Investor Market Analysis – 2026-04-24

Prime Property Funding Market Analysis for 2026-04-24. Current market conditions analyzed through the lens of financing costs, inventory dynamics, and return potential.

📊 Investor Snapshot – April 2026

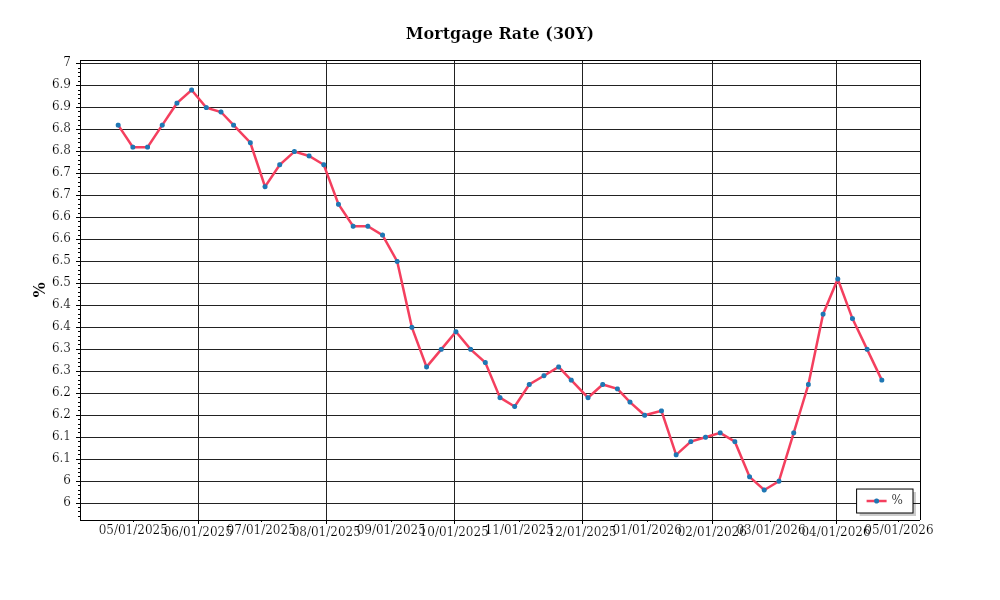

| 30-Year Mortgage Rate: | 6.23% |

| Mortgage–Treasury Spread: | 193 bps |

Current Market Conditions

As of April 2026, the mortgage rate environment is experiencing a period of relative stability, with the average 30-year fixed mortgage rate hovering around 6.25%. This is a slight decrease from the 6.5% observed in March 2026, reflecting a modest downward correction from the peaks seen in 2025, when rates surpassed 7%. The slight decline in rates can be attributed to a combination of the Federal Reserve’s cautious approach to monetary policy and softening inflationary pressures. While the current rates are higher than the historical lows of sub-3% experienced during the pandemic, they are still considered moderate in the larger historical context. Forward-looking indicators suggest that mortgage rates may remain relatively stable in the short term, assuming no major macroeconomic disruptions.

Analyzing the mortgage-treasury spread provides further insight into the risk perception of lenders. Currently, the spread between the 30-year mortgage rate and the 10-year Treasury yield is approximately 2.3%, slightly above the long-term average of 1.8%. This elevated spread indicates that lenders are pricing in higher risk premiums, possibly due to lingering concerns about economic volatility and potential defaults. Historically, a spread of this magnitude suggests lenders are cautious, perhaps influenced by geopolitical uncertainties and the potential for economic slowdowns in key global markets. The spread’s trajectory will be a critical indicator of lender sentiment and could impact borrowing costs if it widens further.

Examining median home price trends reveals a complex landscape. As of April 2026, the national median home price stands at $425,000, reflecting a year-over-year appreciation rate of approximately 5%. This rate of appreciation is a deceleration from the double-digit increases witnessed in the post-pandemic housing boom. Regional variations are notable; the West Coast continues to see higher-than-average price growth, with cities like San Francisco and Seattle experiencing annual increases of 7% and 6.5% respectively. In contrast, some Midwestern markets, such as Cleveland and Detroit, report more modest gains of 2% to 3%. These disparities highlight the differing economic conditions and demand drivers across regions, with tech industry hubs maintaining robust demand and affordability remaining a key factor in slower-growth areas.

Inventory dynamics are another crucial factor shaping the current market. The national housing supply is around 2.8 months, indicating a seller’s market, but showing some improvement from the 2 months recorded in 2025. Despite the modest increase in inventory, competition for acquisitions remains fierce, particularly in metropolitan areas where new construction has not kept pace with demand. The constrained supply is partly due to ongoing labor shortages and elevated construction costs, which continue to hamper new home builds. Market balance is slowly improving, but buyers still face significant competition, and bidding wars are commonplace in high-demand areas.

Finally, cap rate trends offer insights into the investment landscape in commercial real estate. Current cap rates for prime multifamily properties average around 4.5%, while office spaces are slightly higher at 5.2%. These figures represent a slight increase from the previous year, indicating a trend of yield expansion. This movement suggests investors are demanding higher returns to compensate for perceived risks, which could be attributed to economic uncertainties and evolving work-from-home dynamics affecting office space demand. The compression observed in previous years has reversed slightly, aligning with broader expectations of a more balanced market in the near term. Investors are closely monitoring cap rate movements as they reflect broader economic trends and shifts in market sentiment.

Financing Environment & DSCR Analysis

As of April 2026, the financing environment presents a nuanced landscape for real estate investors, particularly in how current interest rates influence debt service coverage ratios (DSCR). Interest rates have steadily increased over the past few years, resulting in a more challenging borrowing environment. Higher rates directly impact the DSCR by increasing the cost of debt, which in turn requires properties to generate more income to maintain a satisfactory DSCR. For instance, if a rental property has a mortgage at a 5% interest rate, and the rate increases to 6%, the monthly mortgage payment could rise significantly, thereby requiring higher rental income to meet the DSCR requirements.

In the current market, lenders typically impose DSCR requirements ranging from 1.25x to 1.35x. This means that the net operating income (NOI) must be at least 1.25 to 1.35 times the mortgage payment. For example, if a property has a monthly debt obligation of $10,000, the NOI must be between $12,500 and $13,500 to satisfy these requirements. The higher threshold of 1.35x is becoming more common as lenders seek to mitigate risk in an environment of rising interest rates. This shift demands that property owners either increase rents or reduce expenses to enhance the NOI, which can be challenging in a competitive rental market.

The implications for cash flow are significant. Consider a property generating $15,000 in monthly NOI with a 1.25x DSCR requirement. With a 5% mortgage rate, the debt service might be $12,000, leaving $3,000 as cash flow. However, if rates rise to 6%, the debt service could increase to $13,500, reducing cash flow to $1,500. This reduction affects the owner’s ability to invest in property improvements or to save for future expenses, highlighting the importance of strategic financial planning. Investors must be vigilant in adjusting rents or exploring operational efficiencies to maintain healthy cash flows.

In the realm of hard money and bridge loans, interest rate premiums are particularly pronounced. These short-term financing options are typically used for property acquisitions or renovations and come with rates that can be several percentage points higher than conventional loans. Currently, hard money loans may carry rates of 9% to 12%, reflecting the elevated risk and quick turnaround expected by lenders. This premium necessitates careful consideration of the cost-benefit balance. Investors must ensure that the anticipated increase in property value or income justifies the higher financing costs.

Timing for refinancing versus holding strategies is critical in the current rate environment. With rates on an upward trajectory, the decision to refinance should be based on a comprehensive analysis of potential interest savings against closing costs and other fees. Conversely, holding onto existing low-rate debt might be advantageous if refinancing does not yield significant benefits. However, investors should also consider the opportunity cost of not accessing equity for new investments, which may offer higher returns despite the higher cost of capital.

Finally, the current interest rate climate influences acquisition criteria and underwriting standards. Investors are increasingly cautious, with a heightened focus on properties that demonstrate strong cash flows and the potential for NOI growth. Underwriting standards are more stringent, with lenders scrutinizing borrowers’ ability to meet higher DSCR thresholds. This environment favors well-capitalized investors who can demonstrate a track record of managing properties efficiently and achieving robust financial performance.

In conclusion, the financing environment as of April 2026 demands careful consideration of DSCR impacts, strategic refinancing decisions, and stringent acquisition criteria. Investors must navigate higher interest rates with a focus on maintaining cash flows and meeting lender requirements, all while capitalizing on potential opportunities for growth and value enhancement in their portfolios.

Investment Strategy & Risk Management

In the current real estate environment, market timing is crucial for identifying prime investment opportunities. As we navigate through 2026, the market has shown signs of stabilization with moderate appreciation in property values. However, investors must be astute, recognizing that the window for acquiring undervalued properties is narrowing. **Prime Property Funding** should focus on strategic acquisitions during seasonal lulls, such as mid-summer or late winter, where competition tends to decrease, allowing for more favorable pricing. Additionally, as interest rates exhibit modest fluctuations, timing acquisitions to coincide with periods of lower rates can enhance profitability.

Risk factors in the current landscape include economic uncertainty and potential interest rate hikes. To mitigate these risks, investors should employ a multi-faceted approach. Emphasizing **contingency planning** is essential, particularly in fix-and-flip operations, where holding costs can escalate due to unexpected market shifts or project delays. For buy-and-hold strategies, maintaining a robust **DSCR cushion** ensures that properties remain profitable even if rental growth slows.

Adjusting acquisition criteria and underwriting standards is vital in this environment. **Stress testing** assumptions against worst-case scenarios, such as a 15% decrease in property values or a 1% increase in interest rates, can safeguard against over-leveraging. Furthermore, diversifying portfolios by incorporating a mix of asset classes and geographic locations can reduce exposure to localized downturns, enhancing overall stability.

Key Considerations for Investors

- For fix-and-flip strategies, establish a maximum holding cost threshold of 5% of the property’s purchase price to prevent erosion of profits.

- Ensure a spread risk margin of at least 20% between purchase price and anticipated sale price to buffer against unexpected market corrections.

- Develop an exit timing plan, aiming to complete flips within six months to capitalize on current market conditions while minimizing risk.

- For buy-and-hold tactics, target a cap rate of no less than 6% to ensure sufficient return on investment, considering potential shifts in market dynamics.

- Incorporate a DSCR cushion of 1.25x to safeguard against fluctuations in rental income or unforeseen expenses.

- Ensure cash-on-cash returns exceed 8% annually to justify holding investments over the long term.

- In the context of bridge financing, secure interest rates below 8% to maintain profitability, especially during initial acquisition phases.

- Implement a draw schedule that aligns with project milestones, ensuring liquidity and minimizing idle capital.

- Prioritize markets with a history of consistent rent growth and employment stability, focusing on cities like Austin, Nashville, and Raleigh for optimal risk-adjusted returns.

- Adopt conservative underwriting by incorporating a 10% contingency reserve for unforeseen repair costs or market shifts.

- Enhance risk mitigation by ensuring robust reserves, comprehensive insurance coverage, and a focus on tenant quality and property condition to maintain asset value.

By incorporating these strategic insights and actionable recommendations, **Prime Property Funding** can navigate the current market with confidence, maximizing opportunities while effectively managing risk. This approach will empower investors to achieve sustainable growth and resilience in their real estate portfolios.

Resources

External References

Disclaimer: This market analysis is for informational purposes only and should not be considered financial or investment advice. Market conditions can change rapidly. Consult with a qualified financial or lending professional before making any decisions.