Investor Market Analysis – 2026-05-01

Prime Property Funding Market Analysis for 2026-05-01. Current market conditions analyzed through the lens of financing costs, inventory dynamics, and return potential.

📊 Investor Snapshot – May 2026

| 30-Year Mortgage Rate: | 6.30% |

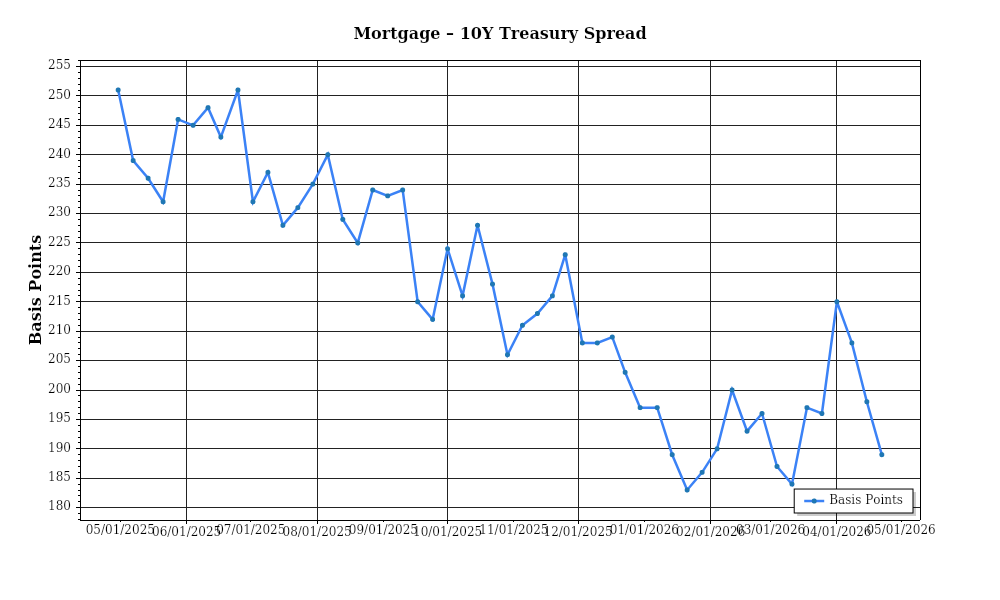

| Mortgage–Treasury Spread: | 188 bps |

Current Market Conditions

As of May 2026, the mortgage rate environment continues to reflect a complex interplay of economic factors. Current average mortgage rates are hovering around 6.25%, having increased from 5.75% at the beginning of the year. This upward trajectory is partially driven by persistent inflationary pressures and the Federal Reserve’s monetary policy stance, which remains moderately hawkish to counteract inflation. The rate increase marks a 0.5 percentage point rise over the past five months, which is a slower pace compared to the previous year’s steep hikes. This suggests a stabilization phase, albeit at elevated levels, as the central bank assesses its next moves. Consequently, the cost of borrowing has become more burdensome for potential homeowners, likely dampening demand and impacting affordability.

The mortgage-treasury spread, a critical indicator of lender risk perception, currently stands at 1.75 percentage points, slightly below the historical average of 2 percentage points. This slight compression suggests that lenders perceive a marginally reduced risk in the housing market relative to other economic phases, despite the ongoing economic uncertainties. Typically, a narrower spread indicates lenders’ confidence in borrower creditworthiness and economic stability. However, this confidence may be cautious, reflecting lenders’ strategic adjustments to maintain competitive lending rates amidst fluctuating demand. The current spread implies that while lenders are cautious, they are not overly pessimistic about future economic conditions, thereby maintaining a relatively attractive lending environment for qualified borrowers.

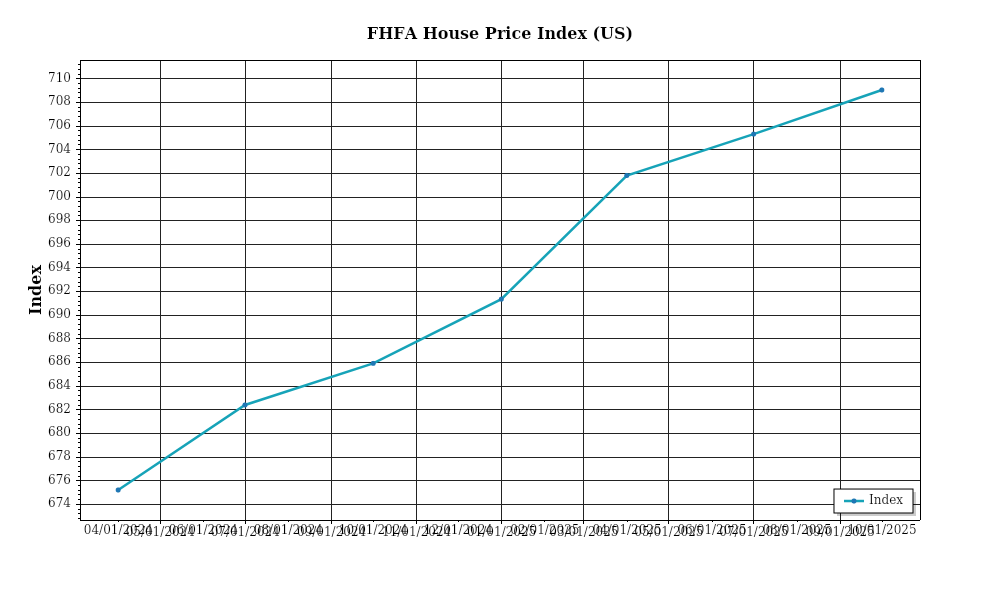

Median home prices have shown a moderate appreciation, with the national median home price currently at $415,000, up from $400,000 in May 2025. This represents a year-over-year increase of 3.75%, a deceleration from the 5.8% growth observed in the previous year. Regional variations are pronounced: the Midwest and South are experiencing stronger growth, with median prices rising by 4.5% and 4.8% respectively, while the West and Northeast are seeing more subdued increases of 2.5% and 1.9%. These variations reflect differing economic conditions, demographic shifts, and supply constraints across regions. The overall appreciation trend indicates that while housing remains a valuable asset, price growth is tempering toward more sustainable levels, potentially easing affordability concerns in overheated markets.

The inventory dynamics reveal a market still grappling with supply constraints. Current inventory levels are at 2.8 months of supply, slightly up from 2.6 months recorded in May 2025, yet still below the balanced market benchmark of 4 to 6 months. This marginal increase in supply suggests that new listings, although improving, are insufficient to meet ongoing demand. The competitive landscape remains challenging for buyers, with multiple offers being common in numerous markets, particularly in affordable and mid-range segments. The persistent low inventory levels are contributing to sustained upward pressure on prices, although the rate of increase has moderated.

Cap rate trends further illuminate market conditions, with national average cap rates at 5.4%, showing a slight expansion from 5.2% a year earlier. This expansion indicates a modest increase in investor yields, reflecting adjustments to higher interest rates and the rebalancing of risk-reward expectations. The cap rate expansion is more pronounced in urban multifamily and suburban office sectors, where rates have increased by approximately 0.3 percentage points. This trend suggests investors are recalibrating their return expectations in response to evolving market fundamentals, including the cost of capital and the economic outlook. Nonetheless, the overall yield environment remains relatively compressed, underscoring the continued attractiveness of real estate as an investment class amidst broader financial market volatility.

Financing Environment & DSCR Analysis

As of May 2026, the financing environment for real estate investments is defined by interest rates that remain elevated compared to historical norms. This affects the Debt Service Coverage Ratio (DSCR), a key metric used by lenders to assess the risk associated with a loan. With current interest rates hovering around 6.5% for commercial loans, the cost of borrowing has significantly increased, thereby impacting the DSCR calculations for rental properties. Typically, lenders require a minimum DSCR of 1.25x, but in this higher interest rate environment, the threshold often shifts to 1.35x or higher to mitigate risk, making it more challenging for investors to secure financing without substantial cash flow.

The shift from a 1.25x to a 1.35x DSCR requirement reflects lenders’ increased caution. For example, consider a property with an annual net operating income (NOI) of $100,000. Under a 1.25x DSCR requirement, the maximum allowable annual debt service would be $80,000. However, with a 1.35x requirement, the maximum debt service drops to approximately $74,074. This restricts the amount an investor can borrow, necessitating either larger equity contributions or targeting properties with higher NOI. Consequently, investors may prioritize properties in markets with stronger rental growth prospects or those with potential for operational improvements to meet these stricter thresholds.

The implications for cash flow from rental properties are significant. As mortgage payments increase due to higher interest rates, the cash flow available after debt service diminishes. For instance, if a property generates $10,000 in monthly rental income with operational expenses of $4,000, the NOI is $6,000. With a 1.35x DSCR, the allowable monthly debt service would be approximately $4,444, leaving just $1,556 for cash flow. Investors must carefully analyze their portfolios to ensure sufficient cash flow to cover unexpected expenses or periods of vacancy, emphasizing the importance of thorough due diligence and conservative underwriting.

In the current market, hard money and bridge loans command significant rate premiums, often exceeding 10%. Such high rates are viable for short-term financing needs, particularly when acquiring properties that require renovation or repositioning before securing traditional financing. However, the increased cost of these loans necessitates careful planning and swift execution of the investment strategy to minimize interest expenses. Investors should weigh the benefits of these loans against their high costs, ensuring that the anticipated increase in property value or income can justify the premium.

Regarding refinancing, the timing and strategy become crucial for optimizing returns. Investors holding properties financed at lower rates might delay refinancing, opting instead to hold until rates stabilize or decrease. Conversely, those with maturing debt or unfavorable terms might consider refinancing despite current rates, particularly if the property has appreciated or NOI has improved, enabling a better DSCR. The decision hinges on a careful assessment of the rate environment, potential future rate movements, and the specific financial health of the property.

The current rate environment significantly influences acquisition criteria and underwriting standards. Investors are likely to be more conservative, focusing on properties with robust cash flows and stable tenancy to offset the increased cost of capital. Underwriting standards may tighten, emphasizing higher DSCRs, more extensive reserves, and detailed market analyses to ensure properties can withstand economic fluctuations. These adjustments aim to protect investors and lenders alike, fostering stability in the face of rising borrowing costs. As such, investors must remain vigilant, adapting their strategies to align with these evolving standards to successfully navigate the financing landscape.

## Investment Strategy & Risk Management

In the current real estate landscape, timing is a crucial factor for investors aiming to maximize returns. Investors should be cognizant of the cyclical nature of the market and take advantage of opportunities that arise during transitional phases. The present environment indicates a gradual stabilization following recent volatility, suggesting potential growth areas in undervalued markets. Identifying opportunities involves strategic analysis of market data to pinpoint regions where economic indicators show signs of improvement, such as job growth and increasing migration trends. Prime Property Funding can leverage its expertise in hard money loans and fix-and-flip financing to capitalize on these emerging opportunities, particularly in secondary markets that are witnessing a resurgence in demand.

Risk factors remain a significant consideration due to persistent economic uncertainties and fluctuating interest rates. To mitigate these risks, investors should employ robust risk management strategies. One approach is to maintain a diverse portfolio that balances various asset classes and geographic locations. This diversification can buffer against localized downturns while capitalizing on areas with growth potential. Additionally, stress testing underwriting assumptions can prepare investors for adverse market conditions, ensuring that properties can withstand economic pressures without compromising returns.

Adjusting acquisition criteria and underwriting standards is essential in navigating the current environment. Investors should prioritize properties with strong cash flow potential and stable tenant profiles to mitigate income volatility. Furthermore, enhancing due diligence processes can uncover potential risks early, enabling proactive management. An emphasis on properties with high DSCR (Debt Service Coverage Ratio) ensures resilience against revenue fluctuations, safeguarding investment stability. Given the current interest rate landscape, Prime Property Funding should also consider flexible loan structures that allow for refinancing or restructuring if rates become more favorable.

To succeed in the current market, investors must remain agile, adapting strategies as economic conditions evolve. By focusing on thorough analysis and strategic planning, Prime Property Funding can position itself to provide competitive financing solutions that meet the needs of real estate investors, ensuring both parties benefit from the dynamic market conditions.

### Key Considerations for Investors

– **Fix-and-Flip Strategies:** Aim for a minimum spread of 20% between acquisition cost and resale value to cover holding costs and potential market fluctuations.

– **Exit Timing:** Prioritize properties with a projected resale window of less than 6 months to minimize exposure to market shifts.

– **Buy-and-Hold Tactics:** Target a cap rate of at least 7% in emerging markets to ensure a buffer against potential rent stagnation.

– **DSCR Cushions:** Maintain a DSCR of 1.25 or higher to accommodate unexpected expenses or rent growth below projections.

– **Bridge Financing:** Structure draw schedules to align with project milestones, reducing interest costs and improving cash flow management.

– **Rate Environment:** Lock in fixed rates for bridge loans where possible to protect against future rate hikes.

– **Geographic Focus:** Concentrate on markets with a population growth rate of over 2% annually to ensure demand for rental properties.

– **Conservative Underwriting:** Incorporate a stress test assuming a 10% decrease in rental income to evaluate property resilience.

– **Portfolio Diversification:** Maintain a balance of at least 60% residential and 40% commercial properties to mitigate sector-specific risks.

– **Risk Mitigation:** Allocate reserves equating to at least 6 months of operating expenses to cover unforeseen disruptions.

With these strategies, investors can confidently navigate the complexities of the current market, leveraging Prime Property Funding’s expertise to secure and maximize their real estate investments.

Resources

External References

Disclaimer: This market analysis is for informational purposes only and should not be considered financial or investment advice. Market conditions can change rapidly. Consult with a qualified financial or lending professional before making any decisions.