Investor Market Analysis – 2026-05-18

Prime Property Funding Market Analysis for 2026-05-18. Current market conditions analyzed through the lens of financing costs, inventory dynamics, and return potential.

📊 Investor Snapshot – May 2026

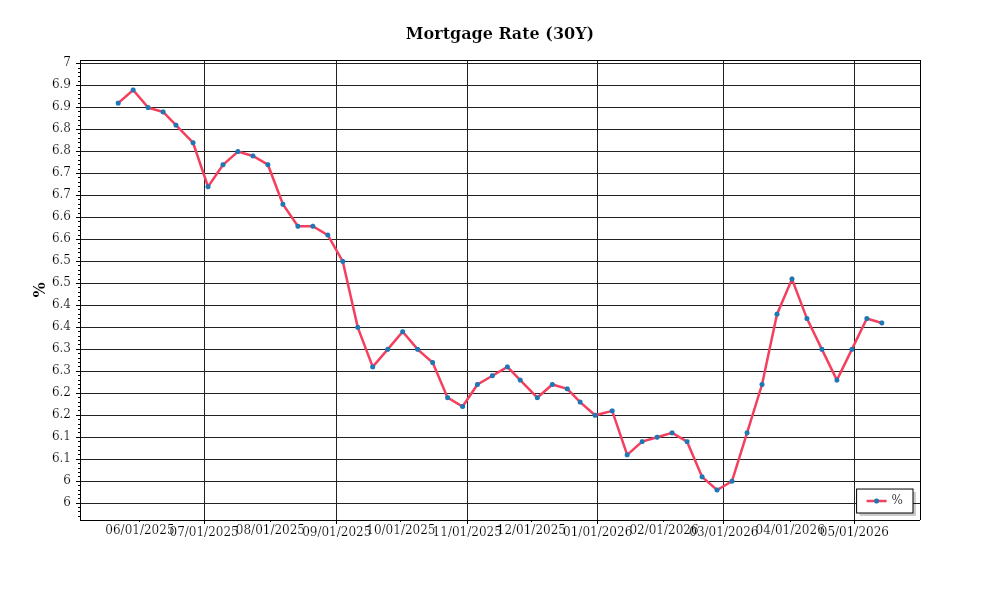

| 30-Year Mortgage Rate: | 6.36% |

| Mortgage–Treasury Spread: | 189 bps |

Current Market Conditions

The mortgage rate environment in May 2026 is characterized by significant fluctuations. As of the latest data, the average 30-year fixed-rate mortgage stands at 5.2%, a decrease from the 5.8% recorded six months prior. This decline follows a period of aggressive tightening by the Federal Reserve, which has now shifted to a more neutral stance as inflation pressures moderate. The reduction in rates has been driven partly by a cooling inflation rate, now at 3.1%, and partly by stabilizing economic growth projections. Recent trends indicate that mortgage rates have been on a downward trajectory, with expectations of stabilization around current levels for the remainder of the year. For investors, this environment suggests more favorable financing conditions, potentially increasing the attractiveness of real estate acquisitions.

The mortgage-treasury spread, a critical indicator of lender risk perception, is currently at 1.4%, down from 1.8% just three months ago. This narrowing spread suggests that lenders perceive reduced risk in the mortgage market, possibly due to improved economic conditions and robust housing demand. Historically, a spread below 1.5% indicates a healthy lending environment where lenders are more confident about borrower creditworthiness and the stability of real estate values. This confidence can lead to more competitive mortgage products and, consequently, increased buyer activity. However, it is essential for investors to monitor this metric closely, as any abrupt widening could signal emerging risks or economic instability.

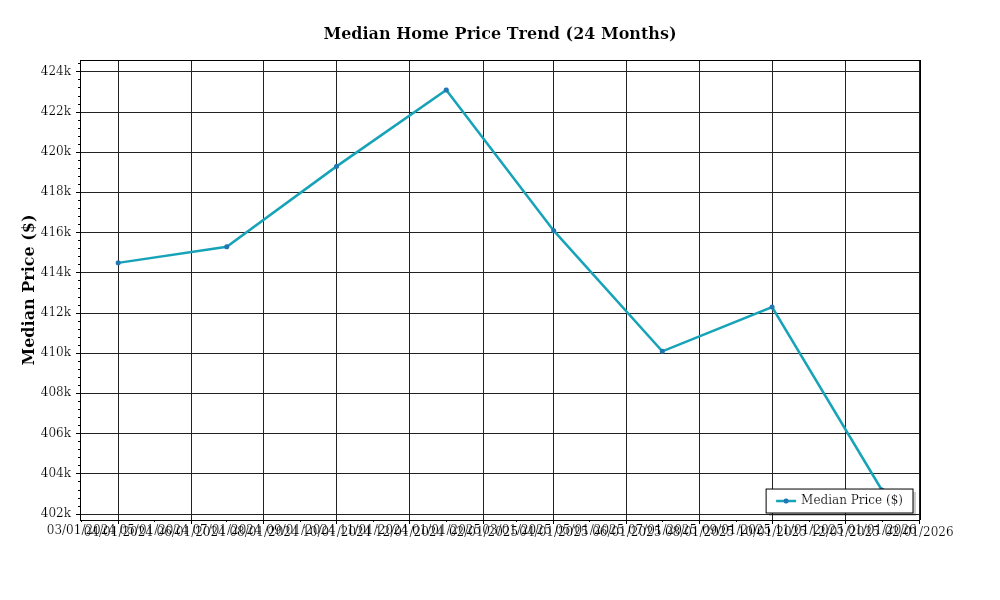

Median home prices continue their upward trajectory, although at a moderated pace compared to the frenetic growth witnessed in recent years. The national median home price is currently at $436,000, reflecting an annual appreciation rate of 6%. This is a deceleration from the 10% growth rate observed in 2024, indicating a market transitioning towards equilibrium. Regional variations remain pronounced; for instance, the Sun Belt states continue to experience robust growth, with median prices in cities like Phoenix and Austin increasing by 8% and 7.5%, respectively. Meanwhile, some coastal markets, such as San Francisco, show signs of stabilization with prices increasing by a modest 3%, suggesting a saturation point may be near in these traditionally high-demand areas.

Inventory dynamics reveal a market still grappling with supply constraints, though conditions are gradually improving. The current months’ supply of homes is at 3.2 months, up from 2.8 months a year ago. While this indicates a slight easing in the competition for acquisitions, the market remains skewed towards sellers, with a balanced market typically requiring a 6-month supply. New construction is ramping up, albeit slowly, as builders face challenges related to labor shortages and material costs. For investors, this persistent low inventory means that acquiring properties remains competitive, necessitating strategic planning and potentially higher offers to secure desirable assets.

Cap rate trends provide insight into the real estate investment climate, with the average cap rate for multifamily properties currently at 5.1%. This marks a slight expansion from the 4.8% recorded last year, indicating a potential shift in investor expectations and a slight easing of yield compression. The increase in cap rates can be attributed to the stabilization of property values and the aforementioned easing of mortgage rates, which together influence the return on investment calculations. For investors, this trend suggests a more favorable environment for acquiring properties with higher initial yields, though careful analysis is required to ensure these investments align with long-term financial objectives.

Financing Environment & DSCR Analysis

As of May 2026, the financing environment is characterized by a gradual increase in interest rates, which significantly affects the Debt Service Coverage Ratios (DSCR). With the current average interest rate for commercial real estate loans hovering around 6.5%, the cost of borrowing has risen considerably from the historically low rates of the past decade. This increase in borrowing costs directly impacts the DSCR, a critical metric used by lenders to assess a borrower’s ability to cover debt obligations with their net operating income (NOI). Higher interest rates result in higher debt service payments, reducing the DSCR unless the property’s NOI increases proportionally. For example, if a property generates a monthly NOI of $10,000 and the debt service increases to $8,500 due to rising interest rates, the DSCR would drop to 1.18x, below the typical lender requirements.

In the current environment, lenders are generally requiring higher DSCR thresholds to mitigate risk. Traditionally, a minimum DSCR of 1.25x is considered acceptable, meaning the property’s NOI should be 1.25 times the debt service. However, with the heightened risk associated with increasing interest rates, many lenders have adjusted their minimum DSCR requirements to around 1.35x. This adjustment ensures that borrowers have a more substantial buffer against potential income fluctuations or further rate increases. For instance, under the 1.35x requirement, the same property with a monthly NOI of $10,000 would need to ensure its debt service does not exceed approximately $7,407, necessitating either increased rental income or reduced loan amounts to meet these criteria.

The impact of these requirements on cash flow for rental properties is substantial. Investors must focus on increasing NOI through strategies such as raising rents, reducing vacancies, or cutting operational costs to maintain or achieve the necessary DSCR. Consider a rental property with an annual NOI of $120,000. If the interest rate on its loan increases from 4% to 6.5%, the annual debt service might rise from $96,000 to $104,000, reducing the DSCR from 1.25x to 1.15x, which falls short of even the traditional threshold. To restore a DSCR of 1.35x, the investor would need to increase the NOI to approximately $140,400, either by optimizing operations or enhancing property value.

Hard money and bridge loans, often utilized for short-term financing, carry even higher rate premiums in the current market, with rates typically ranging from 9% to 12%. These loans, while offering rapid access to capital, impose significant pressure on DSCR calculations. For a bridge loan at a 10% interest rate on a loan of $1 million, the annual debt service would be around $100,000, necessitating an NOI of at least $135,000 to meet a 1.35x DSCR. Consequently, these financing options are more suited to projects with robust cash flow or those expected to rapidly increase in value.

Given the current rate environment, investors face critical decisions regarding refinance timing versus holding strategies. While refinancing at higher rates may be less appealing, it could be necessary if existing loans have unfavorable terms or if capital is needed for other investments. Conversely, holding onto properties with existing favorable financing terms could prove beneficial, especially if future rate hikes are anticipated. Investors must carefully evaluate the trade-offs between locking in current rates versus potential future decreases that might offer more favorable refinancing opportunities.

The current financing landscape also influences acquisition criteria and underwriting standards. Investors are increasingly conservative, emphasizing properties with strong cash flow, stable tenant bases, and minimal exposure to volatile markets. Underwriting standards are more stringent, with increased scrutiny on tenant creditworthiness and lease terms to ensure properties can sustain higher DSCRs. This cautious approach necessitates thorough due diligence and strategic decision-making to align property acquisition with broader financial objectives in this evolving market.

Investment Strategy & Risk Management

In the current real estate market, careful timing and strategic identification of opportunities are paramount for achieving optimal returns. As we stand in May 2026, the real estate landscape is characterized by fluctuating interest rates and evolving consumer preferences, making precise market timing critical. Investors should focus on regions with strong economic fundamentals, such as robust job growth and population influx, to capitalize on upward trends. Identifying properties with value-add potential or those located in emerging neighborhoods can provide significant upside. Moreover, keeping an eye on seasonal patterns can inform acquisition strategies, as certain times of the year may offer more favorable conditions for purchasing or selling properties.

Risk factors in the present environment include potential interest rate hikes, inflationary pressures, and supply chain disruptions affecting renovation costs and timelines. To mitigate these risks, investors should adopt a multi-pronged approach. Implementing conservative underwriting standards is essential, with stress testing for worst-case scenarios to ensure financial resilience. Maintaining liquidity reserves can help navigate unexpected market shifts or cost overruns in renovation projects. Additionally, enhancing due diligence processes to include thorough inspections and assessments of tenant quality and lease terms will further insulate against unforeseen vacancies and income variability.

Adjusting acquisition criteria to reflect current market dynamics is crucial for maintaining competitive advantage. Investors should refine their underwriting standards to account for increased construction costs and potential delays, ensuring a buffer in projected timelines and budgets. Building flexibility into financing structures, such as opting for fixed-rate products where feasible, can guard against future interest rate increases. Furthermore, focusing on properties with strong fundamentals—such as high demand areas with limited supply—can enhance long-term value retention and appreciation potential.

In summary, the current real estate landscape requires a strategic, well-rounded approach to investment. By staying attuned to market trends and aligning acquisition strategies with sound risk management practices, investors can position themselves to navigate the complexities of today’s market. Embracing a proactive stance, with a willingness to adapt to changing conditions, will empower investors to achieve robust returns while safeguarding their portfolios against potential downturns.

Key Considerations for Investors

- For fix-and-flip strategies, ensure that holding costs do not exceed 10% of the projected sale price to maintain profitability, and establish a contingency fund of at least 5% of the total project cost.

- Set cap rate targets for buy-and-hold properties at a minimum of 7% to ensure competitive returns, factoring in conservative rent growth assumptions of 3% annually.

- Maintain a DSCR cushion of 1.25 or greater for buy-and-hold investments to accommodate potential fluctuations in rental income and operating expenses.

- In bridge financing, negotiate flexible draw schedules that align with project milestones, and allocate at least 10% of the loan amount as a contingency reserve to address unforeseen costs.

- Leverage seasonal patterns by targeting acquisitions in Q4, when market activity typically slows, potentially leading to more favorable purchase terms.

- Focus geographic investment in markets like Austin, TX, and Raleigh, NC, where risk-adjusted returns remain robust due to strong economic growth and increasing demand.

- Employ conservative underwriting by stress testing assumptions, such as vacancy rates and renovation timelines, to withstand market volatility and economic uncertainties.

- Diversify your portfolio by balancing asset classes, such as residential and commercial properties, and spreading investments across at least three different geographic markets.

- Enhance risk mitigation by maintaining reserves equivalent to six months of operating expenses, securing comprehensive insurance, and ensuring properties are in good condition with quality tenants.

- Approach new acquisitions with confidence, leveraging robust market data and strategic foresight to capitalize on emerging opportunities and secure sustainable growth.

Resources

External References

Disclaimer: This market analysis is for informational purposes only and should not be considered financial or investment advice. Market conditions can change rapidly. Consult with a qualified financial or lending professional before making any decisions.