Investor Market Analysis – 2026-04-25

Prime Property Funding Market Analysis for 2026-04-25. Current market conditions analyzed through the lens of financing costs, inventory dynamics, and return potential.

📊 Investor Snapshot – April 2026

| 30-Year Mortgage Rate: | 6.23% |

| Mortgage–Treasury Spread: | 189 bps |

Current Market Conditions

As of April 2026, the mortgage rate environment presents a critical factor for real estate investors, with rates currently hovering around 5.75% for a standard 30-year fixed mortgage. This marks a notable decrease from the highs of 6.5% seen late last year, reflecting a gradual easing in monetary policy as inflationary pressures begin to soften. Over the past six months, mortgage rates have experienced a downward trajectory, decreasing by approximately 0.75%, which has increased affordability for potential homebuyers. This trend is likely influenced by the Federal Reserve’s decision to maintain the federal funds rate at 4.5%, coupled with moderate economic growth projections. The current trajectory suggests a stable to slightly declining rate environment, which could fuel increased housing demand if sustained.

Analyzing the mortgage-treasury spread, which currently stands at 1.8%, provides insight into lender risk perceptions. Historically, this spread averages around 1.5%, indicating an elevated risk premium currently factored into mortgage rates. The wider spread suggests lenders remain cautious, reflecting broader economic uncertainties and potential defaults. However, the recent narrowing from a peak spread of 2.2% earlier this year indicates a cautiously optimistic shift in lender sentiment, as macroeconomic conditions stabilize. This reduced spread could translate into marginally lower borrowing costs over the coming months, provided no significant economic disruptions occur.

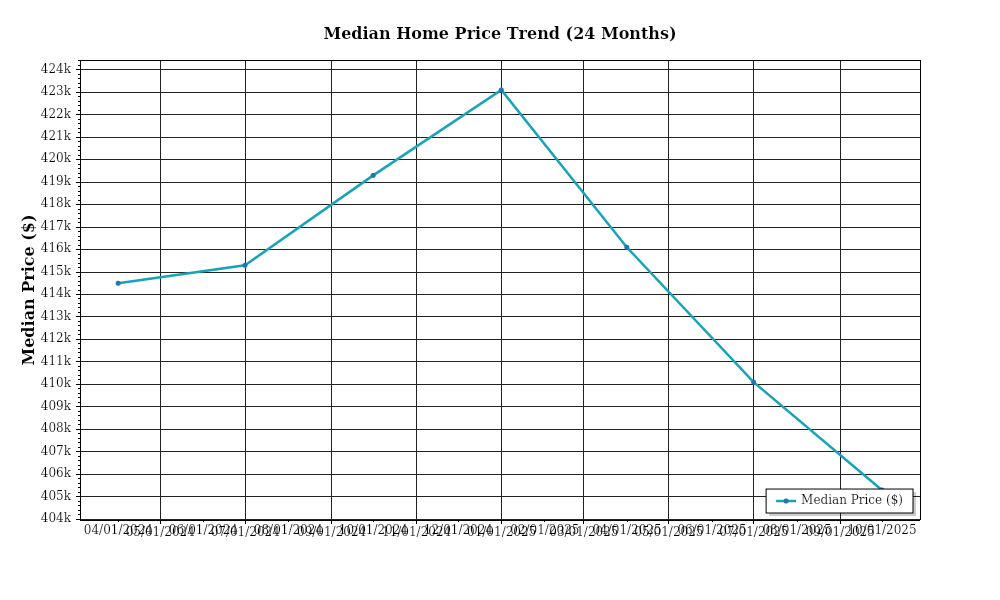

The median home price across the United States stands at $425,000, reflecting a year-over-year appreciation rate of approximately 4.8%. This rate of appreciation, while slower than the double-digit increases seen in previous years, indicates a market moving towards more sustainable price growth. Regional variations are pronounced, with the Southeast experiencing the highest median price increase of 6.5%, driven by strong population growth and demand in states like Florida and Georgia. In contrast, the Pacific Northwest has seen a more modest appreciation of 3.2%, reflecting market saturation and affordability constraints. Such regional disparities highlight the importance for investors to consider local market conditions when making acquisition decisions.

Inventory dynamics continue to play a pivotal role in shaping market conditions. Nationwide, housing supply remains tight, with a current inventory level of 2.5 months, well below the balanced market threshold of 6 months. This persistent undersupply contributes to competitive acquisition conditions, where multiple offers and bidding wars are prevalent in desirable areas. The limited inventory is exacerbated by a slowdown in new construction, with housing starts down by 7% year-over-year, as builders grapple with labor shortages and increased material costs. The sustained low inventory levels suggest continued upward pressure on home prices, despite the recent deceleration in appreciation rates.

Cap rate trends are also a focal point for investors seeking to understand yield dynamics in the current market. The average cap rate for multifamily properties is currently at 5.3%, showing a slight compression from 5.5% at the same time last year. This compression reflects strong investor demand and confidence in income-producing properties, even as property values rise. Yield compression signals that investors are willing to accept lower returns in exchange for perceived stability and long-term growth prospects in the rental market. This trend is evident across major urban centers, where cap rates have fallen below 5%, driven by robust demand for rental housing. Investors should remain vigilant, however, as further compression could heighten vulnerability to interest rate shifts and economic downturns.

Overall, the current market conditions reflect a complex interplay of easing mortgage rates, tight inventory, and regional price disparities. Investors must navigate these dynamics carefully, balancing the potential for appreciation with the risks associated with elevated property values and compressed yields.

Financing Environment & DSCR Analysis

As of April 2026, the financing environment for real estate investments remains complex, influenced by prevailing interest rates and stringent lending standards. **Current interest rates**, which have stabilized at approximately 6.5% for conventional loans, significantly affect the **Debt Service Coverage Ratio (DSCR)**, a critical metric used by lenders to assess the viability of a loan. The DSCR is calculated by dividing a property’s annual net operating income (NOI) by its annual debt service. Given the current rates, the cost of borrowing has increased, leading to a heightened focus on DSCR to ensure that properties generate sufficient cash flow to cover debt obligations. Lenders are generally requiring a minimum DSCR of 1.25x, though more conservative institutions are pushing for a 1.35x threshold to mitigate risk. This means for every dollar of debt service, properties must generate at least $1.25 to $1.35 in NOI, depending on the lender’s appetite for risk.

This increase in DSCR requirements has notable cash flow implications for rental properties. Consider a multifamily property with an annual debt service of $100,000. To meet a 1.25x DSCR, the property must produce an NOI of at least $125,000. At the 1.35x threshold, the required NOI rises to $135,000. These heightened DSCR requirements necessitate either higher rental income or reduced operating expenses to achieve the target ratios. For example, if a property currently generates $120,000 in NOI, it falls short of both DSCR thresholds. Investors may need to explore strategies such as increasing rental rates, which is viable given the current demand in rental markets, or reducing operational costs through efficiency improvements to enhance cash flow and meet lender requirements.

In the realm of alternative financing, **hard money and bridge loan rates** are also shaped by the current interest environment. These short-term loans, typically used for property acquisition and refurbishment, command a premium over conventional financing due to their higher risk and shorter durations. Rates for hard money loans are hovering between 9% and 12%, with bridge loans slightly lower at 8% to 10%. These elevated rates reflect the increased risk perceived by lenders in the current market. Investors utilizing these financing options must factor in these premiums when calculating potential returns and ensure that the anticipated appreciation or rental income justifies the higher cost of capital.

Given the current rate environment, investors face strategic decisions regarding **refinance timing versus hold strategies**. With interest rates expected to remain stable, albeit at a higher level, the potential for refinancing to achieve lower rates in the near future appears limited. Therefore, investors may opt to hold properties longer, capitalizing on appreciation and increased rental income to improve cash flow before considering refinancing. However, if significant equity has been built up, refinancing could still be advantageous to access capital for new acquisitions or property improvements, despite the higher rates.

The impact of the current financing environment extends to **acquisition criteria and underwriting standards**. Investors are increasingly scrutinizing potential deals, focusing on properties with strong cash flow and growth potential to meet higher DSCR requirements. Underwriting standards have tightened, with lenders conducting more rigorous evaluations of property income projections and stress-testing for potential interest rate hikes. This cautious approach necessitates a thorough due diligence process, where investors must accurately project future income, account for potential increases in operating expenses, and ensure that properties can sustain higher debt service burdens. As a result, properties in high-demand locations with stable tenant bases and strong market fundamentals are becoming increasingly attractive, as they are more likely to meet stringent underwriting standards and achieve favorable financing terms.

Investment Strategy & Risk Management

In the current real estate landscape, market timing and opportunity identification remain pivotal for investors aiming to maximize returns. As we move through 2026, economic indicators suggest a nuanced approach to timing acquisitions. While inflationary pressures have eased, interest rates remain elevated compared to pre-pandemic levels. This environment necessitates a focus on identifying undervalued properties with potential for appreciation, particularly in markets with strong employment growth and infrastructure investment. Investors should capitalize on seasonal trends, where historically slower winter months offer opportunities to acquire properties at lower price points.

Risk factors in today’s market include persistent interest rate volatility, uncertain economic growth, and evolving regulatory landscapes. To mitigate these risks, investors should adopt robust stress-testing in their financial models, incorporating various economic scenarios. Maintaining liquidity through adequate contingency reserves is essential, allowing investors to weather any unforeseen market disruptions. Additionally, diversifying portfolios across asset classes and geographies can buffer against localized downturns, ensuring stable cash flows.

Adjusting acquisition criteria and underwriting standards is crucial in this fluctuating market. With higher borrowing costs, property values and corresponding rental yields must align to achieve desired returns. Investors should refine their cap rate targets to reflect market realities, ensuring acquisitions meet or exceed a minimum threshold for profitability. Utilizing conservative assumptions for rent growth and operating expenses will safeguard against overestimating returns. Furthermore, underwriters should emphasize the importance of tenant quality and property condition, setting elevated standards to minimize vacancy risks and maintenance costs.

Key Considerations for Investors

- For fix-and-flip strategies, aim for a minimum spread of 20% between purchase price and after-repair value to cover holding costs and potential market shifts.

- Hold contingency reserves equal to at least 15% of the total project budget to manage unexpected expenses effectively.

- In buy-and-hold tactics, target a minimum cap rate of 6% to ensure profitability in higher interest environments.

- Assume a conservative rent growth rate of 2-3% annually to buffer against economic slowdowns.

- Maintain a Debt Service Coverage Ratio (DSCR) cushion of 1.25x to safeguard against income fluctuations.

- For bridge financing, prioritize projects with clear exit strategies and ensure draw schedules align with project milestones to optimize cash flow.

- Focus on markets with a population growth rate exceeding 1.5% annually, which typically offer better risk-adjusted returns.

- Conduct thorough stress testing by factoring a 1-2% increase in interest rates to evaluate the impact on cash flows and asset valuations.

- Ensure portfolio diversification by maintaining a balanced mix of residential and commercial properties across at least three different geographic regions.

- Implement strong risk mitigation practices, such as maintaining reserves equal to six months of operating expenses and securing comprehensive insurance coverage.

By adhering to these strategic guidelines and maintaining a vigilant approach to risk management, investors can confidently navigate the complexities of the current real estate market. This disciplined strategy not only preserves capital but positions investors to seize emerging opportunities with agility and foresight.

Resources

External References

Disclaimer: This market analysis is for informational purposes only and should not be considered financial or investment advice. Market conditions can change rapidly. Consult with a qualified financial or lending professional before making any decisions.