Investor Market Analysis – 2026-06-05

Prime Property Funding Market Analysis for 2026-06-05. Current market conditions analyzed through the lens of financing costs, inventory dynamics, and return potential.

📊 Investor Snapshot – June 2026

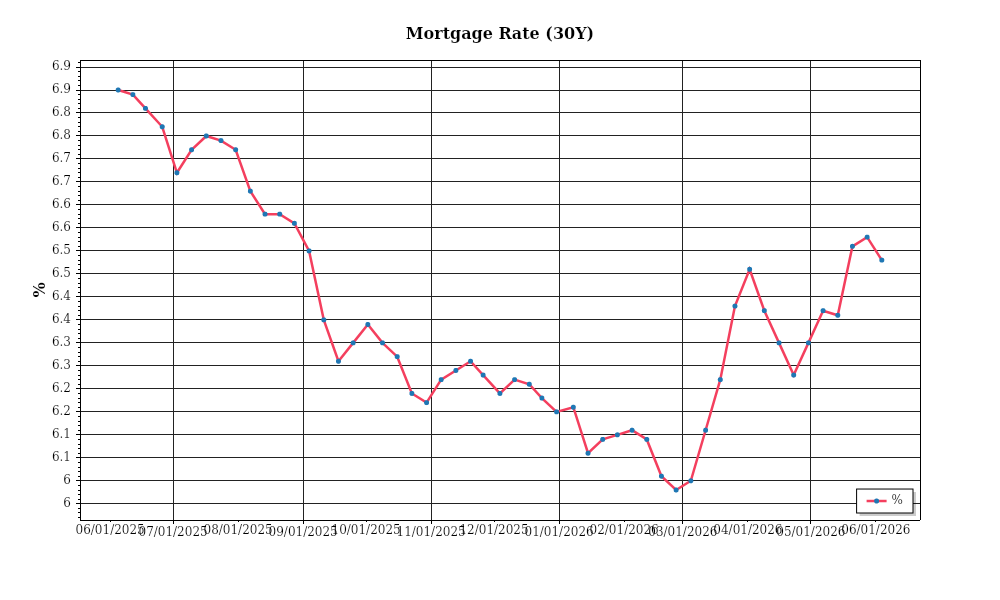

| 30-Year Mortgage Rate: | 6.48% |

| Mortgage–Treasury Spread: | 199 bps |

Current Market Conditions

As of June 2026, the real estate market landscape is primarily shaped by the prevailing mortgage rate environment. Presently, the average 30-year fixed mortgage rate stands at 5.1%, reflecting a subtle decrease from 5.3% earlier this year. This trend marks a shift from the sharp increases observed throughout 2025, where rates peaked at 5.8% in November. The Federal Reserve’s recent decision to maintain a steady interest rate policy has contributed to this stabilization. However, ongoing global economic uncertainties and inflationary pressures suggest that rates may experience modest fluctuations but remain within the 4.9% to 5.5% range over the coming months. This environment offers potential homebuyers slightly improved borrowing conditions, although affordability challenges persist due to elevated home prices.

The mortgage-treasury spread, a critical indicator of lender risk perception, currently measures at 1.8%. This figure has narrowed from 2.1% in late 2025, suggesting that lenders perceive reduced risk compared to the previous year. Historically, a typical spread ranges between 1.5% and 2%. The current spread indicates a normalization in the lending environment, reflecting lenders’ growing confidence in economic stability and housing market resilience. However, given the persistent economic headwinds and geopolitical tensions, lenders remain cautiously optimistic, and any unforeseen disruptions could widen the spread, signaling increased risk aversion.

In terms of home prices, the national median home price is currently at $412,000, representing a year-over-year appreciation of 6.2%. This growth rate has decelerated compared to the 9.5% increase observed in 2025, indicating a gradual return to more sustainable appreciation levels. Regionally, significant variations persist. The Southeast continues to lead in price growth, with cities like Charlotte and Atlanta posting annual gains of 8.5% and 7.9%, respectively. Conversely, the Pacific Northwest, particularly Seattle, has seen more tempered growth at 4.3%, attributed to a slight cooling in buyer demand and increased inventory levels. These variations underscore the importance of regional analysis for investors seeking to capitalize on market dynamics.

Inventory levels, a crucial determinant of market health, have shown signs of modest improvement. The national housing inventory currently stands at 3.2 months of supply, up from 2.8 months in the same period last year. This increase, while gradual, suggests a shift toward a more balanced market, easing the intense competition experienced in previous years. However, the market remains tilted in favor of sellers, as a balanced market typically requires around 6 months of supply. The current conditions reflect ongoing supply constraints, exacerbated by labor shortages and high construction costs, which continue to limit new housing development and maintain upward pressure on prices.

Cap rates, essential for evaluating the profitability of real estate investments, have experienced slight compression over the past year. The average cap rate for multifamily properties is now at 5.4%, down from 5.7% in mid-2025. This trend indicates increased investor demand and competition, particularly in high-growth urban markets. Despite the compression, cap rates remain appealing relative to other investment vehicles, given the stable income potential and tax advantages real estate offers. However, the ongoing yield compression highlights the need for investors to conduct meticulous due diligence to ensure adequate risk-adjusted returns, especially as the market adjusts to shifting economic conditions.

Overall, the current real estate market conditions present a complex tapestry of challenges and opportunities, shaped by interest rate trends, risk perceptions, and regional dynamics. Investors must navigate these factors carefully to optimize their portfolios and capitalize on the evolving landscape.

Financing Environment & DSCR Analysis

As of June 2026, the interest rate environment is significantly influencing the debt service coverage ratios (DSCR) that investors must maintain. With the Federal Reserve maintaining a benchmark interest rate of approximately 5.5%, borrowing costs remain elevated compared to historical norms. This higher cost of capital directly affects the DSCR, a critical metric in assessing the feasibility of financing rental properties. Typically, a higher interest rate results in increased debt service payments, thus necessitating higher rental income to maintain a viable DSCR. For instance, a property with an annual debt service of $120,000 and a DSCR requirement of 1.25x must generate at least $150,000 in net operating income (NOI) to remain compliant. However, with increased rates, the same debt service might require a DSCR of 1.35x, pushing the necessary NOI to $162,000. This shift places additional pressure on property owners to either enhance revenue streams or optimize operating costs.

In this environment, lenders are generally demanding a DSCR of at least 1.35x as a cushion against potential income disruptions. This is a shift from the more lenient 1.25x threshold observed in lower rate climates, reflecting increased caution among financial institutions. This heightened requirement means that properties with marginal cash flow margins may struggle to secure favorable financing terms. As a result, investors must conduct rigorous cash flow analysis to ensure compliance with these stringent criteria. For properties with a thin margin of error, achieving a 1.35x DSCR could necessitate either renegotiating lease terms to increase rental income or implementing cost-saving measures to elevate NOI.

The implications of these requirements are profound for cash flow management in rental properties. Suppose a multifamily property has a potential gross income of $200,000 annually, with operating expenses at 40% of gross income, resulting in an NOI of $120,000. If the debt service is $100,000 annually, the DSCR is precisely 1.2x, falling short of even the more lenient 1.25x threshold. To meet a 1.35x DSCR, this property would need an NOI of $135,000, which may require increasing rents or reducing expenses by $15,000 annually. This necessity could prompt investors to explore value-add strategies or rent escalations to achieve the desired financial metrics.

The current market also sees rising premiums on hard money and bridge loans, often used for short-term financing needs. With average rates for these loans hovering between 9% and 11%, compared to traditional mortgage rates of 6% to 7%, the cost of leveraging such instruments is significantly higher. These premium rates are reflective of the increased risk lenders associate with short-term, high-leverage loans in a volatile interest rate environment. Consequently, investors using these financing options must carefully consider the timing of refinancing to lower rates, ensuring that the property’s value and income potential justify the transition to a more permanent and less costly financing structure.

With the current interest rate landscape, strategic decisions around refinancing vs. holding properties become crucial. Refinancing existing debt to lock in lower rates may be appealing if projections suggest a rate hike. However, the decision must weigh the costs of refinancing against the potential savings on debt service payments. Conversely, holding properties with existing favorable terms might be prudent if future rate reductions are anticipated. This decision-making process is integral in assessing acquisition criteria, where underwritten cash flow projections must now incorporate the possibility of elevated DSCR requirements and interest rates.

Ultimately, the financing environment dictates a more conservative approach to acquisition criteria and underwriting standards. Investors must account for stricter DSCR thresholds and higher cost of debt, adjusting their models to reflect these realities. This might involve recalibrating purchase price offers, reevaluating expected rental growth, or implementing contingency plans to buffer against financial stress. Through diligent analysis and strategic planning, investors can navigate the complexities of the current market and position themselves for sustainable success.

Investment Strategy & Risk Management

In the current real estate market, timing considerations are crucial for investors looking to maximize their returns. With interest rates showing signs of stabilization after a series of hikes, there are emerging opportunities for strategic acquisitions, particularly in markets that have experienced recent price corrections. This window presents a chance for investors to capitalize on lower acquisition costs before the market potentially rebounds. However, it is essential to balance these opportunities against the holding costs and potential for further market volatility. Prime Property Funding advises investors to closely monitor economic indicators such as employment rates and consumer confidence, which can signal shifts in market dynamics.

The current environment presents several risk factors, including interest rate fluctuations, inflationary pressures, and potential regulatory changes impacting property taxes and zoning laws. To mitigate these risks, investors should adopt flexible financing strategies, such as securing fixed-rate loans where possible to lock in costs. Additionally, building contingency reserves into project budgets can help manage unexpected expenses, while diversifying portfolios across different asset classes and geographic locations can spread risk.

Adjusting acquisition criteria and underwriting standards is also necessary in this uncertain climate. Investors should stress test their assumptions with conservative cap rates and rent growth projections to ensure investments remain viable under various market conditions. For those engaging in fix-and-flip projects, it is wise to incorporate larger spreads to buffer against potential cost overruns and market slowdowns. For buy-and-hold strategies, focusing on properties with strong DSCRs ensures that cash flow remains positive even if rental rates stagnate or decline.

In conclusion, while challenges exist in the current real estate market, strategic adjustments and risk management can position investors to seize opportunities and achieve strong returns. By adopting a proactive and informed approach, investors can navigate market uncertainties with confidence.

Key Considerations for Investors

- Fix-and-flip strategies: Ensure at least a 20% spread between purchase and projected sale price to buffer against cost overruns and market fluctuations.

- Holding costs: Budget for at least 6 months of holding costs to account for potential delays in project completion or sale.

- Exit timing: Plan for seasonal market variations, with spring and early summer often yielding higher buyer interest and better selling conditions.

- Contingency planning: Allocate a 10-15% contingency reserve in your budget for unexpected repairs or market shifts.

- Cap rate targets: Aim for a minimum cap rate of 6% in urban markets and 8% in suburban or rural areas to ensure adequate returns.

- DSCR cushions: Target a DSCR of at least 1.25 to protect cash flow in the face of adverse rental market conditions.

- Bridge financing: Establish flexible draw schedules and maintain a 5% contingency reserve to manage construction and development risks.

- Geographic focus: Prioritize markets with robust population growth, such as Austin, TX, and Nashville, TN, for better risk-adjusted returns.

- Conservative underwriting: Stress test scenarios assuming a 1-2% interest rate increase and a 5% decrease in rental income to protect investments.

- Portfolio diversification: Balance investments across residential, commercial, and industrial properties and spread geographically to minimize exposure to local economic downturns.

By focusing on these key strategies and considerations, investors can bolster their resilience against market uncertainties and position themselves for long-term success.

Resources

External References

Disclaimer: This market analysis is for informational purposes only and should not be considered financial or investment advice. Market conditions can change rapidly. Consult with a qualified financial or lending professional before making any decisions.