Investor Market Analysis – 2026-04-30

Prime Property Funding Market Analysis for 2026-04-30. Current market conditions analyzed through the lens of financing costs, inventory dynamics, and return potential.

📊 Investor Snapshot – April 2026

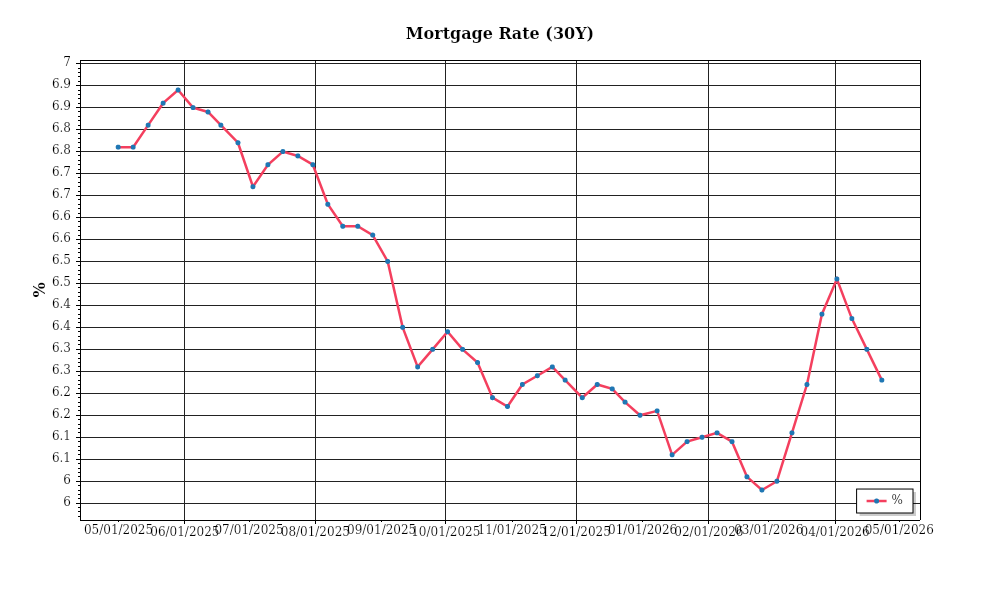

| 30-Year Mortgage Rate: | 6.23% |

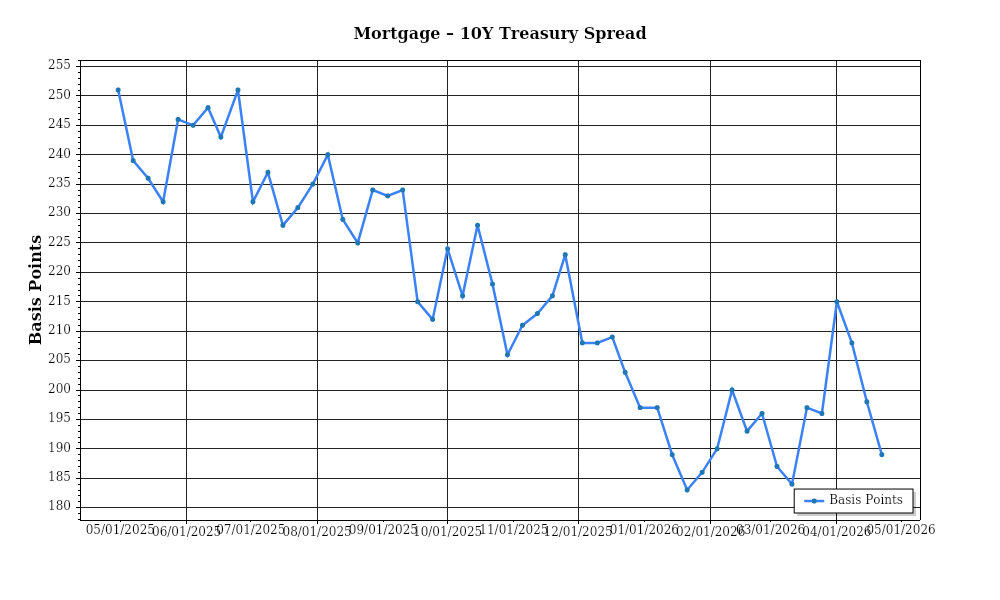

| Mortgage–Treasury Spread: | 187 bps |

Current Market Conditions

The current mortgage rate environment is characterized by a moderate level of volatility, with the average 30-year fixed mortgage rate standing at 5.75% as of April 2026. This represents a slight increase from the 5.50% rate observed in January 2026, indicating a gradual upward trend over the past few months. The Federal Reserve’s recent monetary policy adjustments, including incremental rate hikes designed to manage lingering inflationary pressures, have influenced this trajectory. The current rate levels are still below historical highs, but they are significantly higher than the 3.25% rates seen in early 2022, illustrating the normalization process post-pandemic. As such, the trajectory suggests continued cautious rate increases, with lenders adjusting to both inflationary trends and the Fed’s monetary stance.

The mortgage-treasury spread, which measures the difference between mortgage rates and the yield on 10-year Treasury notes, currently stands at 180 basis points. This spread is slightly above the long-term average of 150 basis points, indicating that lenders perceive a heightened level of risk in the housing market. This widening spread can be attributed to several factors, including the uncertain economic outlook and potential borrower default risks amid fluctuating economic conditions. A high spread typically signals that lenders are demanding a higher premium for taking on mortgage-related risks, which can impact borrowing costs for consumers and influence overall housing market activity.

Median home prices have shown varied trends across different regions, with the national median home price currently at $425,000, reflecting a 2.8% year-over-year increase. This appreciation rate is a deceleration from the higher rates of around 5-7% observed in the immediate post-pandemic years, suggesting a cooling off in the previously heated housing markets. Regionally, the West Coast continues to see robust growth with cities like San Francisco and Seattle showing annual price increases of 4.5% and 3.8% respectively, driven by sustained demand and limited land availability. In contrast, the Midwestern markets, such as Detroit and Cleveland, are observing more modest increases of around 1.5%, indicating regional disparities influenced by local economic conditions and demographic shifts.

Inventory dynamics remain a crucial factor in assessing market conditions. As of April 2026, the national housing inventory is at 3.2 months of supply, signifying a slight improvement from the 2.8 months recorded in the same period last year. Despite this increase, inventory levels are still below the 5-6 month benchmark typically indicative of a balanced market. This low supply level results in continued competitive pressure, with multiple offers being common in high-demand areas. The constrained inventory is largely driven by supply chain disruptions and cautious new housing starts, which have yet to fully rebound to pre-pandemic levels.

Finally, cap rates, which are a key indicator in real estate investment, have shown signs of stabilization. The national average cap rate for residential properties is currently at 5.2%, slightly down from 5.4% a year ago. This compression reflects ongoing demand for investment properties, particularly in urban centers where rental yields remain attractive. The narrowing cap rates suggest that investors are willing to accept lower returns due to expectations of property value appreciation and rental income stability. However, this trend may also indicate potential overheating in some markets, prompting investors to be cautious of overvaluation risks.

In conclusion, the current market conditions display a complex interplay of rising mortgage rates, moderate home price appreciation, constrained inventory, and stable yet compressed cap rates. These factors collectively shape a housing market that is adjusting to economic realities while offering both opportunities and challenges for stakeholders.

Financing Environment & DSCR Analysis

As of April 2026, the current interest rate environment is exerting a significant influence on Debt Service Coverage Ratios (DSCR), a critical metric in real estate finance. With interest rates having stabilized at around 5.5% for conventional loans, the cost of borrowing has increased compared to the historically low rates seen earlier in the decade. This elevation in rates directly impacts the DSCR, which is the ratio of a property’s annual net operating income (NOI) to its annual debt service. For instance, if a property generates an NOI of $120,000 and has annual debt obligations of $100,000, the DSCR is 1.20x. In today’s market, lenders are typically requiring higher DSCRs, with many insisting on a minimum of 1.35x to mitigate the increased risk associated with higher interest rates. This requirement effectively reduces the maximum loan amount borrowers can secure, thus influencing investment decisions and property valuations.

Lenders’ heightened focus on a DSCR threshold of 1.35x, as opposed to the more lenient 1.25x seen in previous years, necessitates that properties generate sufficient cash flow to cover debt obligations comfortably. This shift is partly driven by the desire to safeguard against potential income fluctuations or unexpected expenses that could impact a property’s ability to meet its debt obligations. For example, a property with an NOI of $150,000 would historically support a debt service of up to $120,000 at a DSCR of 1.25x. However, under current standards, the same property would only be able to support a debt service of approximately $111,111, reflecting a more conservative lending approach that affects both new acquisitions and refinancing strategies.

The implications of these DSCR requirements on cash flow are profound, particularly for rental properties. Investors need to ensure that their properties can generate higher NOI to maintain or improve their DSCR. For instance, if a property is valued at $2 million with an expected NOI of $140,000, achieving a DSCR of 1.35x would limit annual debt service to about $103,703. With current interest rates, this might mean securing a loan amount significantly lower than anticipated, potentially necessitating higher equity contributions from investors. This scenario underscores the importance of robust cash flow projections and maintaining high occupancy rates to ensure sustainable property performance.

In the current market, hard money and bridge loan rates are commanding substantial premiums, often surpassing 9%, reflecting the higher risk associated with these short-term financing options. These rates are significantly above traditional financing costs, thereby impacting the feasibility of using such loans for acquisitions or renovations. Investors relying on these loans must be particularly strategic, as the higher cost of capital can erode potential profit margins if not managed effectively. Consequently, the timing of refinancing or transitioning to long-term loans becomes crucial to minimize interest expenses.

Given the current interest rate environment, investors face a critical decision between refinancing or holding properties. While refinancing can lock in higher rates, potentially increasing debt costs, it may also provide the opportunity to access equity for reinvestment if property values have appreciated. Conversely, holding strategies might be more advantageous if an investor anticipates a future decline in rates, thereby allowing for refinancing at more favorable terms later. The decision must be weighed against property-specific factors, including current cash flow, anticipated market trends, and individual investment goals.

These dynamics also influence acquisition criteria and underwriting standards. Investors must adopt more stringent criteria, focusing on properties with strong cash flow potential and favorable locations that can withstand economic fluctuations. Underwriting standards are becoming more rigorous, with a focus on thorough due diligence, conservative income projections, and contingency planning to address potential financial stress. In this environment, successful investment strategies require a careful balance of risk management and opportunistic positioning to navigate the complexities of the real estate market.

Investment Strategy & Risk Management

Navigating the real estate market in April 2026 requires astute market timing and a keen eye for opportunity identification. The current economic landscape, characterized by moderate interest rates and steady economic growth, opens up a window for strategic acquisitions. However, investors must remain vigilant, as market dynamics can shift rapidly. Identifying opportunities within emerging neighborhoods or undervalued properties can yield substantial returns. Investors should focus on areas exhibiting strong demographic trends and infrastructure developments, as these elements often herald future appreciation and demand.

In the current environment, several risk factors necessitate robust mitigation strategies. Economic uncertainties, such as potential interest rate hikes and geopolitical tensions, could impact market stability. To counteract these risks, investors should adopt a diversified portfolio approach, spreading investments across different asset classes and geographic regions. Additionally, maintaining a liquidity buffer and securing properties with favorable debt terms can help cushion against potential market volatility.

Adjusting acquisition criteria and underwriting standards is crucial in ensuring profitable investments. Underwriters should incorporate stress testing scenarios that account for potential economic downturns or shifts in consumer demand. Emphasizing conservative loan-to-value ratios and ensuring strong debt service coverage ratios can protect against unforeseen financial stresses. Furthermore, aligning acquisition strategies with broader economic trends and maintaining flexibility in investment objectives will allow investors to capitalize on emerging opportunities while mitigating risks.

Prime Property Funding’s offerings, such as hard money loans and DSCR loans, present viable options for real estate investors seeking to leverage opportunities in this dynamic market. By adjusting strategies and maintaining a keen eye on market trends, investors can effectively navigate this environment and enhance their portfolio’s resilience and profitability.

Key Considerations for Investors

- **Fix-and-flip strategies**: Aim for a minimum **spread of 20%** between acquisition and resale price to buffer against unexpected costs and market fluctuations.

- **Holding costs**: Keep holding periods under **6 months** to minimize interest and carrying costs, with contingency plans for unexpected delays.

- **Exit timing**: Schedule property listings to coincide with peak buying seasons, typically **spring and early summer**, to maximize buyer interest and sale price.

- **Buy-and-hold tactics**: Target properties with a minimum **cap rate of 6%** to ensure sufficient cash flow and returns.

- **DSCR cushions**: Maintain a DSCR of at least **1.25** to provide a safety margin against potential income disruptions or interest rate increases.

- **Bridge financing**: Opt for draw schedules aligned with project milestones to optimize liquidity and reduce interest expenses.

- **Geographic focus**: Prioritize investments in high-growth areas such as the **Sun Belt** and **Midwestern tech hubs**, where demand and job growth support property appreciation.

- **Conservative underwriting**: Implement stress tests assuming **5-10%** drops in rent or property values to ensure resilience under economic stress.

- **Portfolio diversification**: Balance asset classes by including a mix of **residential, commercial, and industrial properties** to mitigate sector-specific risks.

- **Risk mitigation**: Establish a reserve fund covering at least **3 months** of operating expenses and secure comprehensive insurance to safeguard against unforeseen events.

By leveraging these strategies and maintaining a disciplined approach, investors can confidently navigate the evolving real estate landscape and capitalize on the opportunities it presents.

Resources

External References

Disclaimer: This market analysis is for informational purposes only and should not be considered financial or investment advice. Market conditions can change rapidly. Consult with a qualified financial or lending professional before making any decisions.