Investor Market Analysis – 2026-05-16

Prime Property Funding Market Analysis for 2026-05-16. Current market conditions analyzed through the lens of financing costs, inventory dynamics, and return potential.

📊 Investor Snapshot – May 2026

| 30-Year Mortgage Rate: | 6.36% |

| Mortgage–Treasury Spread: | 189 bps |

Current Market Conditions

In May 2026, the mortgage rate environment continues to reflect the broader economic landscape, characterized by volatility and gradual shifts. As of this month, the average 30-year fixed mortgage rate stands at 5.6%, a slight decrease from 5.8% observed in April 2026. This decline follows an upward trajectory witnessed throughout 2025, where rates peaked at 6.2% in November. This recent dip can be attributed to the Federal Reserve’s decision to halt rate hikes in early 2026, aiming to stabilize economic growth amid concerns of slowing inflation. The 15-year fixed mortgage rate mirrors this trend, currently at 5.1%, down from 5.3% the previous month. These figures indicate a modest easing of borrowing costs, which could potentially stimulate housing demand if sustained.

Examining the mortgage-treasury spread offers insights into lender risk perceptions and the broader economic sentiment. As of May 2026, the spread between the 30-year fixed mortgage rate and the 10-year treasury yield is approximately 2.0%. This spread has narrowed slightly from 2.2% in March 2026, suggesting a reduced risk premium demanded by lenders. Historically, a spread above 1.75% indicates heightened risk concerns, often triggered by economic uncertainty or potential market corrections. The current 2.0% spread implies that while lenders remain cautious, they are increasingly confident about economic stability, possibly influenced by positive employment figures and controlled inflation rates. This narrowing spread could enhance borrower accessibility, promoting more robust housing market activity.

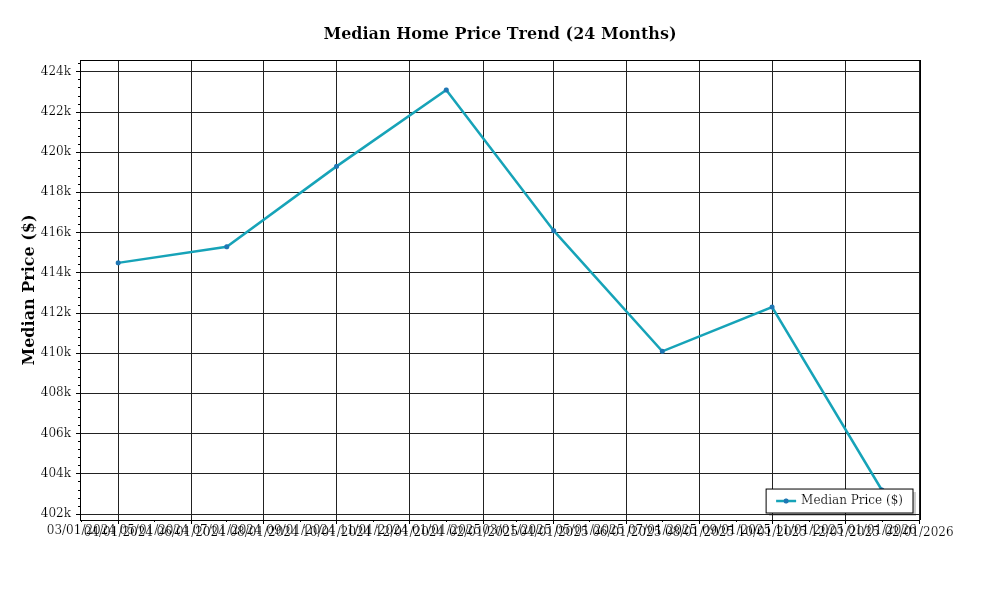

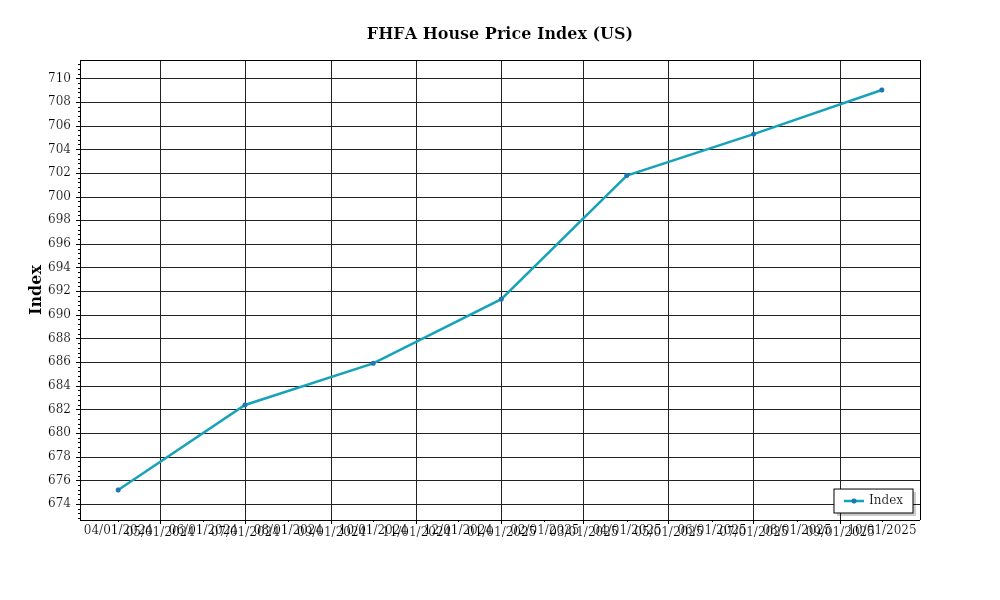

Median home price trends across the United States continue to diversify, with regional variations becoming increasingly pronounced. The national median home price in May 2026 is $420,000, marking a 4.7% year-over-year increase from $401,000 in May 2025. However, this growth rate represents a slowdown from the double-digit appreciation observed during the pandemic era. In the Western United States, particularly in cities like San Francisco and Seattle, median prices have plateaued, with increases of just 2.3% and 1.9% respectively, due to high inventory levels and affordability challenges. Conversely, regions in the Southeast, such as Atlanta and Charlotte, continue to experience robust growth, with median prices rising by 6.5% and 7.1%, driven by strong migration trends and economic expansions. These regional disparities highlight the importance of localized market assessments for informed investment decisions.

Inventory dynamics reveal a complex interplay of supply and demand forces, shaping the competitive landscape for home acquisitions. As of May 2026, national housing inventory stands at approximately 1.25 million units, reflecting a 5% increase from the previous year. This rise in inventory is attributed to a combination of new construction projects coming to fruition and a slight uptick in existing homeowners listing properties, motivated by favorable selling conditions. Despite this increase, the market remains relatively tight, with a current supply of 3.2 months, below the balanced market threshold of 6 months. This imbalance perpetuates competition among buyers, particularly in high-demand areas, sustaining upward pressure on prices and reducing negotiation leverage for purchasers.

Finally, cap rate trends offer insights into the commercial real estate sector’s health and investor yield expectations. As of May 2026, average cap rates for multifamily properties are at 5.4%, reflecting a compression from 5.7% in May 2025. This trend of yield compression indicates strong investment demand, driven by perceived stability and attractive returns compared to other asset classes. In contrast, retail and office sectors exhibit a slight cap rate expansion, currently at 6.8% and 7.1% respectively, up from 6.6% and 6.9% a year ago. These figures suggest a cautious approach to sectors still recovering from pandemic disruptions, with investors demanding higher yields to compensate for perceived risks. Understanding these cap rate dynamics is crucial for investors seeking to optimize portfolio performance in a shifting market environment.

Financing Environment & DSCR Analysis

In May 2026, the financing environment is markedly influenced by the prevailing interest rates, which have seen a slight increase over the past year. These rates significantly impact the Debt Service Coverage Ratios (DSCR), a crucial metric for real estate investors seeking to evaluate the financial health and risk of their investments. As current interest rates hover around 5.5%, they directly affect borrowing costs, subsequently influencing the DSCR by increasing the debt service obligations for property owners. A higher interest rate generally leads to a lower DSCR because a larger portion of rental income is allocated towards servicing debt, thereby reducing the buffer for covering other expenses. For instance, assuming a property generates a net operating income (NOI) of $120,000 annually, with a debt service requirement of $100,000 at a 4% interest rate, the DSCR is 1.20x. However, with the rate adjustment to 5.5%, if the debt service rises to $110,000, the DSCR effectively drops to 1.09x, which fails to meet typical lending standards.

The prevailing DSCR requirements in today’s market remain stringent, typically ranging between 1.25x and 1.35x. Lenders are increasingly cautious, often demanding a minimum threshold of 1.35x to mitigate their risk exposure. This conservative approach is a response to the uncertain economic landscape and potential fluctuations in property values. For investors, achieving a DSCR of 1.35x means ensuring that their properties generate sufficient cash flow to cover at least 135% of the debt obligations. For example, to meet a 1.35x DSCR with a debt service of $110,000, the property must produce an NOI of $148,500. This requirement necessitates strategic financial planning and efficient property management to optimize rental income and control operating expenses.

The cash flow implications for rental properties are significant under these conditions. With higher debt obligations, property owners must maximize rental income to preserve their cash flow margins. Consider a multi-family property with annual rental income of $180,000 and operating expenses totaling $60,000. The NOI of $120,000 initially appears adequate. However, with increased debt service of $110,000 due to higher interest rates, the cash flow is squeezed to just $10,000 annually, limiting the owner’s ability to reinvest in property improvements or expand their portfolio. This scenario underscores the importance of rigorous financial analysis and stress testing to ensure investments remain viable under varying economic conditions.

In the current market, hard money and bridge loan rate premiums are notably higher, reflecting lenders’ risk aversion. Rates for these short-term financing solutions typically range between 8% to 12%, significantly above traditional mortgage rates. These premium rates are designed to compensate for the increased risk and shorter loan durations associated with such financing options. Investors relying on hard money or bridge loans must weigh the higher cost against the benefits of rapid capital access, often reserved for opportunistic acquisitions or urgent property renovations.

Given the current rate environment, investors face critical decisions regarding refinance timing versus hold strategies. If interest rates stabilize or potentially decrease, refinancing could offer substantial savings on debt service costs, enhancing cash flow and DSCR. Conversely, holding properties without refinancing may be prudent if rates continue to climb, avoiding the locking in of unfavorable terms. Therefore, maintaining flexibility in financing agreements and closely monitoring market trends is essential for optimizing investment returns.

The impact on acquisition criteria and underwriting standards is profound. Investors and lenders alike are recalibrating their approaches, emphasizing properties with robust cash flow potential and resilience to economic fluctuations. Underwriting standards now prioritize properties with stable tenant profiles, diversified income streams, and strong location fundamentals. This shift underscores the importance of rigorous due diligence and a comprehensive understanding of market dynamics to align acquisition strategies with financial objectives amidst a challenging financing landscape in May 2026.

Investment Strategy & Risk Management

In the current real estate market, investors face a nuanced landscape marked by shifting economic indicators and competitive pressures. Effective **market timing** and the ability to identify viable opportunities are crucial. Investors should closely monitor interest rate fluctuations, as they have a direct impact on financing costs and property values. While the Federal Reserve’s policy hints at potential stabilization, vigilance is necessary to capitalize on opportune moments when interest rates dip, thereby reducing the cost of borrowing. Identifying markets with robust job growth and population influx, such as cities in the Sun Belt, can provide strategic entry points for both short-term and long-term investments.

The current environment presents several **risk factors**, including economic uncertainty and potential geopolitical tensions that can influence market dynamics. Investors should adopt a multi-layered approach to risk management. This includes diversifying across asset classes and geographies, maintaining adequate liquidity reserves, and applying conservative underwriting standards. Additionally, implementing stress testing on cash flow projections can help gauge the resilience of investments under adverse conditions. Such strategies not only mitigate risks but also enhance the ability to seize unexpected opportunities.

Adjusting **acquisition criteria and underwriting standards** is essential to navigate the current market. A focus on properties with value-add potential can increase profit margins, especially in the fix-and-flip sector. Investors should tighten their criteria by emphasizing properties with strong underlying fundamentals, such as location desirability and structural integrity. Underwriting standards should incorporate conservative assumptions about rent growth and exit cap rates, given potential economic headwinds. Moreover, ensuring a healthy Debt Service Coverage Ratio (DSCR) cushion is vital for sustaining through potential revenue fluctuations.

Overall, strategic flexibility and rigorous risk assessment are paramount. Prime Property Funding is well-positioned to support investors with tailored financing solutions that align with market conditions. By leveraging these insights, investors can optimize their portfolios for both resilience and growth.

Key Considerations for Investors

- **Fix-and-flip strategies**: Target properties with potential for at least a 20% profit margin after accounting for holding costs and renovation expenses to buffer against market fluctuations.

- **Holding costs**: Establish a contingency fund covering at least six months of projected holding costs, including financing charges and property taxes, to mitigate delays in sales.

- **Buy-and-hold tactics**: Aim for a minimum **cap rate** of 5% in urban centers and 6% in suburban areas to ensure competitive returns.

- **Rent growth assumptions**: Use a conservative annual rent growth estimate of 2-3% in underwriting to account for economic variability.

- **DSCR cushions**: Maintain a DSCR of at least 1.3x to ensure sufficient cash flow coverage for debt obligations.

- **Bridge financing**: Structure draw schedules to align with project milestones, minimizing interest costs and optimizing cash flow.

- **Market timing**: Prioritize acquisitions during off-peak seasons when competition is lower, potentially securing better pricing.

- **Geographic focus**: Concentrate investments in markets like Austin, TX, and Raleigh, NC, where projected job growth and demographic trends offer favorable risk-adjusted returns.

- **Conservative underwriting**: Perform stress tests assuming a 10% decline in property values to prepare for potential market downturns.

- **Portfolio diversification**: Balance portfolios with a mix of residential and commercial assets across at least three distinct geographic regions to spread risk effectively.

With a strategic approach and robust risk management practices, investors can confidently navigate the complexities of today’s real estate market, ensuring both protection and potential for significant returns.

Resources

External References

Disclaimer: This market analysis is for informational purposes only and should not be considered financial or investment advice. Market conditions can change rapidly. Consult with a qualified financial or lending professional before making any decisions.