Investor Market Analysis – 2026-05-28

Prime Property Funding Market Analysis for 2026-05-28. Current market conditions analyzed through the lens of financing costs, inventory dynamics, and return potential.

📊 Investor Snapshot – May 2026

| 30-Year Mortgage Rate: | 6.51% |

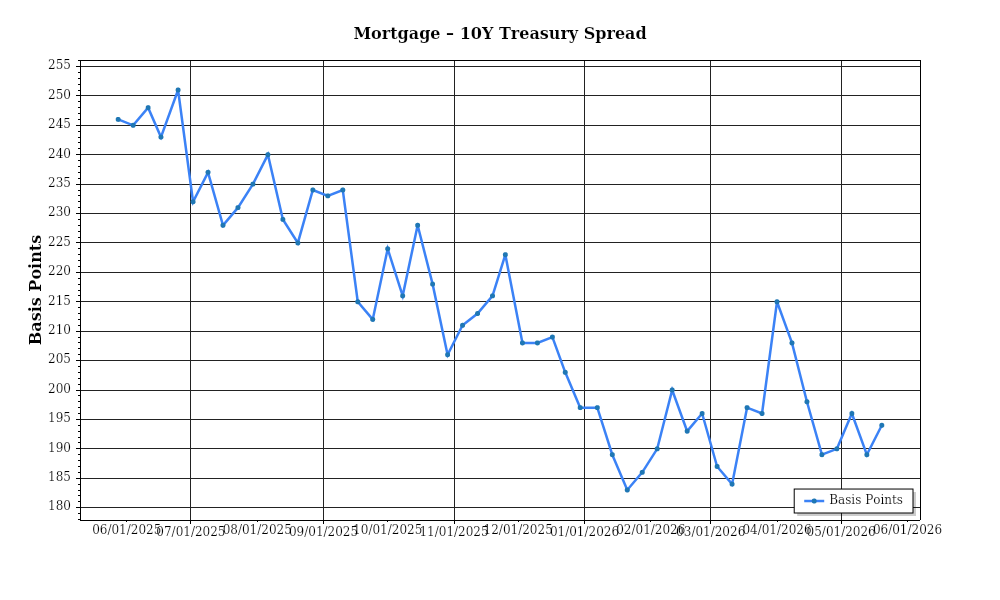

| Mortgage–Treasury Spread: | 201 bps |

Current Market Conditions

As of May 2026, the real estate market is deeply influenced by the current mortgage rate environment. The average 30-year fixed mortgage rate stands at 5.75%, reflecting a slight increase from the 5.50% seen in the previous quarter. This uptick is indicative of the Federal Reserve’s ongoing monetary tightening policy aimed at curbing inflation, which has seen benchmark rates increase by 50 basis points since December 2025. The mortgage rate trajectory remains upward, albeit at a moderated pace, as inflationary pressures begin to abate. This environment is crucial for investors, as higher mortgage rates typically translate to increased borrowing costs, potentially dampening demand among homebuyers and impacting overall market liquidity.

The mortgage-treasury spread, which currently hovers around 180 basis points, provides further insights into lender risk perception. Historically, a spread of 150 basis points is considered indicative of a stable market. The current wider spread suggests heightened risk aversion among lenders, possibly due to economic uncertainties or anticipated defaults. This broader spread can be attributed to the recent fluctuation in the 10-year Treasury yield, which has increased to 3.95% from 3.70% over the past six months. Such dynamics imply that lenders are demanding a higher risk premium, signaling caution in the credit markets and potentially tightening lending criteria.

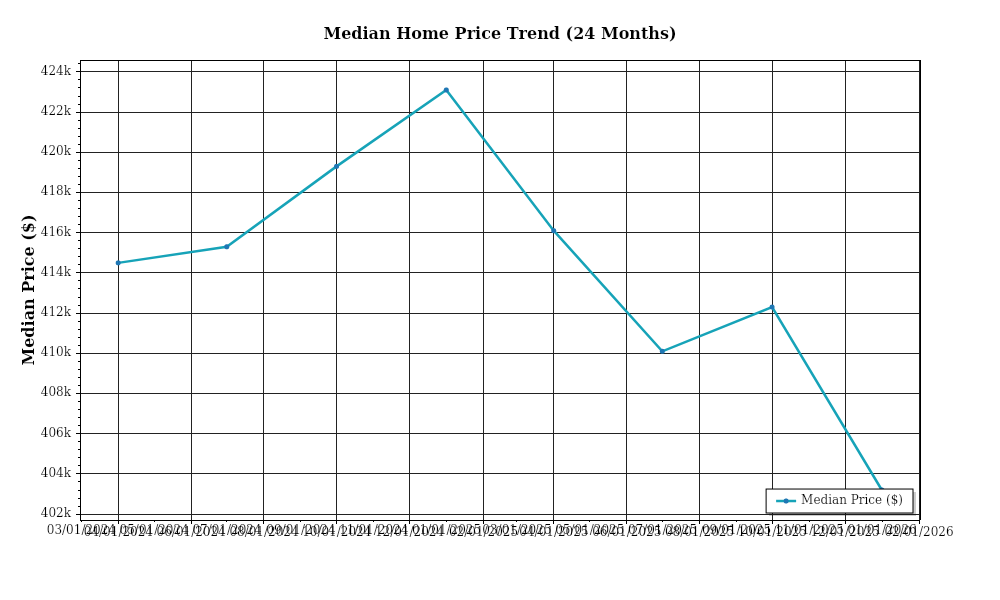

Turning to median home price trends, the national median home price has reached $415,000, marking a 3.8% year-over-year increase. This appreciation rate is modest compared to the double-digit gains observed in the early 2020s, indicating a more balanced market. Regional variations remain pronounced, with the Sun Belt cities like Austin and Phoenix experiencing higher appreciation rates of 5.5% and 5.2%, respectively, due to continued population inflows and economic growth. Conversely, the Midwest markets such as Cleveland and Detroit see slower growth rates around 2%, reflecting more stable but less dynamic economic conditions. These trends highlight the importance for investors of focusing on regional market dynamics and demographic shifts when assessing investment opportunities.

Inventory dynamics play a critical role in shaping the current market conditions. Nationwide, inventory levels have slightly increased, with an active listing count at 1.35 million, up from 1.25 million a year ago. This rise is largely attributed to new construction completions and reduced buyer activity due to higher mortgage rates. Despite this increase, the market remains competitive, with an average of 45 days on the market for homes, down from 60 days last year. The supply-demand balance is slowly inching towards equilibrium, though certain metropolitan areas continue to experience supply shortages. For instance, San Diego and Miami report inventory levels at 2.5 months of supply, significantly below the 6-month benchmark of a balanced market, indicating ongoing competitive pressures and opportunities for strategic acquisitions.

Cap rate trends are equally telling, with the average cap rate for multifamily properties currently at 5.2%, reflecting a slight expansion from 4.8% in early 2025. Yield compression, which characterized much of the past decade, is beginning to reverse, aligning with the broader economic environment of rising interest rates. This expansion in cap rates suggests that investors are recalibrating their expectations for returns in light of increased borrowing costs and potential economic headwinds. However, this trend varies by region and asset class, with suburban and secondary markets seeing more pronounced cap rate expansions compared to urban centers. For investors, the current cap rate trends underscore the need for thorough due diligence and careful market analysis to identify assets that offer the best risk-adjusted returns.

In conclusion, the real estate market as of May 2026 presents a complex tapestry of conditions influenced by macroeconomic factors, regional trends, and evolving market dynamics. Investors must remain vigilant, leveraging data-driven insights to navigate this landscape effectively.

Financing Environment & DSCR Analysis

As of May 2026, the financing environment is characterized by a fluctuating interest rate landscape. Current interest rates, which have stabilized at approximately 5.25% after a series of hikes over the past couple of years, significantly impact the Debt Service Coverage Ratios (DSCR) for real estate investors. Higher interest rates increase borrowing costs, which in turn affect DSCR—a critical metric for lenders assessing the risk associated with lending to property investors. A higher interest rate decreases the net operating income (NOI) relative to the debt service, thereby reducing the DSCR. This situation necessitates careful evaluation by investors, as a decreased DSCR could impair the ability to secure financing or refinance existing loans.

In this current environment, lenders typically require a DSCR of at least 1.25x to 1.35x for standard property acquisitions. This range is indicative of lender caution and the need for a buffer against income fluctuations or unexpected expenses. For a property generating a monthly NOI of $10,000, for instance, a 1.25x DSCR would require that the monthly debt service does not exceed $8,000. Conversely, with a 1.35x requirement, the debt service must remain below approximately $7,407. This threshold impacts the maximum loan amount investors can secure, as the loan size must be aligned with the DSCR requirements given the expected NOI.

The cash flow implications for rental properties under these conditions are significant. Consider a rental property with an NOI of $10,000 per month and a mortgage payment of $8,500. With a DSCR of 1.18x, this property would fall short of the 1.25x minimum threshold, necessitating either a reduction in monthly debt service through refinancing or an increase in NOI through rent adjustments or operational efficiencies. This disparity emphasizes the need for investors to maintain a healthy margin in their cash flow projections, ensuring they can meet both lender requirements and unforeseen financial challenges.

In the current market, hard money and bridge loan rate premiums are particularly pronounced, often exceeding the standard mortgage rates by 300 to 500 basis points. These short-term financing solutions, with rates often between 8% and 10%, provide flexibility for investors needing quick capital but come at a higher cost. The premium rates demand a higher DSCR to compensate for the increased risk, which further impacts the feasibility of such financing options. Investors must weigh the cost of these loans against the potential return on investment and the speed at which they can execute their property strategies.

The decision to refinance or hold existing properties is heavily influenced by the current rate environment. With rates stabilizing, the timing of refinancing becomes a strategic decision. Investors must consider the break-even point for refinancing costs relative to the reduction in monthly payments. For properties with loans originated at higher rates during the peak of recent hikes, refinancing could yield immediate cash flow improvements, provided the DSCR remains favorable. Conversely, holding could be advantageous if further rate drops are anticipated, allowing investors to capitalize on future lower rates without incurring additional transaction costs.

Finally, the impact on acquisition criteria and underwriting standards is profound. With stricter DSCR requirements in place, underwriters are increasingly focusing on detailed cash flow analyses and conservative revenue projections. This shift necessitates thorough due diligence and robust financial modeling on the part of investors. Properties with strong, stable income streams and potential for rent increases are more attractive, as they are better positioned to meet DSCR thresholds and withstand economic fluctuations. Consequently, investors must be diligent in selecting properties with resilient financials and potential for value appreciation, ensuring alignment with current underwriting standards and market conditions.

Investment Strategy & Risk Management

In the current real estate landscape, timing is a critical factor for maximizing investment returns. As we move through 2026, market conditions reflect a delicate balance between rising interest rates and persistent demand in certain sectors. Investors must be astute in identifying opportunities that align with their risk tolerance and investment objectives. Given the market’s cyclical nature, targeting acquisitions during the less competitive winter months could yield better pricing. Additionally, the anticipation of interest rate stabilization in mid-2026 provides a window for locking in financing before rates potentially climb again.

The current environment presents several risk factors, including economic uncertainty, fluctuating interest rates, and regional disparities in market recovery. To mitigate these risks, investors should employ a multi-pronged approach. Diversifying across asset types and geographies can help cushion against localized downturns. Moreover, conservative underwriting standards, such as stress testing cash flows under different economic scenarios, are crucial. Implementing a robust contingency planning strategy, with ample reserves and insurance coverage, can safeguard against unforeseen disruptions.

Adjusting acquisition criteria in this environment necessitates a refined focus on value-add opportunities and properties with strong cash flow potential. For fix-and-flip ventures, ensuring a substantial spread between purchase price and after-repair value (ARV) is imperative. In buy-and-hold scenarios, prioritizing assets with high cap rates and potential for rent growth will enhance long-term viability. Additionally, ensuring that debt service coverage ratios (DSCR) remain comfortably above 1.25 will provide a cushion against revenue fluctuations.

Prime Property Funding’s role as a financier positions it uniquely to support investors through tailored loan products that align with strategic goals. By maintaining flexibility in lending terms and offering competitive DSCR loans, we enable investors to capitalize on opportunities while managing risk effectively. In conclusion, the ability to adapt strategies, maintain rigorous financial discipline, and stay informed about market dynamics will empower investors to thrive in this evolving landscape.

Key Considerations for Investors

- For fix-and-flip strategies, target a minimum spread of 20% between purchase price and ARV to ensure profitability after costs.

- Limit holding costs by aiming for a turnaround time of less than 6 months to minimize exposure to market volatility.

- Utilize contingency planning by setting aside 10% of the project budget to cover unexpected expenses.

- Set cap rate targets at a minimum of 6% for buy-and-hold properties to ensure attractive returns relative to financing costs.

- Factor in a rent growth assumption of 3-5% annually to project future income streams realistically.

- Maintain a DSCR cushion of at least 1.25 to safeguard against income interruptions.

- In the current rate environment, consider bridge financing with a maximum interest rate of 7% to manage cost of capital.

- Develop a draw schedule that aligns with project milestones, ensuring efficient cash flow management.

- Focus on geographic markets like the Southeast and Southwest regions, which offer robust growth prospects and favorable risk-adjusted returns.

- Implement stress testing by modeling worst-case scenarios, adjusting assumptions for vacancy rates and operating costs to ensure resilience.

By applying these strategies, investors can confidently navigate the complexities of the current market, leveraging opportunities while mitigating risks.

Resources

External References

Disclaimer: This market analysis is for informational purposes only and should not be considered financial or investment advice. Market conditions can change rapidly. Consult with a qualified financial or lending professional before making any decisions.