Investor Market Analysis – 2026-04-18

Prime Property Funding Market Analysis for 2026-04-18. Current market conditions analyzed through the lens of financing costs, inventory dynamics, and return potential.

📊 Investor Snapshot – April 2026

| 30-Year Mortgage Rate: | 6.30% |

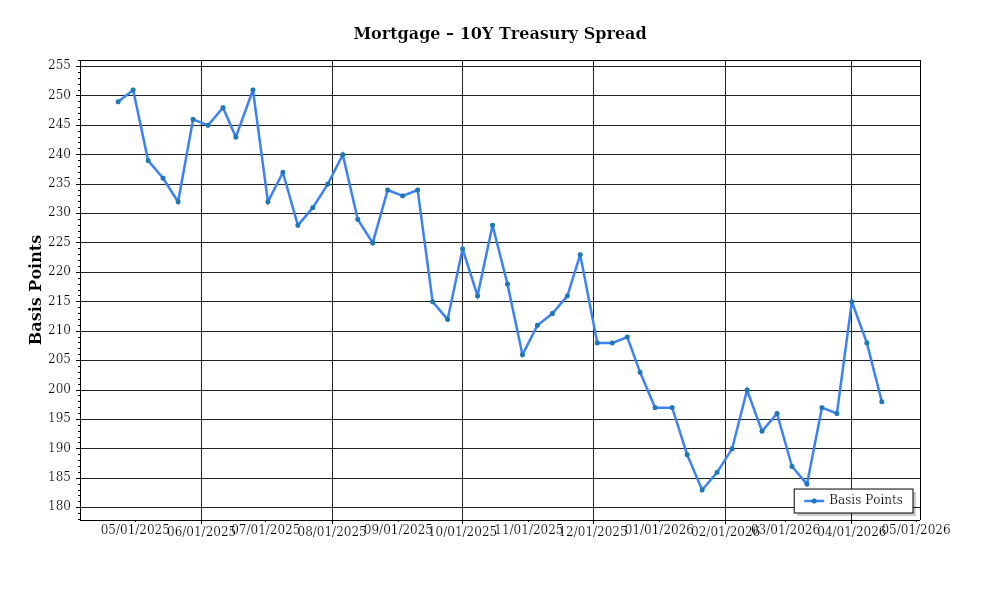

| Mortgage–Treasury Spread: | 198 bps |

Current Market Conditions

As of April 2026, the mortgage rate environment is characterized by persistently elevated levels, with the average 30-year fixed mortgage rate hovering around 6.8%. This represents a modest increase from 6.5% in October 2023, reflecting a gradual upward trajectory over the past two and a half years. The Federal Reserve’s cautious approach to monetary policy, coupled with inflation rates stabilizing around 3.5%, has contributed to this trend. Short-term mortgage options, such as the 15-year fixed rate, are averaging approximately 6.1%, indicating a narrowed gap between short-term and long-term borrowing costs. The sustained high rates are directly influencing buyer affordability, limiting access for first-time buyers, and leading to a more competitive rental market as potential homeowners delay purchases.

The mortgage-treasury spread, a critical indicator of lender risk perception, currently stands at approximately 180 basis points over the 10-year Treasury yield, which is about 3.2%. This spread has widened from 160 basis points noted in late 2023, signaling increased caution among lenders and a perception of heightened risk in the housing market. Typically, a wider spread indicates that lenders are compensating for perceived risks associated with economic uncertainty or potential borrower defaults. The increased spread suggests that while demand for mortgages remains robust, lenders are wary of potential market volatility and the possibility of economic downturns impacting borrower solvency.

Nationally, the median home price has risen to approximately $430,000, up from $380,000 in October 2023, marking an appreciation rate of around 13.2% over this period. This robust growth in home prices is primarily driven by limited supply and continued high demand, especially in urban and suburban areas where economic opportunities are abundant. Regionally, price appreciation varies significantly. The South and West regions of the United States have experienced higher than average appreciation rates, with cities like Austin and Phoenix seeing increases of over 15%. Conversely, the Midwest and Northeast have observed more modest gains, with some areas appreciating by less than 10%. These regional disparities highlight the importance of localized market dynamics and economic factors influencing home values.

Inventory dynamics reveal a persistent imbalance between supply and demand, exacerbating competition for acquisitions. As of April 2026, housing inventory is at a critically low level, with active listings down by 20% compared to pre-pandemic levels. The average time on the market for new listings has dropped to just 30 days, underscoring the fierce competition among buyers. This scarcity is further intensified by the “lock-in effect,” where existing homeowners are reluctant to sell and lose their lower mortgage rates, opting instead to renovate or expand their current homes. This dynamic contributes to sustained upward pressure on prices and limits opportunities for new market entrants.

Cap rate trends, a vital measure of real estate investment attractiveness, are currently showing signs of yield compression. Nationwide, average cap rates for multifamily properties have compressed to around 4.5%, down from 5.2% in late 2023. This compression is indicative of strong investor demand and confidence in rental income streams, despite higher borrowing costs. However, the lower cap rates signal increased competition among investors, potentially leading to lower future returns on investment. In contrast, retail and office properties are experiencing more modest compression, with cap rates around 5.8% and 6.5%, respectively. This divergence highlights the relative stability and growth prospects in multifamily investments compared to other sectors facing challenges related to the changing landscape of work and retail consumption.

These current market conditions underscore a complex environment for real estate investors, characterized by elevated mortgage rates, a cautious lending landscape, significant regional disparities in home price appreciation, and competitive acquisition scenarios due to limited inventory and yield compression across key property sectors.

Financing Environment & DSCR Analysis

The financing environment in April 2026 presents a nuanced landscape for real estate investors, with current interest rates playing a pivotal role in shaping debt service coverage ratios (DSCR). Interest rates have stabilized at a level slightly above historical norms, exerting upward pressure on borrowing costs. This environment has significant implications for DSCR calculations, which represent the ratio of a property’s annual net operating income (NOI) to its annual debt service. A higher interest rate increases the debt service component, thus lowering the DSCR if NOI remains constant. For instance, if a property generates an NOI of $120,000 and the annual debt service is $100,000 at a lower rate, the DSCR is 1.20x. However, with increased rates pushing the debt service to $110,000, the DSCR drops to 1.09x, indicating a tighter margin for error and potentially more challenging loan approvals.

In this environment, lenders are particularly attuned to DSCR requirements, often adhering to thresholds of 1.25x to 1.35x. These benchmarks offer a buffer to absorb interest rate fluctuations and other financial uncertainties. A DSCR of 1.25x implies that the NOI is 25% higher than the debt obligations, providing some cushion for variability in rental income or unexpected expenses. Meanwhile, a threshold of 1.35x is increasingly common as lenders strive to mitigate risk. This heightened requirement can restrict borrowing capability, compelling investors to enhance property management efficiency or seek properties with higher NOI potential to meet these criteria.

Cash flow implications for rental properties are profound in this context. Consider a multi-family property generating a monthly NOI of $10,000. With a DSCR requirement of 1.35x, the maximum allowable debt service is approximately $7,407 per month. If current interest rates necessitate a monthly debt service of $8,000, the deal becomes infeasible without adjusting rental income or reducing acquisition costs. Investors might need to explore rent increases or operational improvements to achieve the desired DSCR, thus impacting the property’s attractiveness and financial viability.

Moreover, the current market has seen a notable increase in hard money and bridge loan rate premiums. These short-term financing options, typically characterized by higher interest rates and fees, are now even costlier due to risk-adjusted pricing models. For example, a hard money loan that might have commanded a 10% interest rate in a more favorable environment could now be priced at 12-14%. This shift necessitates careful consideration of the cost-benefit balance when pursuing these financing avenues, especially for renovation or quick-turnaround projects.

The decision to refinance or hold properties in this interest rate climate hinges on strategic timing and financial objectives. With rates expected to stabilize or even decline slightly in the medium term, some investors might opt to hold existing loans with favorable terms, delaying refinancing until conditions improve. Conversely, those with adjustable-rate mortgages might seek immediate refinancing to lock in fixed rates, despite the current premium, to mitigate future rate volatility.

Finally, the financing environment impacts acquisition criteria and underwriting standards. Lenders are increasingly stringent, emphasizing robust DSCR metrics and requiring comprehensive financial documentation. This shift influences investors to prioritize properties with strong cash flow potential and stable tenant bases. Furthermore, conservative underwriting standards necessitate thorough market analysis and due diligence to ensure that projected cash flows can comfortably surpass debt service obligations. Investors must adapt their acquisition strategies, focusing on properties that can withstand financial scrutiny and meet elevated DSCR benchmarks, thus ensuring sustainable investment performance in the current economic climate.

Investment Strategy & Risk Management

In the current real estate market, strategic timing and opportunity identification are crucial for optimizing investment returns. As of April 2026, the market exhibits signs of stabilization following fluctuating interest rates and changing economic conditions. This creates a fertile ground for investors who can accurately gauge market cycles and strategically time their acquisitions. Investors should focus on areas with pent-up demand and undervalued properties poised for appreciation. Timing is particularly critical in the fix-and-flip segment, where holding costs can rapidly erode profits if the market cools unexpectedly. Engaging in thorough market analysis and leveraging data analytics can help identify prime acquisition windows and mitigate timing risks.

Risk factors in today’s environment primarily stem from economic volatility, interest rate fluctuations, and potential regulatory changes. Mitigation strategies include diversifying across asset classes and geographies to spread risk, maintaining a robust cash reserve for unforeseen expenses, and implementing flexible exit strategies. For example, investors can hedge against market downturns by securing fixed-rate financing and using insurance products to protect against property-specific risks. Adjusting acquisition criteria to focus on properties with higher demand resilience and conducting stress tests on financial models can further cushion against adverse market movements.

Adjusting acquisition criteria and underwriting standards is essential in this evolving landscape. Investors should tighten their criteria by focusing on properties with strong fundamentals, such as high demand areas with solid employment growth and infrastructure development. Underwriting standards should incorporate conservative assumptions about rent growth and vacancy rates. Emphasizing properties that meet stringent debt service coverage ratio (DSCR) thresholds can help ensure investments remain viable under various economic conditions. Additionally, revising cap rate targets to reflect current market realities and maintaining a keen eye on cash-on-cash returns will help align investment decisions with risk-adjusted returns.

In summary, the current real estate market poses both challenges and opportunities. Investors prepared to adapt their strategies through rigorous analysis and sound risk management will be well-positioned to capitalize on emerging opportunities. By focusing on strategic market entry, prudent risk management, and disciplined underwriting, investors can navigate this dynamic environment with confidence.

**Key Considerations for Investors**

- Fix-and-flip strategies: Maintain holding costs below 20% of total project budget to ensure profitability. Implement contingency plans to address potential delays or market shifts.

- Buy-and-hold tactics: Target cap rates of at least 5% in high-demand urban areas to ensure attractive returns. Assume conservative rent growth of 2-3% annually to buffer against economic shifts.

- Bridge financing: Lock in interest rates at or below current market averages (approximately 7%) to manage financing costs. Establish clear draw schedules to optimize cash flow management.

- Market timing: Prioritize acquisitions during seasonal slowdowns, which may offer better pricing opportunities. Assess holding costs against potential appreciation to determine optimal entry points.

- Geographic focus: Invest in markets with robust job growth and population increases, such as the Sun Belt region, for superior risk-adjusted returns.

- Conservative underwriting: Stress test cash flow models by simulating vacancy rates of 10% and rent declines of 5% to ensure resilience under adverse conditions.

- Portfolio diversification: Balance asset classes to include residential, commercial, and mixed-use properties, and spread investments across at least three geographic regions.

- Risk mitigation: Maintain reserves equivalent to six months of operating expenses and prioritize properties with good tenant quality and condition to minimize maintenance risks.

By adopting these strategies, investors can effectively navigate the complexities of the 2026 real estate market, minimizing risks while maximizing opportunities for growth and profitability.

Resources

External References

Disclaimer: This market analysis is for informational purposes only and should not be considered financial or investment advice. Market conditions can change rapidly. Consult with a qualified financial or lending professional before making any decisions.