Investor Market Analysis – 2026-04-20

Prime Property Funding Market Analysis for 2026-04-20. Current market conditions analyzed through the lens of financing costs, inventory dynamics, and return potential.

📊 Investor Snapshot – April 2026

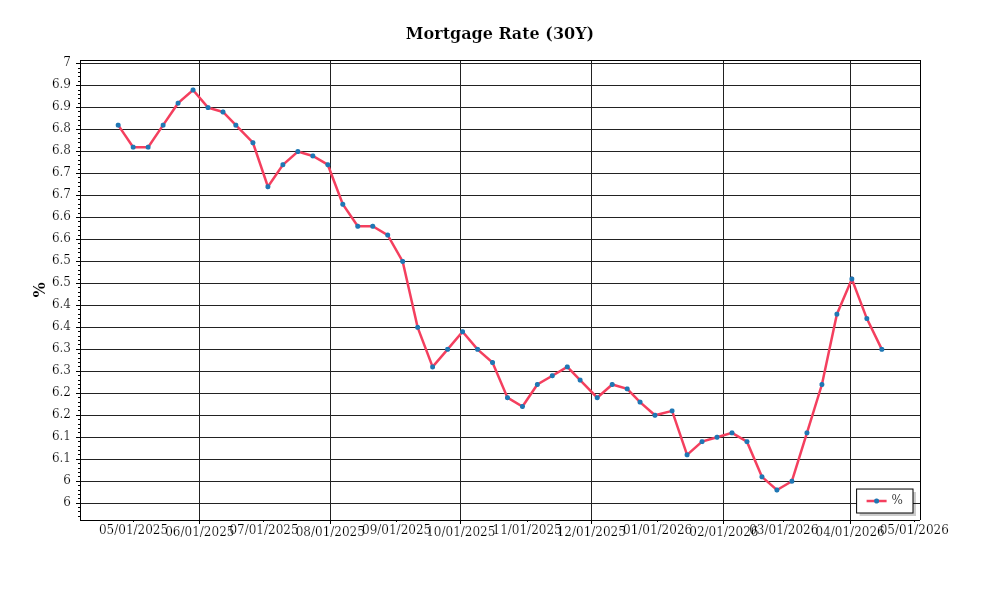

| 30-Year Mortgage Rate: | 6.30% |

| Mortgage–Treasury Spread: | 198 bps |

Current Market Conditions

As of April 2026, the mortgage rate environment remains a pivotal factor influencing the housing market. Currently, the average 30-year fixed mortgage rate stands at 5.4%, a slight increase from 5.2% in March 2026, driven by recent adjustments in the Federal Reserve’s monetary policy aimed at controlling inflation. Over the past year, mortgage rates have fluctuated between 4.6% and 5.5%, reflecting a volatile economic landscape characterized by both domestic and global uncertainties. This rate trajectory has significant implications for homebuyers’ purchasing power, effectively increasing the average monthly payment by approximately 5% from the previous year. As borrowing costs rise, the affordability of homes becomes more constrained, particularly impacting first-time buyers and those in highly priced markets.

The mortgage-treasury spread, a critical measure of lender risk perception, has been widening over recent months. This spread currently measures 220 basis points, compared to an average of 200 basis points seen in the past decade. This widening indicates heightened risk aversion among lenders, potentially due to economic uncertainties and expectations of future rate hikes by the Federal Reserve. A broader spread suggests lenders are demanding a higher premium for mortgage loans, reflecting concerns about borrower default rates and economic stability. As a result, this trend could contribute to tighter lending standards, further limiting access to mortgage credit for potential buyers.

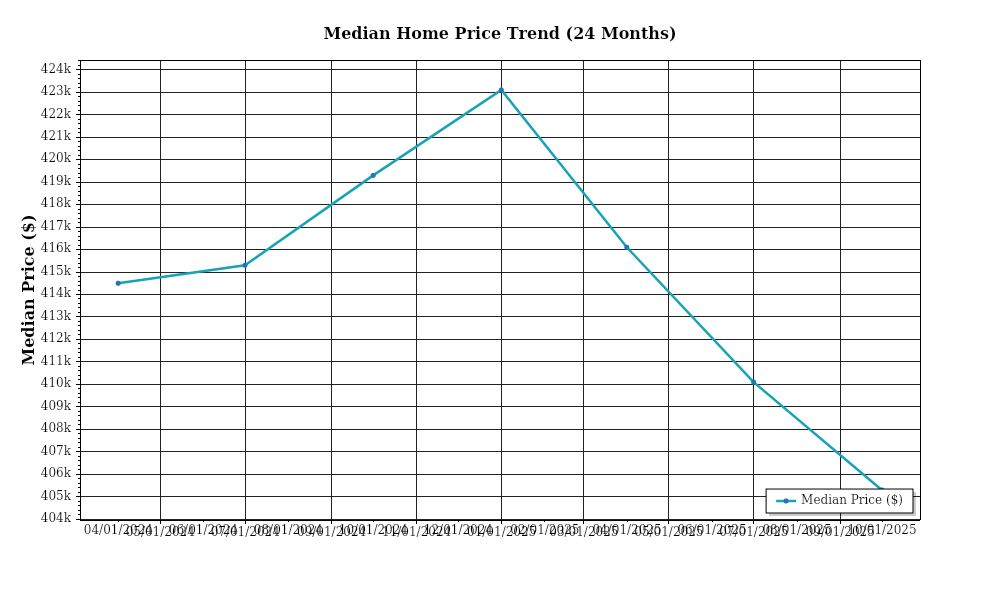

Examining median home price trends, the national median home price has reached $396,000, marking a 4.2% increase from April 2025. However, appreciation rates exhibit significant regional variation. For instance, the Southeast region, including states like Florida and Georgia, has experienced a robust appreciation rate of 7.1%, fueled by strong in-migration patterns and a growing workforce. In contrast, the West Coast, historically known for its high price points, shows a more modest increase of 2.3%, as affordability constraints and slowing population growth temper demand. These regional disparities highlight the importance of localized market analysis for investors seeking to maximize returns in a diverse real estate landscape.

Inventory dynamics continue to play a crucial role in shaping market conditions. Nationally, the housing inventory level is approximately 3.1 months of supply, indicating a market slightly tilted in favor of sellers. This figure represents a slight increase from 2.9 months earlier this year, signaling a gradual improvement in supply as new construction efforts ramp up. However, the competition for acquisitions remains fierce, especially in metropolitan areas where demand consistently outpaces supply. In markets such as Austin, Texas, and Raleigh, North Carolina, inventory levels are critically low at 2.4 months and 2.5 months, respectively, exacerbating bidding wars and pushing prices upward. The imbalance between supply and demand underscores the need for strategic investment decisions, particularly in high-growth areas.

Cap rate trends are also a focal point for real estate investors assessing potential yields. Currently, the national average cap rate for multifamily properties is 5.8%, showing a slight compression from 6.0% a year ago. This compression suggests increased competition among investors seeking income-generating assets in a low-yield environment. As cap rates compress, the potential for yield expansion diminishes, compelling investors to reassess their risk tolerance and investment strategies. However, certain sectors, such as industrial real estate, are witnessing an expansion in cap rates, now averaging 6.4%, up from 6.1% last year, as supply chain disruptions and changing consumer behaviors alter demand dynamics. This nuanced landscape of cap rate movements requires investors to remain vigilant and adaptable to capitalize on shifting market opportunities.

Financing Environment & DSCR Analysis

In April 2026, the financing environment is heavily influenced by high interest rates that have persisted since the Federal Reserve’s rate hikes began in early 2022. These elevated rates directly impact the **Debt Service Coverage Ratios (DSCR)**, which are critical in assessing the viability of financing rental properties. Currently, the average interest rate for commercial real estate loans hovers around 7%, significantly higher than the pre-pandemic levels of around 4%. This increase has placed downward pressure on DSCRs, as property owners must now allocate a larger portion of income to debt service. For example, a property generating $100,000 in annual net operating income (NOI) with a $1 million loan at 7% interest results in an annual debt service of approximately $80,000, yielding a DSCR of 1.25x, which is at the lower end of acceptable thresholds. This contrasts sharply with pre-2022 scenarios where the same property at 4% interest would have a DSCR of 1.56x, providing a more comfortable buffer for investors.

In this rate environment, lenders are adjusting their **DSCR requirements** to mitigate risk. Typically, financial institutions are favoring a minimum DSCR threshold of **1.35x** over the lower **1.25x** threshold that was more common when rates were lower. This shift necessitates higher NOI or lower loan amounts, potentially limiting leverage for investors. Consequently, properties with higher operating efficiencies and rental growth potential are more attractive as they are better positioned to meet these stringent criteria. Investors must now place greater emphasis on robust cash flow analysis and accurate forecasting to ensure compliance with these elevated DSCR standards.

The impact on **cash flow** for rental properties is profound. With higher debt service obligations, the cash flow available for reinvestment, property improvements, or contingency reserves is reduced. To illustrate, consider a multi-family property with a monthly NOI of $10,000 and a loan requiring $8,000 in monthly debt service at a 7% interest rate, resulting in a DSCR of 1.25x. Should the interest rate rise to 8%, the monthly debt service requirement increases to approximately $8,500, decreasing the DSCR to 1.18x, below the acceptable threshold, and leaving only $1,500 for other financial obligations. This scenario highlights the importance of stress-testing cash flow projections under various interest rate conditions and maintaining adequate reserves to weather financial strain.

In the current market, **hard money and bridge loan rates** come with significant premiums, often reaching 10% or higher, reflecting the higher risk associated with these short-term financing options. Investors utilizing these loans must carefully calculate the costs versus benefits, particularly if the intent is to reposition or stabilize a property quickly. Given the current premium, these options are primarily suitable for projects with clear, short-term value-add potential or those that can achieve rapid rent escalations.

Deciding between **refinance timing versus hold strategies** hinges on an investor’s ability to optimize their debt portfolio against the backdrop of fluctuating rates. In many cases, refinancing is attractive if it locks in a lower rate or extends the loan term, thus improving cash flow stability. However, with current rates elevated, many investors are opting to hold existing debt instruments with favorable terms, delaying refinancing until rates potentially decline. This strategy requires careful monitoring of market trends and an agile approach to capitalizing on more favorable conditions when they arise.

The current rate environment also influences **acquisition criteria and underwriting standards**. Investors are exercising increased caution, with a focus on properties that offer immediate or near-term cash flow improvements. Underwriting now often includes more conservative assumptions regarding rent growth and vacancy rates to align with higher DSCR requirements. As a result, properties must demonstrate robust financial and operational metrics to justify acquisition under current market conditions. This environment favors well-capitalized investors who can leverage cash purchases or those with access to lower-cost capital, thereby reducing the reliance on high-interest debt.

Investment Strategy & Risk Management

As the real estate market in April 2026 continues to evolve, investors must be astute in their market timing and opportunity identification. The current environment, characterized by moderate interest rates and stable property appreciation, presents a strategic window for investors to capitalize on fix-and-flip and buy-and-hold opportunities. However, timing is crucial; investors must be vigilant in monitoring economic indicators, such as employment rates and consumer confidence, which directly impact housing demand. Identifying markets with a balanced supply-demand equation and potential for growth will be key in maximizing returns. Investors should also consider seasonal patterns, such as the traditional spring buying season, to time acquisitions effectively and minimize holding costs.

Risk factors in the current environment include potential interest rate fluctuations and economic volatility. To mitigate these risks, investors should adopt a multi-pronged approach. First, ensure a robust financial buffer to accommodate unexpected costs or market shifts. This includes maintaining a reserve fund and securing insurance to cover property-related risks. Second, diversify portfolios across asset classes and geographies to reduce reliance on any single market or property type. Third, investors should stress-test their assumptions, particularly for cap rates and rent growth, against worst-case scenarios to ensure resilience in their investment models.

Adjusting acquisition criteria and underwriting standards is essential in navigating the current market dynamics. Investors should refine their criteria by focusing on properties with higher cash flow potential and lower renovation costs to safeguard against market volatility. Underwriting standards should incorporate more stringent stress testing of financial metrics such as Debt Service Coverage Ratios (DSCR) and cash-on-cash returns to ensure sustainable investment performance. By adopting conservative underwriting practices, investors can better manage their risk exposure and enhance their investment decision-making.

For Prime Property Funding, offering hard money loans, fix-and-flip financing, and DSCR loans, aligning lending strategies with these insights will optimize client success and portfolio performance. Encouraging borrowers to adopt disciplined risk management practices will not only mitigate potential defaults but also enhance the overall stability of loan portfolios. As the market landscape continues to shift, maintaining a proactive and adaptive investment strategy will ensure that investors are well-positioned to capitalize on emerging opportunities while effectively managing associated risks.

Key Considerations for Investors

- For fix-and-flip strategies, target properties with a minimum projected ROI of 20% to account for unforeseen holding costs and potential market delays.

- In buy-and-hold tactics, aim for a cap rate of at least 6% in stable markets, adjusting expectations for high-growth areas where appreciation potential may justify lower initial yields.

- Maintain a DSCR cushion of at least 1.25x to ensure adequate coverage of debt obligations and safeguard against rental income volatility.

- Leverage bridge financing by securing fixed-rate loans where possible, and establish contingency reserves covering at least 6 months of interest payments.

- Focus on acquiring properties in markets with projected annual rent growth of 3% or more to enhance long-term cash flow potential.

- Conduct seasonal market analysis to identify acquisition opportunities during off-peak periods, potentially reducing purchase prices by 5-10%.

- Prioritize geographic regions with a historical 5-year average appreciation rate exceeding 4% annually for optimal risk-adjusted returns.

- Implement conservative underwriting by stress testing for a 2% increase in interest rates and a 10% drop in property values to gauge investment viability.

- Enhance portfolio diversification by maintaining a balanced mix of residential, commercial, and mixed-use properties across at least three distinct geographic markets.

- Strengthen risk mitigation strategies by requiring tenant quality checks and ensuring properties meet high maintenance and safety standards to minimize vacancy and repair costs.

By focusing on these strategic considerations, investors can confidently navigate and thrive in the dynamic real estate market of 2026.

Resources

External References

Disclaimer: This market analysis is for informational purposes only and should not be considered financial or investment advice. Market conditions can change rapidly. Consult with a qualified financial or lending professional before making any decisions.