Investor Market Analysis – 2026-04-28

Prime Property Funding Market Analysis for 2026-04-28. Current market conditions analyzed through the lens of financing costs, inventory dynamics, and return potential.

📊 Investor Snapshot – April 2026

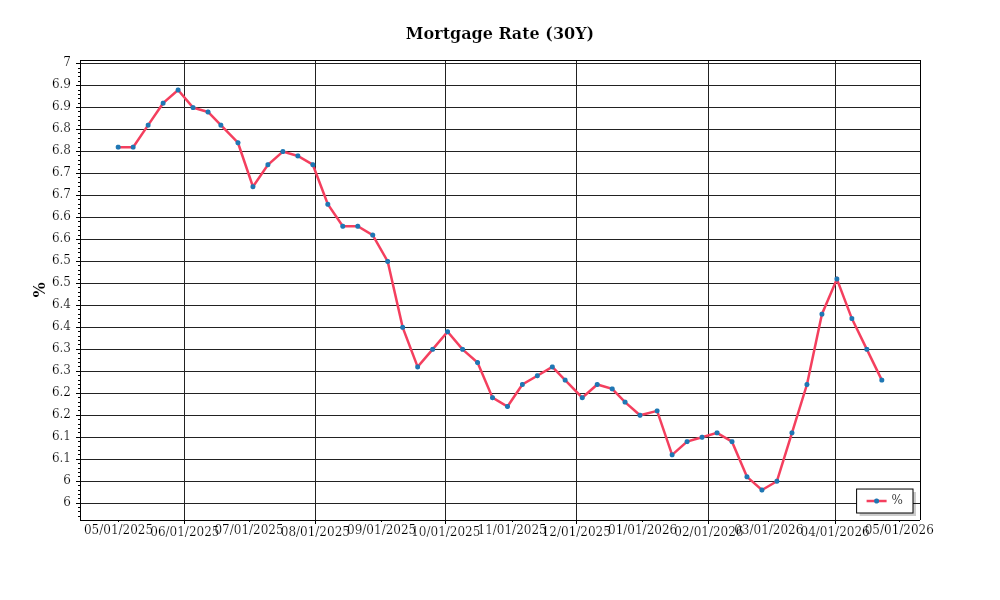

| 30-Year Mortgage Rate: | 6.23% |

| Mortgage–Treasury Spread: | 192 bps |

Current Market Conditions

As of April 2026, the mortgage rate environment reflects both stability and volatility in the economic landscape. The national average for a 30-year fixed mortgage rate is currently at 5.1%, a slight decrease from the 5.3% observed in March 2026. This decrease marks a continuation of the downward trend seen over the past six months, where rates have oscillated between 4.9% and 5.5%. The Federal Reserve’s recent decision to maintain interest rates has contributed to this stabilization, although market analysts suggest potential upward pressure in the latter half of the year as inflationary concerns persist. The current rates remain historically low, encouraging refinancing and new purchases, yet the ongoing fluctuation signals caution among lenders and borrowers alike.

The mortgage-treasury spread, a critical indicator of lender risk perception, currently stands at 1.8%. This spread has remained relatively constant over the past few months, slightly below the long-term average of 2%. A narrower spread typically suggests that lenders perceive lower risk in the housing market, reflecting confidence in borrower creditworthiness and the broader economic conditions. However, the spread’s stability amidst economic uncertainties, such as fluctuating employment rates and global economic tensions, suggests that lenders are cautiously optimistic. This balance between risk and stability indicates that while lenders are maintaining competitive lending practices, they remain vigilant against potential economic disruptions.

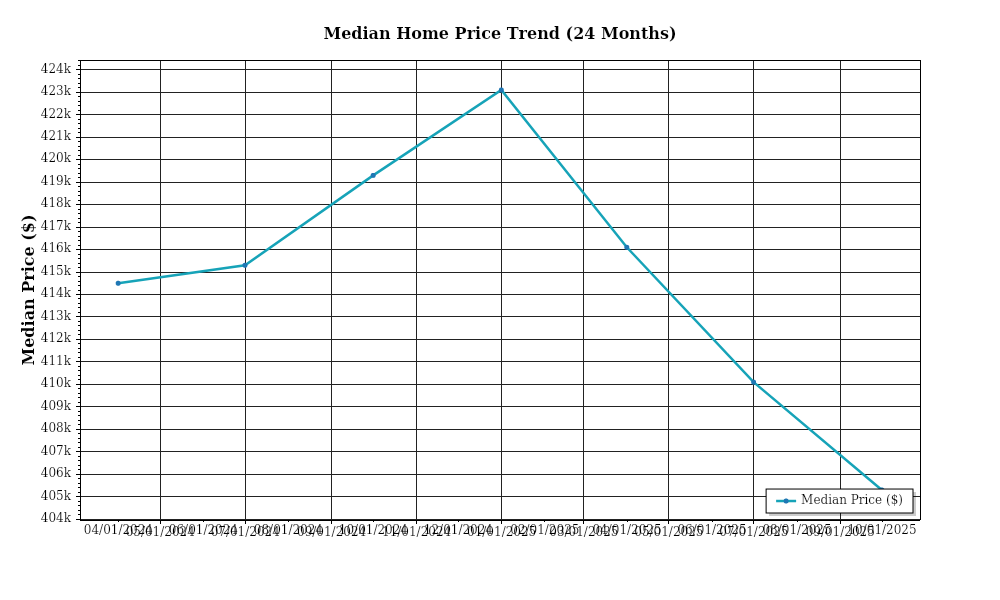

Examining median home price trends, the national median home price as of April 2026 is $435,000, representing an annual appreciation rate of 6.2%. This rate of appreciation, although robust, shows a deceleration compared to the double-digit growth rates seen in the years following the pandemic. Regionally, significant variations persist: the South has experienced the highest growth, with states like Florida and Texas reporting increases of 8% and 7.5%, respectively. In contrast, the Midwest, with its historically stable market, reports a more modest increase of 4.3%. These regional disparities highlight shifting demographics and economic conditions, with the South benefiting from continued migration and job growth, while the Midwest remains attractive for its affordability and slower-paced lifestyle.

Inventory dynamics remain a pivotal factor in current market conditions. Nationally, housing supply levels are sitting at 3.2 months, a slight improvement from the 3 months reported in the previous quarter, yet still below the balanced market threshold of approximately 6 months. This limited supply continues to fuel competition, particularly in urban and suburban areas where demand remains high. Multiple-offer situations are common, with many homes selling above asking prices. However, new construction is beginning to catch up; permits for new residential buildings have increased by 12% year-over-year, suggesting relief may be on the horizon if these trends continue.

Finally, cap rate trends reveal a slight compression, with the national average cap rate for multifamily properties currently at 5.4%, down from 5.6% in April 2025. This compression indicates increased property valuations relative to net operating income, a sign of investor confidence in continued rental demand and property appreciation. However, the narrowing margin also suggests that investors are willing to accept lower yields in exchange for the perceived safety and stability of real estate assets, particularly in the face of volatile equities markets. This trend is most pronounced in high-demand metropolitan areas where investor competition remains fierce, driving prices up and yields down.

In conclusion, the current real estate market is characterized by a mix of cautious optimism and competitive dynamics. Mortgage rates, while stable, remain susceptible to economic shifts, and the mortgage-treasury spread reflects a balanced perception of risk. Median home prices continue to appreciate, though at varied regional rates, while inventory shortages persist but show potential improvement. Cap rate compression underscores strong investor interest, albeit with lower yield expectations. Collectively, these factors paint a complex picture of the market, offering both opportunities and challenges for stakeholders.

Financing Environment & DSCR Analysis

The financing environment in April 2026 remains notably influenced by the persistently high-interest rates, which have a profound impact on the Debt Service Coverage Ratios (DSCR) critical for real estate investment evaluations. Currently, interest rates hover around 6.5% for traditional mortgages, exerting pressure on the DSCR calculations. This rate environment necessitates a higher income from rental properties to meet the debt obligations, thus straining cash flows. The effect is more pronounced for investors who financed properties at lower rates in preceding years and are now facing refinancing at current, elevated rates. Consequently, the ability to maintain adequate DSCR becomes challenging, especially for properties with marginal cash flows.

In this environment, lenders are increasingly stringent, often requiring a minimum DSCR of 1.35x instead of the traditional 1.25x. The higher threshold reflects the lenders’ need to mitigate risk in a volatile financial climate. For example, consider a multifamily property generating $100,000 annually in net operating income (NOI). Under the 1.25x DSCR requirement, the maximum debt service would be $80,000. However, with a 1.35x requirement, the allowable debt service drops to approximately $74,074, effectively reducing leverage and potentially necessitating additional equity or a reduced purchase price to meet financing criteria.

The cash flow implications for rental properties are significant. For instance, a property with an NOI of $200,000 and facing a debt service of $148,148 under a 1.35x DSCR must ensure revenues remain stable or grow. If interest rates were to rise further or rental income declines, the property could quickly fall below the required DSCR, jeopardizing financing eligibility. In practical terms, investors might face the need to enhance revenue streams through value-add strategies or cost-reduction measures to sustain compliance with DSCR thresholds.

In the current market, hard money and bridge loan rates carry substantial premiums, often exceeding traditional financing rates by 3-5 percentage points. This places these loans in the 9-11% range, making them a costly option for short-term financing needs. The high rates reflect the increased risk these lenders assume, and they can significantly erode profits if used unwisely. For example, an investor utilizing a bridge loan at 10% to acquire a property must have a clear, expedited strategy for either refinancing into a conventional loan or executing a profitable exit to avoid excessive interest costs eroding potential returns.

When considering refinance timing versus hold strategies, the current rate environment suggests a cautious approach. Investors must weigh the potential benefits of locking in current rates against the possibility of future rate reductions. Properties purchased or refinanced at lower rates in previous years may benefit more from a hold strategy if current refinancing results in a higher cost of debt. However, properties with adjustable-rate mortgages facing upward resets might necessitate refinancing to stabilize debt service obligations, even at today’s higher rates.

The impact on acquisition criteria and underwriting standards is profound. Investors must adopt conservative underwriting practices, prioritizing properties with strong cash flow potential and resilience to withstand economic fluctuations. Acquisition criteria now demand greater scrutiny of market conditions, tenant profiles, and long-term growth projections to ensure compliance with stricter DSCR requirements. Underwriting standards also emphasize robust contingency plans and sensitivity analyses to prepare for adverse market shifts, ensuring that investments remain viable under various scenarios.

In summary, the current financing environment necessitates a strategic, analytical approach to real estate investment, with a keen focus on maintaining healthy DSCRs amid high-interest rates, ensuring cash flow stability, and adhering to stringent acquisition and underwriting criteria.

Investment Strategy & Risk Management

In the current real estate landscape of April 2026, investors are navigating a market characterized by fluctuating interest rates, evolving consumer preferences, and regional economic disparities. Timing is crucial, and opportunities often arise swiftly. The key to successful investment lies in identifying these opportunities early, particularly in emerging markets, while being mindful of cyclical economic patterns. Investors should focus on markets with strong economic fundamentals, like job growth and population influx, which are more likely to yield favorable returns. Monitoring these indicators helps in timing acquisitions to coincide with market upswings.

However, the present environment is fraught with risk factors that require careful navigation. Rising construction costs and labor shortages continue to challenge fix-and-flip strategies, while interest rate volatility impacts financing costs and potentially, property valuations. Mitigation strategies include maintaining a diverse portfolio to spread risk, employing conservative underwriting standards that stress-test assumptions against adverse market scenarios, and building adequate contingency reserves. A focus on liquidity and flexible exit strategies can also buffer against unexpected market shifts.

Adjusting acquisition criteria and underwriting standards is essential to align with current market conditions. Investors should prioritize properties with strong cash flow potential and value-add opportunities, even if they come at a premium. Underwriting should incorporate conservative rent growth assumptions and stress-tested cap rates to ensure financial viability under various scenarios. Additionally, a heightened focus on tenant quality and property condition can mitigate risks associated with rental income volatility.

Prime Property Funding, specializing in hard money loans, fix-and-flip financing, and DSCR loans, should advocate for a strategic approach that balances aggressive pursuit of high-return opportunities with a cautious assessment of risks. By emphasizing market research, investor education, and flexible financing solutions, the firm can empower investors to capitalize on market opportunities while safeguarding their investments.

Key Considerations for Investors

- Fix-and-Flip Strategies: Maintain holding costs under 10% of projected sale price; anticipate potential spread risk by adding a 15% buffer to expected renovation costs.

- Exit Timing for Flips: Align renovation completion with peak selling seasons, typically spring and early fall, to maximize buyer interest and sale price.

- Buy-and-Hold Tactics: Target cap rates above 6% in secondary markets, ensuring DSCR remains above 1.25 to buffer against potential rent declines.

- Rent Growth Assumptions: Limit to 3-4% per annum in underwriting models to account for economic uncertainties and inflation impacts.

- Bridge Financing: Secure fixed-rate loans where possible; establish draw schedules that allow for flexibility in project pacing and unexpected expenses.

- Geographic Focus: Prioritize investments in regions with a minimum 5% annual population growth rate and robust job market indicators.

- Conservative Underwriting: Stress test financial models against a 2% increase in interest rates to ensure sustainability under tighter credit conditions.

- Portfolio Diversification: Aim for a mix of asset classes, with no more than 30% investment in any single market to enhance risk-adjusted returns.

- Risk Mitigation: Maintain cash reserves equal to six months of operating expenses; enforce strict tenant screening processes to protect rental income streams.

In conclusion, while the real estate market of 2026 presents challenges, it also offers abundant opportunities for those well-prepared to act. By employing diligent research and robust risk management strategies, investors can confidently navigate the market and achieve sustainable growth.

Resources

External References

Disclaimer: This market analysis is for informational purposes only and should not be considered financial or investment advice. Market conditions can change rapidly. Consult with a qualified financial or lending professional before making any decisions.