Investor Market Analysis – 2026-05-29

Prime Property Funding Market Analysis for 2026-05-29. Current market conditions analyzed through the lens of financing costs, inventory dynamics, and return potential.

📊 Investor Snapshot – May 2026

| 30-Year Mortgage Rate: | 6.53% |

| Mortgage–Treasury Spread: | 205 bps |

Current Market Conditions

As of May 2026, the mortgage rate environment is characterized by a stabilization in interest rates after a period of volatility. The average 30-year fixed mortgage rate stands at 5.25%, maintaining a steady position compared to the 5.15% seen at the start of the year. This stability comes after a period of upward pressure, peaking at 5.45% in early March. The Federal Reserve’s recent decisions to maintain the federal funds rate in its current range have contributed to this steadiness. Despite the relative calm, the market remains sensitive to macroeconomic indicators such as inflation rates and employment data, which could prompt future rate adjustments. The current trajectory suggests that while rates may see modest increases, significant hikes are unlikely in the short term, providing some assurance to borrowers and investors about financing conditions.

The spread between mortgage rates and the 10-year treasury yield is an important indicator of lender risk perception. Currently, this spread is approximately 1.9%, slightly above the historical average of 1.7%. This elevated spread indicates that lenders are pricing in a higher risk premium, reflecting uncertainties in the broader economic environment and housing market stability. The persistence of geopolitical tensions and fluctuating economic data contribute to this cautious stance. In practical terms, this suggests that lenders are maintaining stringent borrowing criteria, potentially impacting loan accessibility for certain segments of the market. Investors should consider this cautious lending environment when assessing potential acquisitions and financing strategies.

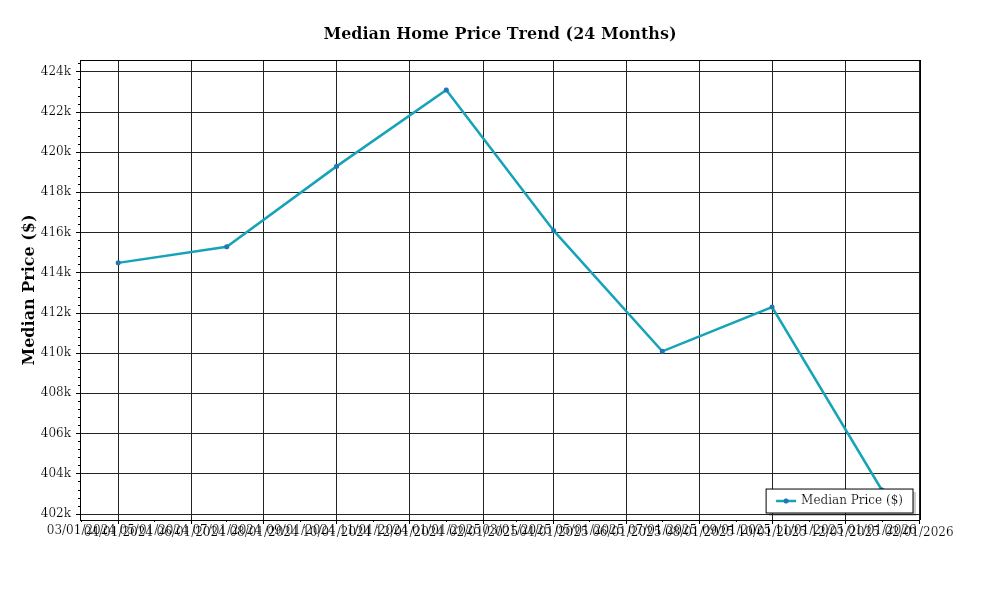

The median home price in the United States has reached $420,000, marking a year-over-year appreciation rate of approximately 4.2%. This rate represents a deceleration from the previous year’s 6.8% increase, suggesting a cooling in the rapid home price growth observed during the pandemic years. Regional variations are notable, with the Sun Belt cities such as Austin and Phoenix experiencing above-average increases of 6% and 5.5% respectively, driven by strong demographic trends and economic growth. In contrast, some Midwestern markets have seen more modest gains of around 2%. This regional divergence underscores the importance of localized market analysis for investors, as areas with robust economic fundamentals continue to offer better appreciation prospects.

Inventory dynamics continue to play a crucial role in shaping market conditions. Nationally, the supply of homes for sale stands at 3.4 months, an increase from 2.7 months a year ago, reflecting an improvement in inventory levels. However, this remains below the balanced market threshold of 5-6 months, indicating continued competition among buyers. While the increase in listings provides more options for buyers, the market is still skewed towards sellers, particularly in high-demand regions. This imbalance is likely to sustain upward pressure on prices and maintain competitive acquisition scenarios, with multiple offers still prevalent in desirable locations.

Cap rate trends provide insights into commercial real estate market conditions, with current average cap rates hovering around 5.75%, slightly compressing from 5.85% last year. This compression suggests an increase in property values relative to income, driven by robust demand for income-generating assets and limited supply in prime locations. Yield compression is particularly evident in sectors like multifamily and industrial properties, where investor interest remains strong due to resilient demand fundamentals. Investors should be aware that while lower cap rates can indicate higher asset values, they also imply lower initial yields, necessitating careful consideration of long-term growth prospects and income stability. As market conditions evolve, these metrics will be crucial in assessing the attractiveness of investment opportunities across various real estate sectors.

Financing Environment & DSCR Analysis

As of May 2026, the financing environment has been characterized by a steady yet moderate increase in interest rates, a trend that has persisted since early 2024. This rise in rates has a significant impact on Debt Service Coverage Ratios (DSCR), a critical measure for assessing a property’s ability to cover its debt obligations. The current interest rate environment has seen average commercial mortgage rates hovering around 6.5%, which poses a challenge for investors reliant on debt financing. Higher interest rates increase monthly debt service payments, thereby compressing the DSCR. For instance, a property generating a net operating income (NOI) of $120,000 annually with a debt service of $100,000 would have a DSCR of 1.20x. However, with higher rates pushing debt service to $110,000, the DSCR drops to approximately 1.09x, highlighting the pressure on maintaining adequate coverage.

In this current environment, lenders have adjusted their DSCR requirements to safeguard against increased financial risk. While pre-pandemic thresholds hovered around 1.25x, the industry is now trending towards a more conservative 1.35x for new acquisitions. This tightening reflects lenders’ need to buffer against potential default risks, given the increased cost of borrowing. Properties that fail to meet this updated threshold might find it challenging to secure favorable financing terms, forcing investors to either increase equity contributions or seek properties with stronger cash flow potential. This shift compels a reevaluation of acquisition strategies, as the ability to meet these higher DSCR requirements becomes a critical factor in determining the viability of investment opportunities.

The cash flow implications for rental properties are profound. Consider a multifamily property previously financed at a 4.5% interest rate with an annual debt service of $90,000 and an NOI of $112,500, yielding a DSCR of 1.25x. With current interest rates at 6.5%, the annual debt service increases to $105,000, reducing the DSCR to approximately 1.07x. This drop below the typical 1.35x threshold necessitates an increase in NOI by at least $30,750 to restore the DSCR to 1.35x, assuming other variables remain constant. Landlords may need to explore rent increases, operational efficiencies, or cost-cutting measures to bridge this gap, although these strategies must be balanced against market conditions and tenant retention rates.

The premium for hard money and bridge loans in the current market reflects the risk undertaken by lenders in extending short-term, high-interest financing. Rates for these loans are typically 2-4 percentage points higher than traditional financing, often surpassing 10%. While these loans offer flexibility and quicker access to capital, the cost is significant, impacting the overall profitability of a project. Investors opting for this route must ensure that the underlying asset has a clear path to stabilization or refinance at more favorable terms before the loan term expires.

Given the current rate environment, the decision to refinance versus hold is pivotal. While refinancing can lock in lower rates in anticipation of further hikes, it comes with transaction costs and potential prepayment penalties. Conversely, holding onto existing financing might be beneficial if the rates are historically low or if market conditions indicate a potential rate decrease. This decision impacts acquisition criteria, where investors are now more focused on underwriting standards that emphasize stress-tested financial models to absorb potential rate increases. Properties with stable cash flows, low leverage, and room for operational improvements are more attractive, as they offer a buffer against the volatility of the financing environment.

In summary, the current financing landscape demands rigorous financial scrutiny and strategic foresight. Investors must navigate between tighter DSCR requirements, elevated debt costs, and a nuanced understanding of market dynamics to optimize their portfolios in a rising rate environment.

## Investment Strategy & Risk Management

In the current real estate climate, market timing is crucial to capitalize on investment opportunities while minimizing exposure to risk. The market in May 2026 shows signs of stabilization following a period of volatility, which presents both opportunities and challenges for investors. With interest rates having shown gradual increases over the past year, investors need to be particularly discerning about when and where to deploy capital. Identifying submarkets and property types that are undervalued or poised for growth is critical. Areas that have recently undergone infrastructure improvements or have announced new business developments may offer significant upside potential.

Risk factors in the current environment include potential regulatory changes, fluctuating interest rates, and economic uncertainty. To manage these risks, investors should consider employing hedging strategies such as locking in current rates, diversifying across asset classes, and maintaining a robust contingency fund. Additionally, staying informed about policy changes and economic indicators will help in adjusting strategies proactively. Engaging in comprehensive due diligence and stress testing underwriting assumptions for various economic scenarios can further mitigate risks.

Adjusting acquisition criteria and underwriting standards is essential in this evolving market. Investors should tighten criteria to focus on properties with strong fundamentals, such as high demand locations and solid rental income history. Underwriting should incorporate more conservative assumptions about rent growth and vacancy rates, ensuring that investments remain viable even if market conditions worsen. For Prime Property Funding’s clients, maintaining a healthy debt service coverage ratio (DSCR) is imperative, especially given the potential for fluctuating rental incomes and increased holding costs.

Overall, the strategic approach in 2026 should emphasize a balance between opportunistic and cautious investment. By focusing on thorough risk assessment and diligent market analysis, investors can position themselves for both stability and growth.

### Key Considerations for Investors

– **Fix-and-flip strategies**: Aim for projects with a minimum spread of 20% between acquisition and potential sale prices to account for holding costs and unexpected expenses. Implement contingency planning for project delays that could affect exit timing.

– **Buy-and-hold tactics**: Target properties with a cap rate of at least 6% to ensure adequate cash flow. Assume conservative rent growth of 2-3% annually in underwriting to mitigate optimistic projections.

– **DSCR loans**: Maintain a DSCR cushion of at least 1.25 to withstand potential drops in rental income and increased interest rates.

– **Bridge financing**: Stay attuned to the rate environment and ensure draw schedules are flexible to accommodate project needs. Maintain contingency reserves of at least 10% of total project costs.

– **Market timing**: Prioritize acquisition opportunities during the fall and winter months when holding costs may be lower due to reduced competition.

– **Geographic focus**: Focus on secondary markets with strong economic indicators, such as population growth and employment rates, for better risk-adjusted returns.

– **Conservative underwriting**: Stress test property performance against scenarios of a 10% drop in rental income and a 5% increase in vacancy rates.

– **Portfolio diversification**: Balance investments across residential and commercial properties and diverse geographic locations to reduce exposure to market-specific risks.

– **Risk mitigation**: Ensure adequate reserves equivalent to three months of operating expenses and secure comprehensive insurance coverage. Prioritize properties with strong tenant profiles and good condition to minimize maintenance costs.

With a careful, informed approach to investment, Prime Property Funding clients can navigate the complexities of the 2026 market with confidence, securing profitable ventures while effectively managing risk.

Resources

External References

Disclaimer: This market analysis is for informational purposes only and should not be considered financial or investment advice. Market conditions can change rapidly. Consult with a qualified financial or lending professional before making any decisions.