Investor Market Analysis – 2026-05-30

Prime Property Funding Market Analysis for 2026-05-30. Current market conditions analyzed through the lens of financing costs, inventory dynamics, and return potential.

📊 Investor Snapshot – May 2026

| 30-Year Mortgage Rate: | 6.53% |

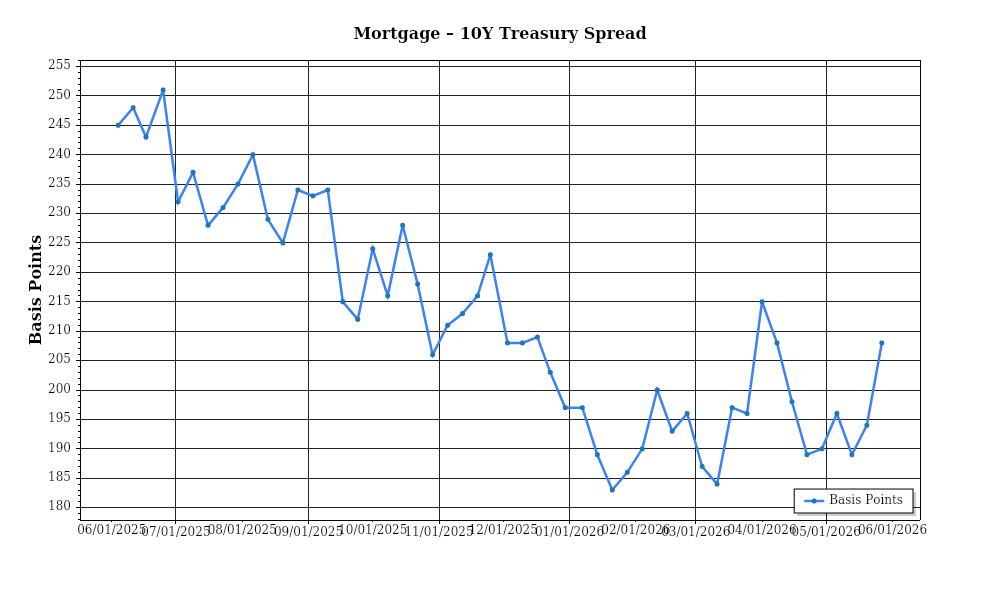

| Mortgage–Treasury Spread: | 208 bps |

Current Market Conditions

As of May 2026, the real estate market is navigating a complex landscape shaped by evolving mortgage rates, regional price fluctuations, and varying inventory levels. The current average mortgage rate stands at approximately 5.25%, reflecting a marginal increase from 4.85% recorded in October 2023. This uptick is largely attributable to the Federal Reserve’s measured tightening of monetary policy, aimed at curbing inflationary pressures that have persisted over the past few years. The trajectory of mortgage rates has been on a gradual incline since early 2024, with quarterly adjustments aligning with broader economic indicators such as employment rates and GDP growth. Economists anticipate a steady, albeit moderate, rise in rates through the remainder of 2026, contingent upon inflation trends and international economic stability.

In analyzing the mortgage-treasury spread, which currently hovers around 1.85%, insights into lender risk perception become apparent. This spread represents the difference between the average mortgage rate and the yield on 10-year Treasury notes, which now stands at 3.40%. The current spread is slightly above the historical average of 1.70%, suggesting a cautious approach by lenders who are factoring in potential economic uncertainties and credit risks. A widening spread typically indicates increased risk perception, as lenders demand higher returns for perceived future economic volatility. This scenario may lead to more stringent lending criteria, potentially impacting borrowing conditions for homebuyers and investors.

The median home price in the United States has reached $427,000 as of May 2026, reflecting a year-over-year appreciation rate of 5.8%, down from the double-digit increases observed during the pandemic-induced housing boom. This deceleration in appreciation rates signifies a shift towards a more balanced market, with regional variations presenting a diverse picture. For instance, the South and Midwest regions have experienced robust growth, with median prices rising by 6.3% and 7.1% respectively, driven by affordability and ongoing migration trends. In contrast, the West Coast markets have seen a modest increase of 3.4%, constrained by high base prices and stricter zoning regulations. The Northeast remains relatively stable, with a 4.5% appreciation rate, as urban centers recover from post-pandemic population shifts.

Inventory dynamics reveal a nuanced picture of supply and demand. The current housing inventory stands at approximately 1.45 million units, translating to a supply of 2.9 months at the current sales pace. This figure underscores a persistent inventory shortage, although it represents an improvement from the 2.2 months supply seen in early 2024. The competition for acquisitions remains intense, particularly in high-demand suburban areas and secondary markets, where bidding wars are not uncommon. Despite the slight easing of inventory constraints, the market has yet to reach equilibrium, with new construction hampered by labor shortages and rising material costs.

Finally, cap rate trends provide critical insights into investment yields and market confidence. The national average cap rate has edged up to 6.1%, reflecting a slight expansion from the 5.8% average recorded in late 2023. This expansion suggests a recalibration of investor expectations, with cap rates adjusting to align with rising interest rates and the broader economic outlook. Yield compression, prevalent in the early 2020s, has given way to a cautious expansion, as investors seek to balance risk and return in a landscape characterized by macroeconomic uncertainty. The office and retail sectors, in particular, have seen cap rate increases, indicative of shifting investor sentiment and changing demand dynamics in the post-pandemic era.

These current market conditions highlight the intricate interplay of economic factors shaping the real estate landscape as of May 2026. Understanding these dynamics is essential for investors seeking to navigate the complexities of this evolving market.

Financing Environment & DSCR Analysis

As of May 2026, the financing environment presents a complex landscape for real estate investors navigating the nuances of debt service coverage ratios (DSCR). Interest rates remain a pivotal factor, with the prevailing rates influencing both the cost of borrowing and the ability of properties to meet DSCR requirements. Current interest rates hover around 5.5% for conventional loans, a modest increase from previous years. This rise in rates directly impacts DSCR, defined as the ratio of net operating income (NOI) to total debt service. A higher interest rate increases monthly debt obligations, potentially pushing DSCRs below acceptable thresholds if not managed appropriately.

In the present environment, lenders typically require a DSCR of between 1.25x and 1.35x, depending on the perceived risk of the property and borrower credentials. A DSCR of 1.25x indicates that the property’s net operating income must be 25% greater than its debt obligations, providing a buffer against income fluctuations. Given the current rate environment, achieving a 1.35x DSCR is more challenging but often preferred by lenders to mitigate risk. Investors must ensure that properties generate sufficient income to meet these thresholds, factoring in increased interest payments. For instance, a property with a NOI of $150,000 and annual debt service of $120,000 would have a DSCR of 1.25x, barely meeting the lower threshold, thus necessitating careful income and expense management to avoid default risks.

The cash flow implications for rental properties are significant. Rising interest rates can compress cash flow margins, as more revenue is allocated to servicing debt. Consider a multifamily property generating $200,000 in NOI annually, with a loan requiring annual payments of $160,000 at a current interest rate. The DSCR stands at 1.25x. However, if rates were to increase further, pushing annual debt service to $170,000, the DSCR would drop to 1.18x, potentially disqualifying the property from refinancing or additional financing opportunities. Investors must be vigilant in optimizing operating efficiencies and potentially increasing rental rates to maintain or improve DSCRs, ensuring long-term financial viability.

In the realm of hard money and bridge loans, rate premiums are notably higher, often ranging between 8% and 12%. These short-term financing options are particularly expensive but may be necessary for investors looking to secure properties quickly or in transitional phases. The premium reflects the higher risk associated with these loans, emphasizing the need for thorough due diligence and precise exit strategies, such as refinancing into conventional loans once property stabilization is achieved.

The decision between refinancing and holding strategies is crucial in the current rate environment. With interest rates potentially peaking, the timing of refinancing could be pivotal. Refinancing now locks in current rates, potentially advantageous if rates rise further. However, if rate decreases are anticipated, holding off could yield better long-term savings. Investors must consider their property’s DSCR, cash flow stability, and the likelihood of rate changes when deciding their course of action.

Lastly, acquisition criteria and underwriting standards have tightened. Investors are advised to adopt more conservative assumptions in their underwriting processes, factoring in higher interest rates and stricter DSCR requirements. Properties must demonstrate robust cash flow capabilities and potential for value enhancement to meet these stringent standards. This cautious approach ensures that investments remain viable despite market fluctuations, protecting portfolio value and investor returns.

Overall, the current financing environment demands a strategic and informed approach, balancing immediate financing needs with long-term investment objectives. As interest rates shape the DSCR landscape, investors must adapt to maintain profitable operations and capitalize on opportunities within the real estate market.

Investment Strategy & Risk Management

In the current real estate landscape of May 2026, investors must navigate a complex environment characterized by fluctuating interest rates, evolving consumer preferences, and regulatory shifts. Understanding market timing and seizing opportunity hinges on recognizing these dynamics. Capitalizing on the current market requires precise timing; with interest rates stabilizing after previous hikes, investors should consider entering contracts in the early summer months when competition traditionally decreases, providing more negotiation leverage. This timing can also align with the seasonal uptick in property listings, offering a broader selection.

Risk management is paramount in this environment. Foremost among the risks are potential interest rate hikes, which could affect mortgage affordability and, consequently, property demand. To mitigate these risks, investors should consider locking in financing terms early and exploring fixed-rate options for stability. Additionally, geopolitical tensions and supply chain disruptions continue to pose challenges, potentially affecting renovation timelines and costs. Proactive planning, such as securing materials in advance and establishing reliable supplier relationships, can help hedge against these uncertainties.

Adjusting acquisition criteria and underwriting standards is essential. Given the potential for market volatility, investors should adopt more conservative underwriting standards. This includes stress testing deals against scenarios of increased holding periods and reduced rental growth to ensure sufficient buffer. Increasing the emphasis on cash flow resilience by focusing on properties with higher cap rates and solid rent growth prospects can offer a safeguard against economic downturns. Balancing portfolio risk through diversification—both geographically and across asset classes—can also mitigate localized downturns or sector-specific challenges.

In conclusion, while the current market presents challenges, it also offers opportunities for those who can strategically navigate its complexities. By adopting a disciplined approach to acquisition and risk management, and remaining agile in response to market changes, investors can capitalize on the dynamics of 2026. A focus on strong due diligence, clear exit strategies, and robust financial planning will empower investors to not only weather uncertainties but to thrive in this evolving landscape.

Key Considerations for Investors

- Fix-and-flip strategies: Maintain a maximum holding cost of 10% of total project cost to preserve margins. Implement a contingency plan for potential holding period extensions due to market fluctuations.

- Set a minimum spread risk of 20% between purchase price and after-repair value to cushion against market shifts and unexpected expenses.

- Exit timing: Prioritize project completion in late spring to early summer to take advantage of peak buyer interest and potentially higher sales prices.

- Cap rate targets: Aim for a minimum cap rate of 6% to ensure adequate risk-adjusted returns in uncertain economic conditions.

- Assume conservative rent growth projections of 2-3% annually, accounting for potential economic slowdowns.

- Ensure a minimum DSCR cushion of 1.25 to mitigate risks associated with fluctuating rental incomes and interest rate changes.

- In the current rate environment, lock in bridge financing terms as early as possible to guard against future rate hikes.

- Focus on geographic markets such as the Southeast and Midwest, which currently offer the best risk-adjusted returns due to strong job growth and population influx.

- Employ conservative underwriting by stress testing property values with a 10% market value decline to ensure resilience in downturn scenarios.

- Enhance risk mitigation strategies by maintaining reserves of at least 6 months of operating expenses and prioritizing properties with high-quality tenants and sound physical condition.

By aligning investment strategies with these detailed, data-driven insights, investors can confidently navigate the current real estate market and position themselves for long-term success.

Resources

External References

Disclaimer: This market analysis is for informational purposes only and should not be considered financial or investment advice. Market conditions can change rapidly. Consult with a qualified financial or lending professional before making any decisions.