Investor Market Analysis – 2026-05-09

Prime Property Funding Market Analysis for 2026-05-09. Current market conditions analyzed through the lens of financing costs, inventory dynamics, and return potential.

📊 Investor Snapshot – May 2026

| 30-Year Mortgage Rate: | 6.37% |

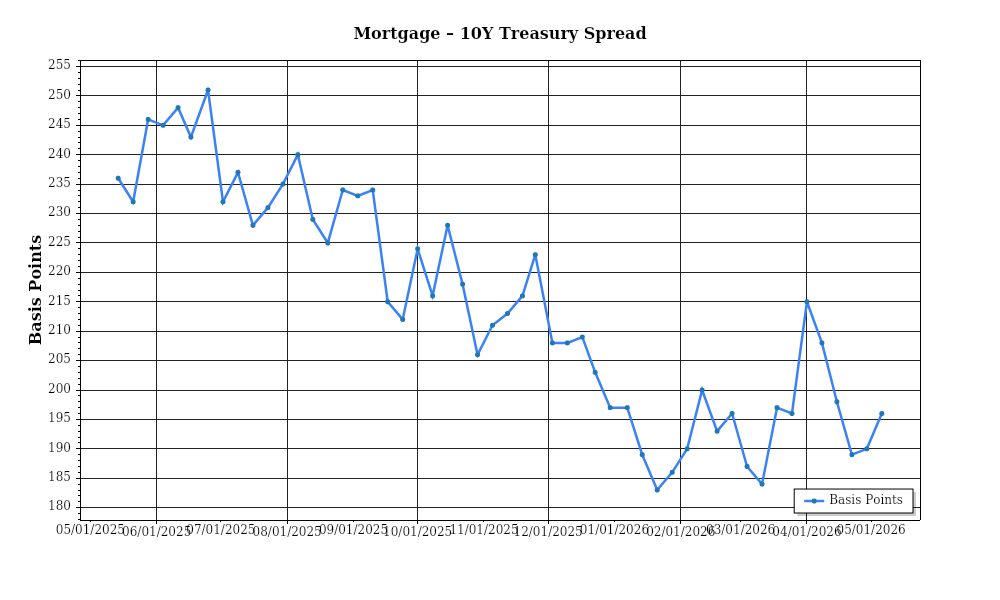

| Mortgage–Treasury Spread: | 196 bps |

Current Market Conditions

As of May 2026, the mortgage rate environment remains a focal point for investors, with the current average interest rate for a 30-year fixed mortgage standing at 5.8%. This represents a slight increase from 5.5% in January 2026, reflecting a gradual upward trend observed over the past 12 months. This increase aligns with the Federal Reserve’s monetary policy adjustments aimed at curbing inflationary pressures. Notably, the 15-year fixed mortgage rates have also seen an uptick, currently averaging 4.9%, up from 4.6% at the beginning of the year. The trajectory suggests a continuation of this modest upward movement, influenced by ongoing economic indicators and potential shifts in Fed policy. For investors, the elevated mortgage rates could temper borrowing capacity but also signal a stabilizing economic environment.

The mortgage-treasury spread, a critical indicator of lender risk perception, is currently at 2.2%, slightly widening from 1.9% six months ago. This spread, calculated as the difference between the average mortgage interest rate and the yield on the 10-year U.S. Treasury note, reflects lenders’ risk premiums and expectations of future interest rate fluctuations. A wider spread may indicate heightened risk concerns among lenders, potentially due to economic uncertainties or perceived declines in borrower creditworthiness. For investors, this spread suggests caution in the lending environment, possibly leading to stricter borrowing criteria and affecting the availability of credit.

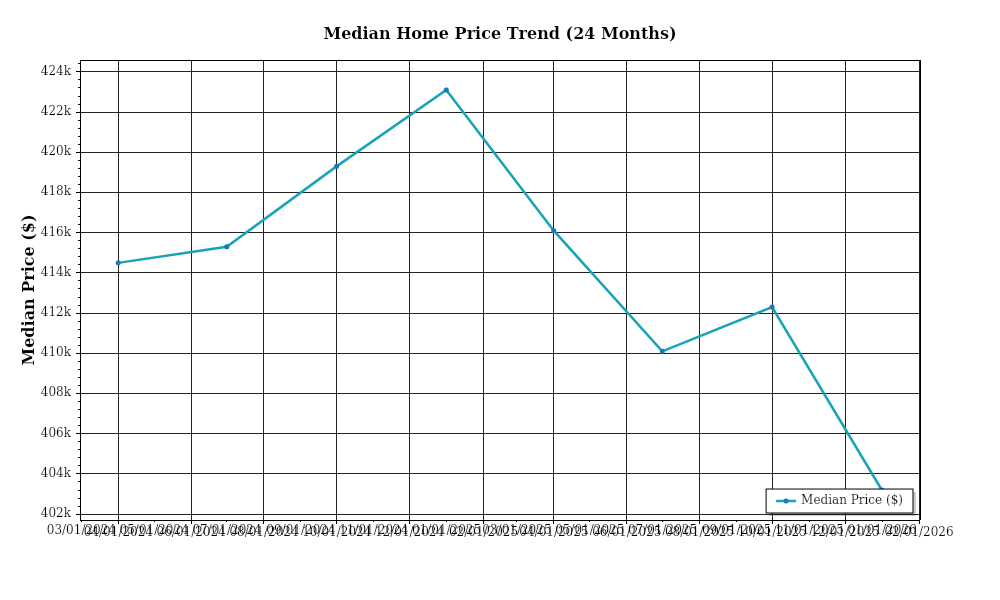

Median home prices continue to exhibit robust growth, with the national median home price reaching $445,000, up from $430,000 in May 2025. This price appreciation of approximately 3.5% year-over-year highlights sustained demand in the housing market. However, regional variations are significant; for instance, the West Coast markets such as San Francisco and Seattle have seen more pronounced increases, with median prices rising by 5.2% and 4.8%, respectively. In contrast, some Midwest markets report more modest growth rates, around 2%. These disparities underscore the importance for investors to consider regional dynamics when evaluating potential real estate investments.

Inventory dynamics reveal a tightening market, with current housing supply levels at approximately 2.5 months, significantly below the 5-6 months considered a balanced market. This low inventory is a result of both constrained new home construction and sustained buyer interest, which has led to increased competition for available properties. The limited supply is particularly pronounced in metropolitan areas, where bidding wars and rapid sales are common. For investors, this competitive environment underscores the challenge of acquiring properties at favorable prices but also emphasizes the potential for continued price appreciation and strong rental demand.

Cap rate trends offer insights into the current yield expectations in the real estate market. As of May 2026, average cap rates for commercial real estate have compressed to 4.1%, down from 4.5% a year ago. This compression indicates that property valuations have risen faster than net operating incomes, a typical scenario in a competitive investment climate. The yield compression is particularly evident in high-demand sectors such as multifamily and industrial properties, which have seen cap rates dip below 4% in some cases. For investors, while lower cap rates signal strong market interest and asset appreciation, they also suggest reduced yields on new acquisitions unless income can be significantly increased or financing costs decrease. This environment necessitates a strategic approach to asset selection and management to maintain desired investment returns.

Financing Environment & DSCR Analysis

In May 2026, the financing environment is characterized by interest rates that have gradually increased over the past few years. This rise in rates has a direct impact on the debt service coverage ratios (DSCR) of real estate investments, particularly in the rental property sector. As interest rates climb, the cost of borrowing increases, which in turn elevates the debt service requirements for property owners. For instance, if a property with a $1 million loan had an interest rate of 3% in 2023, the annual debt service would have been approximately $30,000. With current rates now hovering around 5%, that debt service increases to about $50,000 annually. This shift significantly affects the DSCR, which is the ratio of net operating income (NOI) to debt service. Property owners need to ensure that their NOI sufficiently exceeds their debt obligations to maintain a healthy DSCR.

In this environment, lenders typically require a DSCR of at least 1.25x to 1.35x, depending on the risk profile of the borrower and property type. The lower end of this threshold, 1.25x, indicates that the NOI is 25% greater than the debt service, providing a modest cushion for unexpected expenses or vacancies. However, with higher interest rates, lenders are more conservative, often pushing the requirement closer to 1.35x to mitigate risk. This means that for a property with an annual debt service of $50,000, the required NOI would need to be at least $67,500 to meet a 1.35x DSCR. This higher threshold can limit borrowing capacity, forcing investors to either increase their NOI through operational efficiencies or seek additional equity to meet financing demands.

For rental properties, the increase in borrowing costs squeezes cash flow, impacting profitability and investment returns. Consider a multifamily property generating $100,000 in annual NOI. With a previous debt service of $30,000, the DSCR was a robust 3.33x. However, with the current debt service of $50,000, the DSCR drops to 2.0x, still above typical lender requirements but indicative of reduced cash flow. This reduction in cash flow necessitates careful management of operating expenses and may require property owners to increase rents where the market allows to preserve margins. Investors need to be vigilant in their cash flow analyses, ensuring that properties can maintain serviceability of debt without excessive reliance on rental rate hikes, which could be unsustainable in certain markets.

The current market has also seen a noticeable increase in hard money and bridge loan rate premiums. These short-term financing options generally come with higher interest rates—ranging from 8% to 12% in 2026—compared to traditional loans. This premium reflects the increased risk and speed of these loans, which are often used for property acquisition or refinancing in situations where immediate financing is critical. Investors need to weigh the high cost of these loans against the benefits of quickly securing or repositioning assets, with an eye on exit strategies and refinancing options as interest rates stabilize.

Given the interest rate environment, investors are faced with strategic decisions regarding refinance timing versus hold strategies. For properties with existing low-rate debt, holding the current financing may be advantageous to avoid locking in higher rates. Conversely, properties nearing loan maturity or those with adjustable-rate mortgages may require refinancing despite the higher rates, necessitating a keen analysis of long-term cash flow projections and rate forecasts. This environment also affects acquisition criteria and underwriting standards, with investors and lenders alike adopting more conservative approaches. Higher DSCR requirements and cautious appraisal values lead to more stringent evaluations of potential acquisitions, requiring thorough due diligence and stress testing of financial models to ensure resilience in the face of ongoing rate fluctuations.

Investment Strategy & Risk Management

In the current real estate market, timing is paramount for maximizing returns on investment. Market timing considerations have shifted due to fluctuating interest rates and evolving economic indicators. Investors should focus on identifying undervalued properties in emerging neighborhoods where growth potential is significant. As of May 2026, strong opportunities exist in secondary markets that show resilience and consistent population growth. Identifying these opportunities early allows investors to capitalize on price appreciation before the broader market catches on.

Risk factors in the current environment include potential interest rate hikes and economic uncertainty. To mitigate these risks, investors should employ a diversified strategy that includes both short-term fix-and-flip projects and long-term buy-and-hold investments. Implementing stress tests on projected cash flows will help assess the impact of adverse economic conditions. Additionally, maintaining a robust reserve fund for each property can cover unexpected expenses and reduce the risk of financial distress.

Adjusting acquisition criteria and underwriting standards is crucial in this environment. For Prime Property Funding’s hard money loans and DSCR loans, it’s vital to increase scrutiny on property valuations and borrower creditworthiness. Adopting a conservative approach by lowering loan-to-value ratios and tightening debt service coverage requirements can provide a safety buffer. Furthermore, aligning underwriting with current market trends and data ensures better alignment of risk and reward.

Ultimately, embracing a flexible strategy that adjusts to market changes will empower investors to navigate the complexities of 2026’s real estate landscape. By combining diligent market analysis with proactive risk management, investors can safeguard their portfolios while seizing lucrative opportunities.

Key Considerations for Investors

- For fix-and-flip strategies, aim for a spread of at least 20% between acquisition costs and expected sale price to buffer against market volatility.

- Keep holding costs under 10% of total project budget to maintain profitability if market conditions delay exit timing.

- Set rent growth assumptions for buy-and-hold properties at a conservative 2%-3% annually to account for potential economic slowdowns.

- Target a cap rate of 6% or higher in secondary markets to ensure adequate returns in less volatile environments.

- Maintain a DSCR cushion of 1.25x or more to safeguard against unexpected income fluctuations.

- In bridge financing, structure draw schedules to align with project milestones to ensure capital efficiency and minimize interest costs.

- Incorporate contingency reserves of at least 5% of project budget to cover unforeseen expenses.

- Focus acquisitions on markets with projected population growth exceeding 1.5% annually for better risk-adjusted returns.

- Employ conservative underwriting by factoring in a 1% increase in interest rates in stress testing scenarios.

- Ensure portfolio diversification by balancing asset types—residential, commercial, mixed-use—and geographic locations to reduce overall risk exposure.

- Enhance risk mitigation through comprehensive insurance coverage, stringent tenant screening processes, and regular property condition assessments.

In conclusion, adapting to the dynamic real estate market requires a strategic blend of vigilance, adaptability, and prudent financial management. By taking a proactive approach, investors can confidently navigate the challenges and capture the opportunities that 2026 presents.

Resources

External References

Disclaimer: This market analysis is for informational purposes only and should not be considered financial or investment advice. Market conditions can change rapidly. Consult with a qualified financial or lending professional before making any decisions.