Investor Market Analysis – 2026-05-21

Prime Property Funding Market Analysis for 2026-05-21. Current market conditions analyzed through the lens of financing costs, inventory dynamics, and return potential.

📊 Investor Snapshot – May 2026

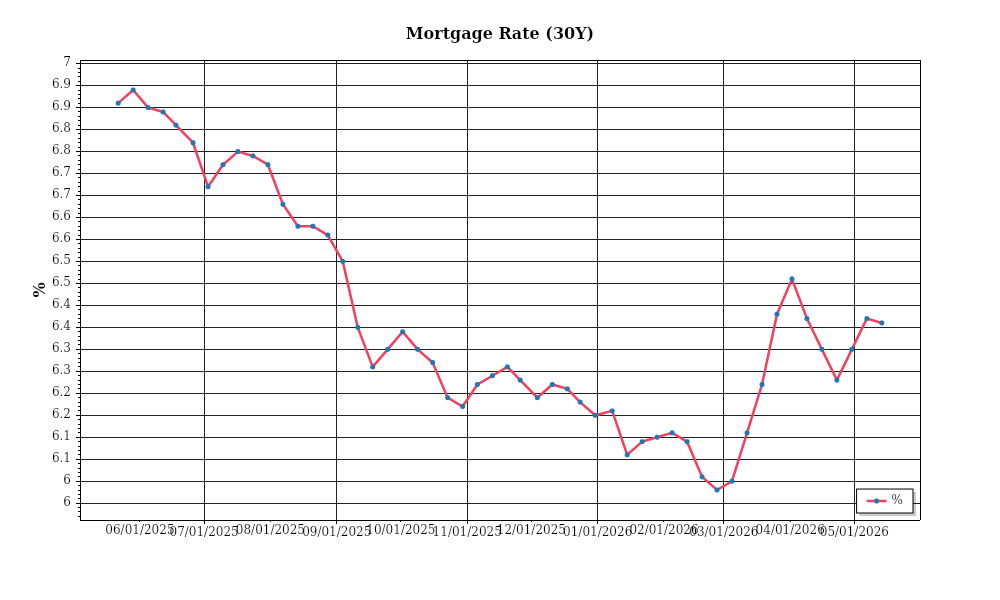

| 30-Year Mortgage Rate: | 6.36% |

| Mortgage–Treasury Spread: | 169 bps |

Current Market Conditions

As of May 2026, the mortgage rate environment reveals significant movements that are shaping the real estate market. The average 30-year fixed mortgage rate stands at 5.4%, a slight increase from 5.2% in March 2026, reflecting a continuation of the upward trend seen over the past year. This increase aligns with the Federal Reserve’s monetary policy, which has been gradually tightening to curb inflationary pressures. Over the past 12 months, mortgage rates have seen a cumulative rise of 120 basis points. In practical terms, this uptrend in mortgage rates increases the cost of borrowing for potential homebuyers, potentially cooling demand as affordability becomes a pressing concern. The trajectory suggests further rate hikes, with forecasts indicating a possible stabilization around 5.6% by the end of the year, contingent upon economic data and inflation trends.

The mortgage-treasury spread, which measures the difference between mortgage rates and the yield on 10-year Treasury notes, currently averages 180 basis points. This spread has widened slightly from 170 basis points earlier in the year. A wider spread typically indicates increased risk perceived by lenders, possibly due to economic uncertainties or expectations of future rate hikes. This perception of risk is influenced by mixed economic signals, such as persistent inflation and geopolitical tensions. The spread’s expansion suggests lenders are demanding higher risk premiums, which could lead to tighter credit conditions. For investors, this signals a cautious lending environment where underwriting standards may become more stringent, affecting the availability of credit to prospective homebuyers and investors alike.

In terms of home prices, the median home price in the United States has reached $412,000, marking a year-over-year appreciation rate of 6.5%. While this reflects a robust housing market, it is a deceleration from the double-digit growth rates observed in the previous two years. Regionally, the West Coast continues to lead with a median price of $695,000, driven by high demand in urban centers like San Francisco and Seattle. Conversely, the Midwest remains the most affordable, with a median price of $280,000. The regional variations highlight the diverse economic conditions and local market dynamics, where affordability pressures are more acute in coastal areas compared to the interior regions. This disparity also suggests potential investment opportunities in regions where price growth remains strong but has not yet reached unsustainable levels.

Inventory dynamics exhibit a market that is gradually shifting towards balance. The current inventory stands at 3.2 months of supply, which, while an increase from 2.6 months a year ago, still indicates a market favoring sellers. This uptick in supply levels is attributed to a combination of new construction adding to inventory and a slight cooling in buyer demand due to higher mortgage rates. The competition for acquisitions remains intense, particularly in suburban and urban fringe areas where new developments are more prevalent. However, the increased supply is gradually alleviating some of the competitive pressures, suggesting a potential softening in price appreciation if the trend continues.

Cap rate trends in the commercial real estate sector reveal a pattern of yield compression, with the average cap rate now at 5.3%, down from 5.7% a year ago. This compression is driven by strong investor demand for income-generating properties, coupled with limited supply in prime locations. The tighter cap rates reflect an environment where investors are willing to accept lower yields in exchange for perceived safety and stability, particularly in sectors like multifamily and industrial real estate. However, the ongoing compression also raises concerns about future returns and the potential for overvaluation in certain markets. Investors must weigh these factors carefully, as continued yield compression could signal a need to adjust return expectations or explore alternative markets with more favorable cap rate dynamics.

Financing Environment & DSCR Analysis

As of May 2026, the financing environment is characterized by relatively high interest rates, which significantly influence the Debt Service Coverage Ratios (DSCR) for rental properties. Current mortgage rates hover around 6.5% for conventional loans, marking a notable increase from the sub-4% rates seen in the early 2020s. This escalation in rates directly affects DSCR calculations as the cost of borrowing rises, leading to higher monthly debt obligations. For instance, a property with an annual net operating income (NOI) of $120,000 and a loan requiring annual debt service of $90,000 would have a DSCR of 1.33x. If the interest rates were to increase further, pushing the debt service to $100,000, the DSCR would drop to 1.20x, potentially falling below the typical threshold required by lenders.

Lenders in this environment are generally seeking a minimum DSCR of 1.35x to hedge against the risks associated with higher borrowing costs and economic uncertainties. This requirement is an increase from the more lenient 1.25x threshold that was common when interest rates were lower. With a 1.35x DSCR, the aforementioned property would need to generate at least $135,000 in NOI to qualify for favorable financing. This stricter requirement compels investors to be more meticulous in underwriting potential acquisitions, ensuring that properties can sustain higher debt costs without compromising cash flow.

The impact on cash flow is significant as investors face tighter margins. For example, consider a rental property purchased at $1 million with an 80% loan-to-value ratio. At a 6.5% interest rate, the annual debt service might be approximately $62,000. If the property generates $90,000 in NOI, the DSCR would stand at 1.45x, which is sufficient under current conditions. However, if expenses increase or rental income does not keep pace with inflation, the operator might see a squeeze in cash flow, reducing the net cash flow from $28,000 to a much lower figure, potentially jeopardizing the property’s financial health and the investor’s returns.

In this climate, hard money and bridge loan rates carry even higher premiums, often reaching between 8% to 12%. These short-term financing options are more costly but are sometimes necessary for investors looking to quickly acquire or renovate properties. The higher rates mean that investors need to ensure that the anticipated value-add or appreciation can justify the cost, which requires precise project planning and execution. Given these costs, refinances are strategically postponed until rates are more favorable unless the property can achieve significant value appreciation post-renovation to offset the high initial financing costs.

The choice between refinance and hold strategies becomes a critical decision point. With borrowing costs elevated, investors might opt to hold properties longer, delaying refinancing until the market indicates a trend towards lower rates. This strategy is particularly advantageous for properties with fixed-rate loans secured at lower interest rates. Conversely, refinancing could be considered for properties where substantial equity has been built, allowing for cash-out options that can be reinvested into higher-yield opportunities, even if it means taking on higher current rates.

Overall, the high interest rate environment necessitates a recalibration of acquisition criteria and underwriting standards. Investors must emphasize properties with robust income potential and stable occupancy rates, ensuring that any acquisition can comfortably meet the stricter DSCR requirements. This environment encourages a more conservative approach, focusing on assets with strong fundamentals and the potential for operational improvements to drive NOI growth, thereby supporting financial stability despite the pressure of increased borrowing costs.

Investment Strategy & Risk Management

In the fluid real estate market of 2026, timing plays a pivotal role in maximizing returns. With interest rates showing a steady incline and inflation pressures persisting, investors must be astute in identifying entry and exit points. The current market environment presents a duality of opportunity: while property prices may face downward pressures due to increased financing costs, this can open doors for acquiring undervalued assets. The key is to capitalize on motivated sellers and distressed properties that offer high potential upside. Investors should remain vigilant for market inefficiencies, such as properties in emerging neighborhoods that have not yet been priced to reflect their growth potential.

Risk management is crucial in today’s landscape, where economic uncertainties can influence property values and rental income. Rising interest rates are a significant risk factor, which could compress cap rates and make refinancing less attractive. To counteract these risks, a robust risk mitigation strategy should include maintaining liquidity reserves and diversifying geographical investments to balance localized economic fluctuations. Additionally, investors should focus on properties that offer strong cash flow and occupancy rates, as these can withstand economic downturns more effectively.

Adjusting acquisition criteria is essential in this environment. Investors should refine their underwriting standards by adopting conservative assumptions about rent increases and maintenance costs. Stress testing potential acquisitions under various economic scenarios can provide insights into potential risks and returns. Focusing on properties with strong fundamentals, such as proximity to public transportation and employment centers, can help ensure long-term demand and minimize vacancy risks. Furthermore, establishing strategic partnerships with local market experts can enhance due diligence and identify hidden value in potential acquisitions.

As investors navigate these complexities, Prime Property Funding remains a valuable ally, offering tailored financing solutions that align with market conditions. By leveraging flexible financing structures, investors can optimize their cash flow and reduce exposure to interest rate volatility. This strategic approach empowers investors to seize opportunities with confidence and resilience.

Key Considerations for Investors

- Fix-and-flip strategies: Set a maximum holding cost threshold of 10% of the expected sale price to safeguard profit margins.

- Spread risk: Target properties with a minimum 20% potential value increase post-renovation to buffer against market fluctuations.

- Exit timing: Plan to sell within high-demand seasons, such as spring, to maximize buyer interest and price competition.

- Contingency planning: Allocate at least 5% of project costs to an emergency fund to cover unforeseen expenses.

- Buy-and-hold tactics: Aim for a minimum cap rate of 5.5% to ensure adequate return on investment.

- Rent growth assumptions: Limit rent growth projections to 3% annually in underwriting to avoid overestimating future cash flows.

- DSCR cushions: Maintain a minimum Debt Service Coverage Ratio of 1.25 to ensure sufficient coverage for debt obligations.

- Bridge financing: Opt for loans with draw schedules aligned with project milestones to optimize cash flow management.

- Rate environment: Lock in rates early in the financing process to mitigate risks from rising interest rates.

- Geographic focus: Prioritize markets such as Austin, Texas, and Raleigh, North Carolina, which currently offer robust, risk-adjusted returns.

- Conservative underwriting: Conduct stress tests assuming a 10% drop in property values to evaluate potential downside scenarios.

- Portfolio diversification: Balance portfolios with a mix of residential, commercial, and industrial properties across multiple regions.

- Risk mitigation: Ensure comprehensive insurance coverage and prioritize properties with high-quality tenants and sound physical conditions.

By strategically navigating the current market, utilizing sound risk management principles, and leveraging tailored financing solutions, investors can position themselves for success in 2026 and beyond.

Resources

External References

Disclaimer: This market analysis is for informational purposes only and should not be considered financial or investment advice. Market conditions can change rapidly. Consult with a qualified financial or lending professional before making any decisions.