Investor Market Analysis – 2026-05-13

Prime Property Funding Market Analysis for 2026-05-13. Current market conditions analyzed through the lens of financing costs, inventory dynamics, and return potential.

📊 Investor Snapshot – May 2026

| 30-Year Mortgage Rate: | 6.37% |

| Mortgage–Treasury Spread: | 195 bps |

Current Market Conditions

The current landscape of the real estate market in May 2026 is shaped significantly by the mortgage rate environment. As of now, the average 30-year fixed mortgage rate stands at 6.75%, reflecting a modest increase from 6.50% in April 2026. This uptick aligns with a broader upward trend observed over the past year, where rates have risen from 5.25% in May 2025. This trajectory is primarily influenced by the Federal Reserve’s monetary policy stance, which has focused on combating persistent inflation through incremental rate hikes. As a result, the cost of borrowing has increased, impacting affordability and potentially cooling buyer enthusiasm in the housing market. The current trajectory suggests that rates may stabilize if inflationary pressures ease, but any unexpected economic shocks could further elevate these rates.

In addition to the mortgage rate environment, the mortgage-treasury spread offers insights into lender risk perceptions. Currently, the spread between the 30-year fixed mortgage rate and the 10-year Treasury yield is at 2.25%. This spread has widened from 1.90% a year ago, indicating heightened risk aversion among lenders. Historically, a widening spread suggests that lenders are demanding higher compensation for perceived risks, possibly due to economic uncertainties or volatility in the housing market. This situation signals a cautious approach from financial institutions, potentially leading to tighter lending standards and impacting the overall accessibility of mortgage loans for prospective buyers.

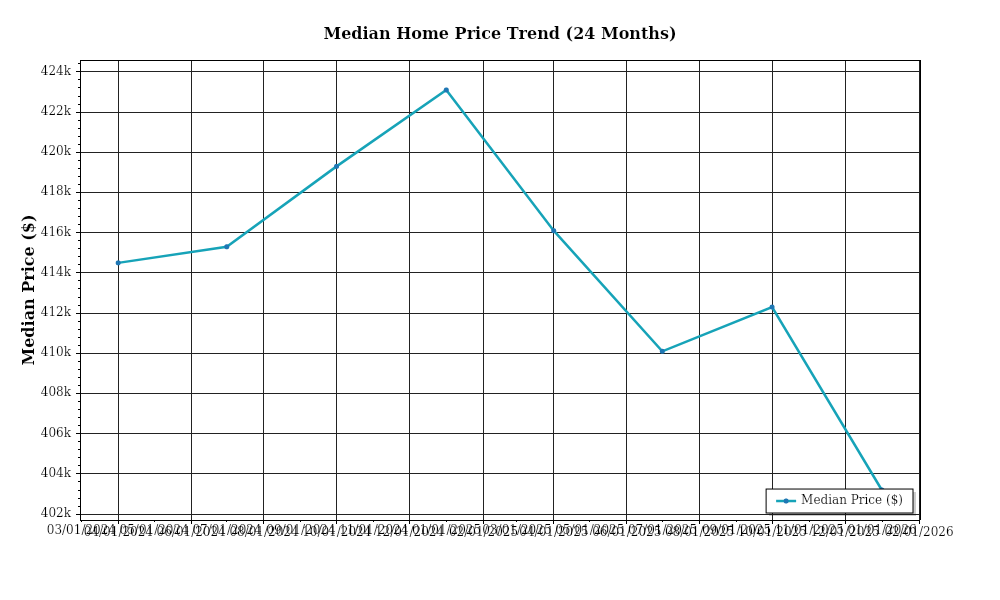

Turning to median home price trends, the national median home price is currently pegged at $420,000, marking an annual appreciation rate of 3.5%. This rate represents a deceleration from the robust 6.2% growth recorded in the previous year. Regional variations are notable, with the Western U.S. experiencing the highest appreciation at 4.8%, driven by strong demand in metropolitan areas like Seattle and Denver. Conversely, the Midwest sees a more modest increase of 2.1%, reflecting more stable demand and supply dynamics. This variation underscores the importance of regional economic factors and demographic trends in influencing home price movements.

Inventory dynamics continue to play a critical role in shaping the real estate market. As of May 2026, the national housing inventory stands at 2.5 months of supply, which is below the balanced market threshold of 6 months. This low level of supply indicates a seller’s market, characterized by limited options for buyers and heightened competition for available properties. The competitive landscape is particularly intense in urban centers where demand significantly outpaces supply, leading to bidding wars and rapid sales. However, there are signs of inventory levels inching higher as more homeowners look to capitalize on elevated home prices, which could gradually ease the current imbalance and stabilize the market.

Cap rate trends provide further insights into the real estate investment climate. The average cap rate for multifamily properties has recently compressed to 5.3%, down from 5.7% a year ago. This compression is indicative of strong investor interest and confidence in the long-term potential of rental income despite rising financing costs. However, other sectors like retail and office spaces are witnessing a cap rate expansion to 6.1% and 7.0%, respectively, reflecting investor caution due to changing consumer behaviors and increasing remote work trends. Yield compression in multifamily properties suggests that investors are willing to accept lower returns due to perceived stability and demand resilience, while expansion in other sectors highlights the differentiated risk profiles and strategic adjustments investors must consider.

In sum, the current market conditions in May 2026 are marked by a complex interplay of rising mortgage rates, widened mortgage-treasury spreads, varied home price appreciation, constrained inventory, and divergent cap rate trends. These factors collectively shape the investment landscape and require careful analysis to navigate effectively.

Financing Environment & DSCR Analysis

As of May 2026, the financing environment has seen interest rates maintaining a moderately high level compared to the previous years, which directly impacts the Debt Service Coverage Ratio (DSCR). Currently, the average interest rate for 30-year fixed mortgages is around 6.5%, while commercial real estate loans hover slightly higher at approximately 7.0%. These elevated rates affect the DSCR by increasing the debt service obligations, thus requiring higher net operating income (NOI) to meet lender thresholds. In this environment, lenders typically enforce a DSCR minimum requirement ranging between 1.25x to 1.35x, with more conservative lenders leaning towards the latter. This means that for every dollar of debt service, the property must generate at least $1.25 to $1.35 in NOI, making it crucial for investors to optimize property performance or consider alternative financing structures.

The implications for cash flow in rental properties are significant. For example, consider a property generating an NOI of $100,000 annually. Under a 1.25x DSCR requirement, the maximum annual debt service permissible would be $80,000 ($100,000 / 1.25). However, with the DSCR threshold increasing to 1.35x, the maximum debt service drops to approximately $74,074 ($100,000 / 1.35). This directly affects the amount of leverage an investor can utilize, often necessitating a larger equity contribution or a reduction in purchase price to meet lender requirements. With elevated interest rates, the monthly mortgage payment for a $1 million loan at 7.0% interest would be approximately $6,653.02, translating to an annual debt service of $79,836.24. In this scenario, properties with lower NOI or those acquired at inflated prices may struggle to meet the DSCR requirements, prompting a need for strategic financial planning.

In the current market, hard money and bridge loans carry an even higher premium, with rates typically ranging from 10% to 12%. These loans, designed for short-term financing or transitional properties, now demand careful consideration of the holding period and exit strategy. While they offer the flexibility to quickly close deals or finance non-stabilized properties, the high cost of borrowing can erode profitability if the transition to long-term financing or property stabilization is delayed. As such, investors must meticulously plan the timeline for refinancing into more favorable terms, particularly as rate projections suggest eventual stabilization but not immediate declines.

The decision to refinance versus hold is complex in this rate environment. Refinancing to lock in current rates might seem prudent to avoid potential future hikes, but the associated costs and the likelihood of future rate stabilization should be weighed. Holding onto an existing mortgage with a lower rate could be advantageous if the difference in interest rates results in minimal cash flow improvement post-refinance. Nevertheless, properties with adjustable-rate debt or nearing loan maturity must evaluate refinancing options proactively to mitigate the risk of rate increases.

Lastly, these financial dynamics significantly influence acquisition criteria and underwriting standards. Lenders are increasingly emphasizing robust DSCR metrics, conservative value assessments, and strong borrower credentials. Underwriting now often includes stress testing at higher interest rates to ensure ongoing viability. As a result, investors must adjust acquisition strategies, focusing on properties with potential for NOI growth, or considering markets with historically stable or appreciating rental rates. Additionally, diversifying financing sources and engaging in strategic partnerships can enhance purchasing power and mitigate individual exposure to financial risks. Understanding these nuances allows investors to navigate the current environment effectively, ensuring decisions are both strategic and sustainable.

Investment Strategy & Risk Management

In the evolving real estate landscape of May 2026, astute market timing can be the cornerstone of a successful investment strategy. As market conditions shift, investors should capitalize on the cyclical nature of real estate by identifying opportunities for acquisition during low-demand periods and preparing for higher returns as demand rebounds. This entails close monitoring of market indicators such as interest rate movements, housing supply dynamics, and consumer confidence metrics, which collectively signal optimal entry and exit points. Prime Property Funding can leverage its expertise in hard money loans and DSCR loans to assist investors in rapidly capitalizing on these opportunities, ensuring that they are positioned to take advantage of favorable market conditions.

The current market environment presents several risk factors that necessitate careful consideration. Rising interest rates and inflationary pressures can adversely impact property values and rental income, squeezing profit margins for both fix-and-flip and buy-and-hold strategies. To mitigate these risks, investors should adopt a multifaceted approach that includes stress testing their financial models against different economic scenarios, maintaining robust contingency reserves, and securing competitive financing terms. Additionally, incorporating flexible exit strategies and hedging against rate fluctuations through fixed-rate financing options can provide a buffer against market volatility.

Adjusting acquisition criteria and underwriting standards is crucial in this uncertain environment. Investors should focus on properties with strong fundamentals, such as high-demand locations with resilient economic drivers and robust rental markets. Underwriting should prioritize conservative assumptions, particularly around rental income growth and occupancy rates, to ensure that investments remain viable even under less favorable conditions. Prime Property Funding’s offerings, such as DSCR loans, can support this approach by providing flexible financing solutions that accommodate varying cash flow scenarios and help investors maintain a healthy cushion between debt obligations and rental income.

Key Considerations for Investors

- Estimate holding costs accurately for fix-and-flip projects, including taxes, insurance, and utilities, to avoid unexpected expenses that can erode profits.

- Set a minimum spread threshold of 20% between purchase price and expected sale price to buffer against market fluctuations.

- Identify optimal exit timing by analyzing local sales trends and seasonality, aiming to sell during peak demand periods for maximum returns.

- Incorporate a 10% contingency plan into budgets for unforeseen repair costs or delays in fix-and-flip projects.

- Target a cap rate of 6% or higher for buy-and-hold properties to ensure attractive returns in light of current interest rate levels.

- Assume modest annual rent growth of 2-3% to account for inflation and potential economic slowdowns, ensuring realistic cash flow projections.

- Maintain a minimum DSCR cushion of 1.2 to safeguard against income disruptions and interest rate hikes.

- Utilize bridge financing with flexible draw schedules to manage cash flows efficiently and keep projects on track.

- Prioritize markets with strong job growth and population influx, such as Austin and Raleigh, for better risk-adjusted returns.

- Adopt stress testing in underwriting by considering worst-case scenarios, such as a sudden 10% drop in property values or rental income.

- Ensure portfolio diversification across asset classes and geographic regions to mitigate localized market risks.

- Implement comprehensive risk mitigation strategies, including maintaining adequate reserves, securing robust insurance policies, and conducting thorough tenant screenings.

By adopting these strategic measures, investors can navigate the complexities of the current real estate market with confidence, ensuring sustainable growth and resilience in their investment portfolios.

Resources

External References

Disclaimer: This market analysis is for informational purposes only and should not be considered financial or investment advice. Market conditions can change rapidly. Consult with a qualified financial or lending professional before making any decisions.