Investor Market Analysis – 2026-05-27

Prime Property Funding Market Analysis for 2026-05-27. Current market conditions analyzed through the lens of financing costs, inventory dynamics, and return potential.

📊 Investor Snapshot – May 2026

| 30-Year Mortgage Rate: | 6.51% |

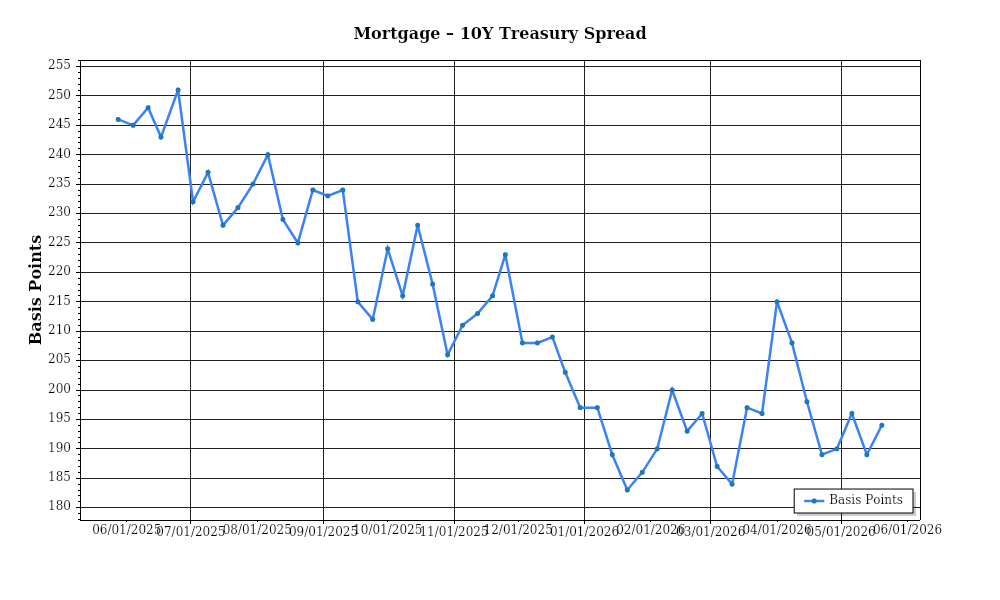

| Mortgage–Treasury Spread: | 195 bps |

Current Market Conditions

The mortgage rate environment as of May 2026 is a critical factor in understanding the current real estate landscape. Mortgage rates have seen a moderate increase over the past year, with the average 30-year fixed mortgage rate now hovering around 5.2%, up from 4.6% in May 2025. This shift can be attributed to ongoing monetary policy adjustments by the Federal Reserve, which has gradually raised interest rates to curb inflation that spiked post-pandemic. Over the past six months, mortgage rates have fluctuated between 5.0% and 5.4%, indicating a relatively stable but elevated rate environment. Analysts predict that rates will likely stabilize in the mid 5% range for the rest of the year, assuming inflationary pressures continue to ease and economic growth remains steady. This rate increase impacts affordability and borrowing costs but also suggests a healthier economy and potentially less frothy asset valuations.

The mortgage-treasury spread, a key indicator of lender risk perception, currently stands at approximately 1.75%. This spread has narrowed from a peak of 2.1% in early 2025, suggesting that lenders perceive a lower risk in the housing market compared to last year. Historically, a spread above 2% indicates heightened risk aversion among lenders, often due to economic uncertainty or expected volatility in housing prices. The current narrower spread reflects increased confidence in the market’s stability, driven by a robust labor market and steady economic growth. This confidence is bolstered by the Federal Reserve’s signals of a steady monetary policy path, reducing the likelihood of abrupt changes in borrowing costs.

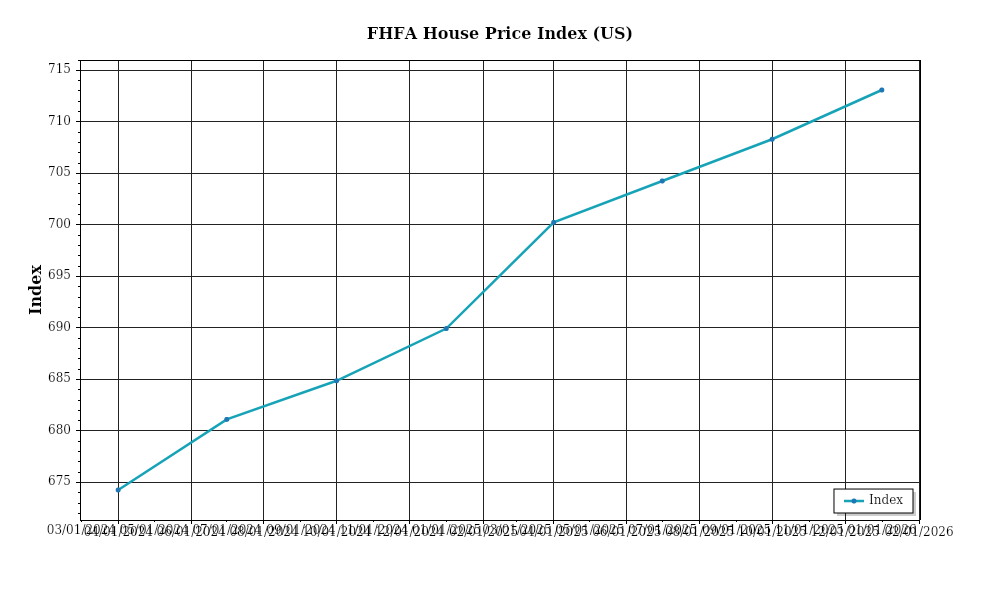

Median home prices have continued their upward trajectory, with the national median home price reaching $437,000 in May 2026, marking a 6.5% year-over-year increase from $410,000 in May 2025. This appreciation is slightly lower than the double-digit increases seen in the previous years, indicating a cooling but still robust market. Regionally, the South and Midwest have experienced the highest appreciation rates, with cities like Austin and Nashville seeing increases of 8% and 7.5%, respectively. Meanwhile, coastal markets like San Francisco and New York exhibit more modest gains of around 4%, reflecting market saturation and affordability constraints. These regional variations highlight the continued demand for more affordable and high-growth areas, as well as a shift in buyer preferences towards secondary and suburban markets.

Inventory dynamics are showing signs of gradual improvement, though supply remains tight. Current housing inventory levels are approximately 2.8 months of supply, a slight increase from 2.5 months a year earlier. This increase, although modest, suggests a slowly improving balance between supply and demand. However, inventory remains below the ideal balanced market threshold of 5-6 months, indicating ongoing competitive pressures in buyer markets. The competition for acquisitions remains fierce, particularly in the lower and mid-market segments where affordability concerns drive demand. This competition is further fueled by investors seeking rental properties, as rental markets remain strong.

Cap rates, reflecting the yield on real estate investments, have remained fairly stable, currently averaging around 5.4% nationally. This represents a slight compression from 5.6% a year ago, driven by strong demand for income-producing properties and a general appetite for real assets as a hedge against inflation. Yield compression is most pronounced in multifamily and industrial sectors, where cap rates are as low as 4.8% in top-tier markets due to high investor interest and strong leasing fundamentals. In contrast, retail and office sectors show more variability, with cap rates in the 5.5%-6.5% range, reflecting ongoing uncertainty about post-pandemic occupancy trends and retail consumption patterns. This cap rate stability suggests that while yields are compressed, the real estate market remains attractive for investors seeking stable returns amidst broader market volatility.

Financing Environment & DSCR Analysis

In the current real estate financing environment of May 2026, interest rates remain elevated, significantly affecting the Debt Service Coverage Ratios (DSCR) crucial for investors evaluating rental properties. The DSCR, a metric used to assess a property’s ability to cover its debt obligations, is directly impacted by interest rates. Higher rates increase the cost of borrowing, which in turn raises monthly debt service payments. For instance, a property with a mortgage rate of 6% compared to 4% results in higher monthly obligations, thus lowering the DSCR. This environment requires investors to ensure that their properties can generate enough income to maintain a favorable DSCR, typically above 1.25x, to secure financing. However, lenders are increasingly favoring a threshold of 1.35x in light of the current rate volatility, pushing investors to enhance their income streams or reduce debt levels to meet these stricter requirements.

The move from a DSCR requirement of 1.25x to 1.35x necessitates a re-evaluation of cash flow strategies. For example, a property generating $10,000 in monthly income with a 1.25x DSCR supports up to $8,000 in debt servicing. However, with a 1.35x requirement, the same income only supports approximately $7,407 in debt payments, necessitating a reduction in leverage or an increase in rental income. Investors need to focus on boosting rental yields to maintain compliance with stricter lending standards. This could involve strategic property improvements or targeting high-demand rental markets to justify higher rents, which are essential to sustain cash flow and meet DSCR expectations.

In the current market, hard money and bridge loan rates carry significant premiums due to the increased risk associated with short-term lending amidst economic uncertainty. These rates are typically 2-4% higher than conventional loans, reflecting lenders’ demand for higher returns to offset potential risks. For a $500,000 loan, a 2% premium equates to an additional $10,000 per annum in interest costs. This premium can heavily affect cash flow and DSCR, especially for investors relying on these financing options as interim solutions before refinancing into long-term products. As such, investors must carefully calculate these additional costs when considering short-term financing as part of their acquisition strategy.

The decision to refinance or hold properties in this rate environment is complex. On one hand, refinancing at current rates might lock in higher costs compared to waiting for a potential rate decrease. However, delaying could also risk exposure to further rate hikes. For investors, the decision hinges on individual DSCR metrics and cash flow projections. For instance, if a property currently meets the 1.35x DSCR threshold comfortably, holding off on refinancing might be viable. Conversely, if cash flow is tight, locking in current rates could provide stability at the expense of higher short-term interest costs. This strategic decision requires a comprehensive analysis of market trends and individual property performance metrics.

Finally, the prevailing rate environment influences acquisition criteria and underwriting standards. Investors must adjust their expectations and strategies, focusing on properties with robust cash flow potential to meet enhanced DSCR requirements. Underwriting standards now incorporate stricter income verification and stress testing under higher interest rates to ensure properties can withstand financial pressures. This scenario demands investors perform detailed cash flow analyses and remain vigilant about potential rate fluctuations, ensuring properties can consistently meet debt obligations under various economic conditions. This meticulous approach is crucial for maintaining portfolio stability and profitability in a challenging financing landscape.

Investment Strategy & Risk Management

As we approach mid-2026, real estate investors are navigating a landscape marked by varying economic indicators and geopolitical uncertainties. Market timing remains critical, with opportunities emerging in both undervalued properties and markets poised for appreciation. Investors should focus on identifying properties in regions with strong economic fundamentals and infrastructure projects that promise future growth. Areas with recent population growth or tech sector expansion, for instance, offer lucrative entry points and the potential for rapid returns.

However, such opportunities come with inherent risks. Interest rates have stabilized but remain higher than pre-pandemic levels, impacting borrowing costs and profit margins. To mitigate these risks, investors should employ rigorous stress testing in their financial models, accounting for potential increases in interest rates and operational costs. Diversifying portfolios across multiple geographic markets and asset classes can also cushion against localized downturns. Employing a conservative approach to leverage, with a preference for fixed-rate financing, can protect against interest rate volatility.

Adjusting acquisition criteria and underwriting standards is crucial in this environment. Investors should prioritize properties with strong cash flow potential, even if it means accepting lower immediate returns. Targeting a higher Debt Service Coverage Ratio (DSCR) can provide a buffer against revenue fluctuations. Additionally, incorporating contingency reserves into financial planning can address unexpected repairs or tenant defaults, safeguarding profitability. Underwriting should also include detailed market analyses to identify neighborhoods with undervalued properties and emerging demand trends.

Strategically, Prime Property Funding’s focus on hard money loans, fix-and-flip financing, and DSCR loans offers a robust approach to capitalizing on current market conditions. By emphasizing quick turnaround projects in the fix-and-flip segment and stabilizing cash flows through DSCR loans, investors can balance risk and reward effectively. As the market continues to evolve, staying informed and flexible in strategy will empower investors to seize opportunities and secure consistent returns.

Key Considerations for Investors

- Fix-and-Flip Strategies: Aim for a minimum spread of 20% between acquisition and resale prices to accommodate holding costs and unexpected expenses.

- Exit Timing: Plan for a maximum project duration of six months to minimize holding costs and market exposure.

- Buy-and-Hold Tactics: Target properties with a cap rate of at least 6% to ensure adequate returns under current market conditions.

- DSCR Cushion: Maintain a DSCR of 1.25 or higher to withstand potential rent declines or interest rate hikes.

- Bridge Financing: Structure draw schedules to align with project milestones, ensuring access to funds while minimizing interest accumulation.

- Contingency Reserves: Allocate at least 10% of project costs as a contingency to cover unforeseen expenses.

- Geographic Focus: Prioritize investments in regions such as the Sun Belt where job growth and migration trends support strong rental demand.

- Conservative Underwriting: Implement a 5% stress test on rental income projections to account for economic fluctuations.

- Portfolio Diversification: Balance investments across three asset classes and multiple geographic areas to reduce risk exposure.

- Risk Mitigation: Enhance property insurance and conduct thorough tenant screenings to protect against potential losses.

By integrating these strategies and considerations, investors can navigate the complexities of the current market with confidence, ensuring both profitability and resilience in their real estate ventures.

Resources

External References

Disclaimer: This market analysis is for informational purposes only and should not be considered financial or investment advice. Market conditions can change rapidly. Consult with a qualified financial or lending professional before making any decisions.