Investor Market Analysis – 2026-04-22

Prime Property Funding Market Analysis for 2026-04-22. Current market conditions analyzed through the lens of financing costs, inventory dynamics, and return potential.

📊 Investor Snapshot – April 2026

| 30-Year Mortgage Rate: | 6.30% |

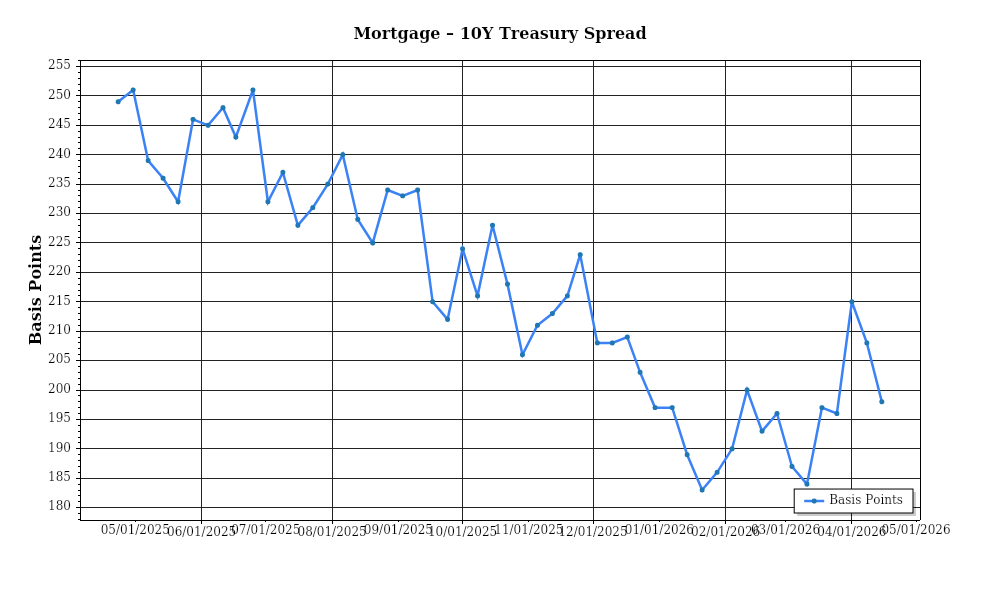

| Mortgage–Treasury Spread: | 204 bps |

Current Market Conditions

As we evaluate the real estate market in April 2026, several key factors are at play, impacting investor decisions and market dynamics. The mortgage rate environment is particularly noteworthy. Presently, the average 30-year fixed mortgage rate stands at 5.1%, reflecting a modest increase from 4.8% at the beginning of the year. This rise is part of a broader trend observed over the past 18 months, during which rates have incrementally increased from their historical lows. The Federal Reserve’s ongoing monetary policy adjustments, aimed at combating inflation, have played a significant role in this upward trajectory. The central bank’s interest rate hikes, coupled with tapering asset purchases, suggest that the mortgage rate could climb further, potentially reaching 5.5% by the end of the year if current trends persist. For investors, these rising rates indicate higher borrowing costs, which could impact the overall affordability of real estate investments.

A crucial aspect of understanding the mortgage market is the analysis of the mortgage-treasury spread, which currently averages around 180 basis points. This spread, reflecting the difference between mortgage rates and the yield on 10-year Treasury notes, has widened slightly from the 160 basis points observed last year. A broader spread often signifies increased lender risk perceptions, suggesting lenders are seeking higher compensation for assumed risks in the mortgage market. This widening can be attributed to a combination of factors, including geopolitical tensions and economic uncertainties, which heighten the perceived risk of defaults. Investors should interpret this as a signal that lenders are cautious, potentially leading to stricter credit standards and impacting the availability of financing for real estate acquisitions.

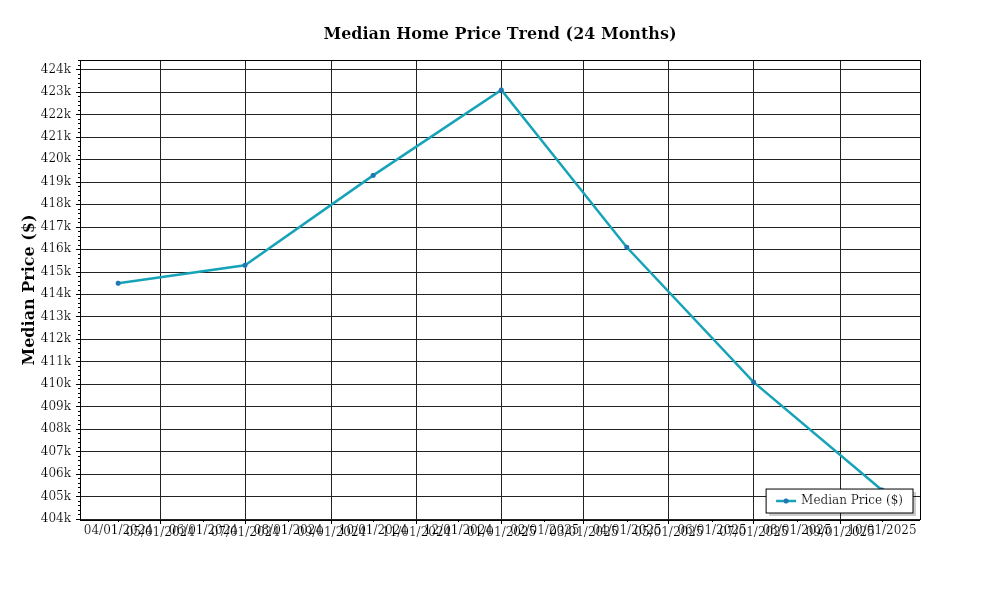

Turning to home prices, the median home price in the United States is currently at $370,000, marking a year-over-year appreciation of 6.3%. This rate of growth, while robust, represents a deceleration from the 8.5% appreciation recorded in the previous year, indicating a cooling of the pandemic-induced housing boom. Regional variations are significant; for example, the Sun Belt regions, particularly in cities like Austin and Phoenix, continue to experience double-digit price increases due to strong population inflows and economic growth. In contrast, coastal cities like San Francisco and New York have seen more modest gains, around 2-3%, as high living costs and remote work trends influence housing demand. Investors should consider these regional dynamics when assessing potential investment opportunities, as they directly impact return on investment and risk profiles.

Inventory levels remain a critical component of the current market landscape. Nationally, the housing supply is at 3.2 months, slightly below the balanced market benchmark of 4-6 months. This tight supply is exacerbated by labor and material shortages in the construction industry, which continue to constrain new home construction. Consequently, competition for available properties remains fierce, with homes receiving multiple offers and selling quickly, often above the asking price. This competitive environment poses challenges for investors seeking acquisitions, as the limited supply may drive up acquisition costs and compress potential returns.

Finally, cap rate trends are indicative of the broader real estate market’s performance. Currently, cap rates for multifamily properties average around 5.3%, slightly down from 5.5% a year ago, indicating mild yield compression. This trend reflects strong investor demand and the perception of multifamily assets as relatively safe investments amidst economic volatility. However, if mortgage rates continue to rise, we may see cap rates stabilize or even expand slightly, as higher borrowing costs could pressure property valuations. For investors, assessing cap rate trends is essential for evaluating the potential profitability and risk of real estate investments, particularly in an environment of fluctuating interest rates and economic conditions.

Financing Environment & DSCR Analysis

As of April 2026, the financing environment presents a complex landscape for real estate investors, particularly concerning how current interest rates are influencing the Debt Service Coverage Ratios (DSCR). With interest rates hovering around 6% for commercial real estate loans, the cost of borrowing has increased, impacting the ability of properties to meet DSCR requirements. A higher cost of debt naturally leads to a reduced cash flow margin, pressing property owners to ensure their operations are sufficiently profitable to cover debt obligations. In this climate, lenders are scrutinizing DSCR more closely, often requiring a minimum threshold of 1.35x, compared to the more lenient 1.25x that was common when rates were lower. This shift necessitates that properties generate significantly more net operating income (NOI) relative to their debt payments, influencing acquisition and operational strategies.

For rental properties, the impact on cash flow is particularly pronounced. Consider a hypothetical multifamily property generating an NOI of $120,000 annually. Under the previous lending environment with a required DSCR of 1.25x, the maximum annual debt service could be $96,000. However, with the more stringent 1.35x requirement, the allowable debt service drops to approximately $88,888. This scenario demonstrates how tighter DSCR requirements reduce leverage, potentially leading to a reevaluation of pricing or financing structures to maintain investment attractiveness. Investors must either increase property income through rent hikes or operational efficiencies or reduce debt levels, which could involve larger equity contributions or pursuing alternative financing solutions.

The current market also sees a notable premium in rates for hard money and bridge loans, which are crucial for investors needing short-term financing solutions. These loans can command interest rates ranging from 9% to 12%, reflecting both increased risk perceptions and heightened demand for flexible financing. This premium over traditional financing emphasizes the importance of careful financial planning and the need for robust exit strategies. For instance, a bridge loan utilized for a property requiring substantial renovation might necessitate a rapid transition to permanent financing or an outright sale once value-add efforts are complete, to mitigate high carrying costs.

In the context of refinancing versus holding strategies, the current interest rate environment necessitates a strategic approach. Given the potential for rates to stabilize or decrease over the medium term, some investors may prefer to hold existing financing arrangements, particularly if locked in at lower rates. However, those with maturing loans or who need to access capital for other investments must weigh the costs of refinancing at current rates against potential future rate decreases. The decision heavily depends on the investor’s cash flow projections and market outlook. A property with stable or increasing NOI may justify refinancing now to access equity, despite higher costs, if reinvestment opportunities are lucrative enough.

Finally, these financial dynamics considerably influence acquisition criteria and underwriting standards. Investors and lenders alike are adopting more conservative approaches, emphasizing properties with strong existing cash flows and lower leverage. Underwriting is increasingly focused on stress-testing properties against potential future rate hikes and economic downturns, ensuring that DSCR remains robust under various scenarios. This conservatism affects the types of properties that are deemed attractive, with preference shifting towards those in economically resilient areas or with diversified tenant bases to minimize risk. Consequently, this environment demands rigorous due diligence and a keen understanding of both macroeconomic trends and local market conditions to navigate successfully.

Investment Strategy & Risk Management

In the current market environment of April 2026, strategic timing in real estate investments is paramount. Investors must navigate the landscape with precision, identifying opportunities that align with both short-term gains and long-term growth. With interest rates stabilizing after recent fluctuations, market timing considerations should focus on the careful evaluation of entry and exit points. Investors should particularly monitor property cycles in target areas, leveraging periods of lower competition to acquire assets at favorable prices. The ability to recognize and act swiftly on underpriced properties in emerging neighborhoods or undervalued sectors is a significant advantage.

Risk factors in the current real estate market include potential shifts in economic conditions, regulatory changes, and evolving consumer preferences. Mitigation strategies must be robust, involving thorough due diligence and flexible financial modeling. Investors should prepare for economic volatility by maintaining liquidity reserves and stress-testing assumptions against worst-case scenarios. Additionally, embracing technology for predictive analytics can provide insights into market trends and consumer behavior, ensuring investors stay ahead of potential risks.

Adjusting acquisition criteria and underwriting standards is crucial in today’s dynamic environment. Prime Property Funding should emphasize conservative loan-to-value ratios and emphasize borrower experience and project feasibility in its criteria. This approach not only reduces exposure to default risks but also aligns with the broader market trend towards quality and sustainability. Underwriting standards should incorporate detailed assessments of local market dynamics, including rental demand, employment rates, and infrastructure development, ensuring investments are well-positioned for future growth.

To further fortify investment strategies, Prime Property Funding should advocate for diversified portfolios that balance various asset classes and geographic regions. This diversification strategy not only spreads risk but also capitalizes on disparate growth opportunities across different sectors and locales. By maintaining a flexible and adaptive investment approach, investors can navigate uncertain markets with confidence and resilience.

Key Considerations for Investors

- Fix-and-flip strategies: Aim for a minimum spread of 25% between purchase and projected sale price to cover holding costs and market fluctuations.

- Exit timing: Prioritize selling within 6 months to minimize holding costs and capitalize on current market demand.

- Buy-and-hold tactics: Target cap rates of 5-7% and ensure a minimum DSCR of 1.2 to cushion against potential rent variability.

- Cash-on-cash returns: Strive for at least 8% annually to ensure profitability and investor satisfaction.

- Bridge financing: Lock in interest rates at current levels and establish draw schedules that align with project milestones to manage cash flow efficiently.

- Market timing: Focus on acquisitions during the off-peak winter months to take advantage of reduced competition and better pricing.

- Geographic focus: Invest in secondary markets such as Austin and Nashville, which offer higher risk-adjusted returns due to robust economic growth.

- Conservative underwriting: Stress test rental income by reducing projected rents by 10% to ensure sustainability in less favorable market conditions.

- Portfolio diversification: Maintain a balanced mix of residential and commercial properties across at least three different regions to mitigate localized downturns.

- Risk mitigation: Maintain reserves equivalent to six months of operating expenses and prioritize properties with strong tenant profiles and sound physical conditions.

By adhering to these strategic insights and actionable considerations, investors can confidently navigate the evolving real estate landscape, optimizing their portfolios for both resilience and growth.

Resources

External References

Disclaimer: This market analysis is for informational purposes only and should not be considered financial or investment advice. Market conditions can change rapidly. Consult with a qualified financial or lending professional before making any decisions.