is characterized by elevated interest rates, which have significant implications for debt service coverage ratios (DSCR) and overall investment strategies in the real estate market. The current average interest rate for commercial loans is around 7.5%, a level that has put pressure on DSCR calculations. A higher interest rate increases the cost of borrowing, thus impacting the ability of revenue generated from properties to cover debt obligations. In a scenario where an investor holds a property generating $120,000 annually with a debt obligation of $100,000, the DSCR would be 1.20x. This falls short of the common lender requirement of 1.25x, reflecting the challenges investors face in maintaining adequate coverage amidst rising rates.

Lenders have adapted to the current environment by adjusting DSCR requirements. While a DSCR requirement of 1.25x was typical in a lower interest rate environment, many lenders now prefer a threshold of 1.35x as a buffer against potential income volatility and increased borrowing costs. This shift requires investors to ensure their properties generate more income relative to debt payments. For example, if a property has an annual debt obligation of $90,000, the required minimum net operating income to meet a 1.35x DSCR would be $121,500. This adjustment impacts acquisition strategies as investors must seek properties with higher income potential or consider value-add opportunities to meet these stricter criteria.

The implications for cash flow in rental properties are significant. Investors must now reassess their cash flow projections to ensure investments remain viable under these new DSCR requirements. Assuming an investor purchases a property for $1 million with a 75% loan-to-value ratio, the annual debt service at a 7.5% interest rate would be approximately $56,250. To meet a 1.35x DSCR, the property must generate at least $75,938 in net operating income. If the property’s current income falls short, investors may need to implement rent increases or improve operational efficiencies to bridge the gap. These adjustments are critical to maintaining positive cash flow and achieving desired returns.

In the current market, rates for hard money and bridge loans have also increased, with premiums now ranging from 10% to 14%. These rates reflect the heightened risk associated with such financing options, particularly given the volatile interest rate environment. Consequently, investors utilizing these instruments must be wary of the impact on overall project costs and potential refinancing challenges. The premium over traditional financing highlights the need for precise underwriting and exit strategies, particularly in short-term holding scenarios where investors anticipate refinancing into more favorable terms once stabilization is achieved.

Given the prevailing rate environment, the timing of refinancing versus holding strategies is a critical consideration. Investors must weigh the cost of maintaining current financing terms against potential savings from refinancing, should rates decrease in the future. For instance, if an investor expects rates to drop to 6% within the next year, refinancing a $1 million loan from 7.5% could save approximately $15,000 annually in interest. However, investors must also consider the costs associated with refinancing, including fees and possible prepayment penalties, which can impact the net benefit of such a decision.

The current interest rate landscape necessitates a reevaluation of acquisition criteria and underwriting standards. Investors must adopt a conservative approach, focusing on properties with robust income streams and potential for growth. Underwriting standards now require a deeper analysis of market trends, tenant creditworthiness, and long-term viability to ensure investments align with heightened DSCR requirements. In this environment, due diligence and strategic planning are paramount to mitigate risks and capitalize on opportunities within the real estate market.

Investment Strategy & Risk Management

In the current real estate landscape of mid-2026, investors must meticulously consider **market timing** and **opportunity identification** as pivotal components of their strategy. With interest rates stabilizing after a period of volatility, there is renewed potential for entry into the market. However, investors should remain vigilant and adaptable, closely monitoring both macroeconomic indicators and local market signals. Identifying opportunities requires a deep dive into regional trends, such as population shifts, employment growth, and infrastructure developments, which can signal burgeoning markets ripe for investment. Investors should focus on properties that not only meet immediate market demand but also have the potential for appreciation as economic conditions evolve.

The current environment presents several **risk factors**, including potential regulatory changes, geopolitical tensions, and the lingering effects of global supply chain disruptions. To mitigate these risks, investors should employ robust due diligence processes, ensuring all potential acquisitions are assessed for their resilience to these factors. Implementing a diversified portfolio strategy can also reduce risk exposure. This involves balancing investments across different asset classes and geographic locations to cushion against localized downturns. Additionally, incorporating technology such as predictive analytics can enhance decision-making and risk assessment capabilities.

Adjusting **acquisition criteria** and **underwriting standards** is essential in this climate. Investors should refine their criteria to prioritize properties with strong income potential and sustainable growth prospects. It is advisable to incorporate stress testing in underwriting processes, simulating various economic scenarios to evaluate property performance under adverse conditions. This can help determine appropriate leverage levels, ensuring that debt obligations remain manageable even in downturns. Investors should also consider enhancing liquidity by maintaining higher cash reserves or exploring flexible financing options such as hard money loans.

Ultimately, real estate investors who embrace a strategic, data-driven approach can navigate the complexities of the 2026 market with confidence. By focusing on resilient investments and prudent risk management, they can capitalize on emerging opportunities and achieve sustainable growth.

Key Considerations for Investors

- For fix-and-flip strategies, target a holding cost of less than 10% of total project cost to maintain profitability in case of project delays.

- Aim for a spread risk of at least 20% between acquisition cost and expected sale price to cushion against market fluctuations.

- Establish a contingency plan that includes a 5% budget overrun on renovation costs to address unforeseen expenses.

- In buy-and-hold tactics, set a minimum cap rate target of 6% to ensure positive cash flow and justify investment risks.

- Project rent growth at a conservative 2-3% annually, considering current inflation trends and wage growth data.

- Ensure DSCR loans have a cushion of at least 1.25x to withstand temporary income disruptions.

- For bridge financing, negotiate draw schedules that align with project milestones to optimize cash flow management.

- Maintain a contingency reserve of 3-6 months of operating expenses to manage unforeseen financial pressures.

- Identify markets offering the best risk-adjusted returns by analyzing local economic indicators, focusing on regions with tech and healthcare job growth.

- Adopt a conservative underwriting approach by stress testing against a 5% increase in interest rates to gauge impact on cash flow and asset valuation.

- Encourage portfolio diversification by allocating at least 25% of the portfolio to emerging markets to balance risk and opportunity.

- Implement risk mitigation strategies, such as maintaining higher reserves and ensuring all properties have comprehensive insurance coverage to protect against unforeseen events.

By staying informed and adaptable, investors can position themselves to seize opportunities and mitigate risks effectively, ensuring long-term success in the dynamic real estate market.

Resources

External References

Disclaimer: This market analysis is for informational purposes only and should not be considered financial or investment advice. Market conditions can change rapidly. Consult with a qualified financial or lending professional before making any decisions.