Investor Market Analysis – 2026-04-14

Prime Property Funding Market Analysis for 2026-04-14. Current market conditions analyzed through the lens of financing costs, inventory dynamics, and return potential.

📊 Investor Snapshot – April 2026

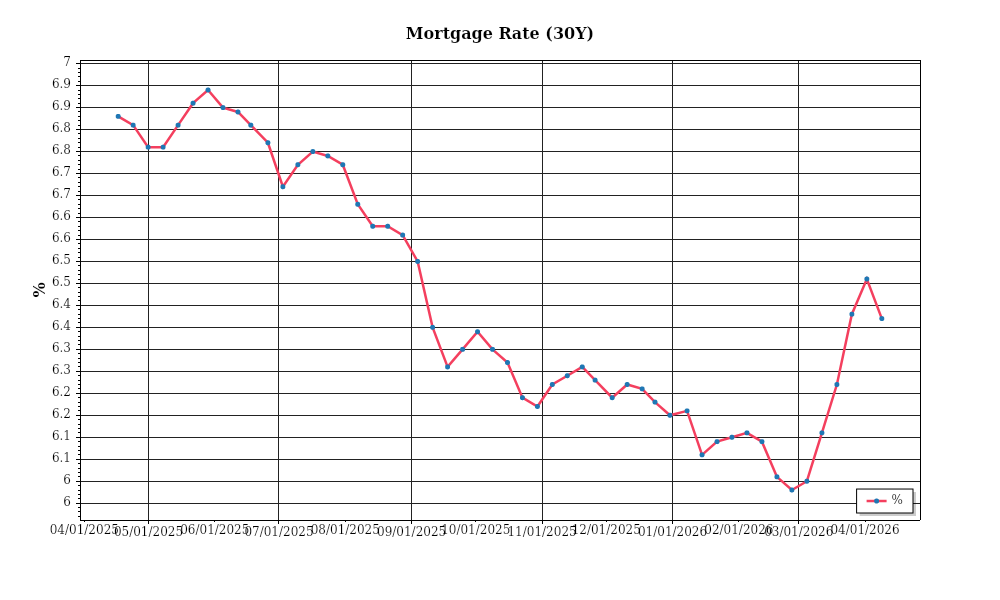

| 30-Year Mortgage Rate: | 6.37% |

| Mortgage–Treasury Spread: | 206 bps |

Current Market Conditions

As of April 2026, the mortgage rate environment is characterized by moderate stability following a period of volatility in late 2025. The average 30-year fixed mortgage rate currently stands at 5.65%, a slight decrease from the 5.75% observed in March 2026. This stabilization comes after a peak of 6.10% in December 2025, indicating a gradual easing in monetary policy and a response to recent Federal Reserve signals of interest rate normalization. Over the past six months, mortgage rates demonstrate a downward trajectory, reflecting improved economic confidence and reduced inflationary pressures. However, the potential for rate increases remains, contingent on upcoming economic data and Federal Reserve actions. The current rates are still above the pre-pandemic levels of approximately 3.75%, suggesting a more cautious lending environment.

The mortgage-treasury spread, an indicator of lender risk perception, is currently at 1.75%, which is slightly elevated compared to the historical average of 1.50%. This spread has narrowed from a high of 2.10% in the third quarter of 2025, indicating a reduced risk premium demanded by lenders. The narrowing spread suggests increased lender confidence in borrower creditworthiness and a stable economic outlook. However, the spread remains above pre-pandemic levels, indicating that lenders are still pricing in some level of uncertainty, particularly related to geopolitical tensions and potential economic disruptions. This spread is a critical indicator for investors, as it affects borrowing costs and, consequently, housing demand and pricing.

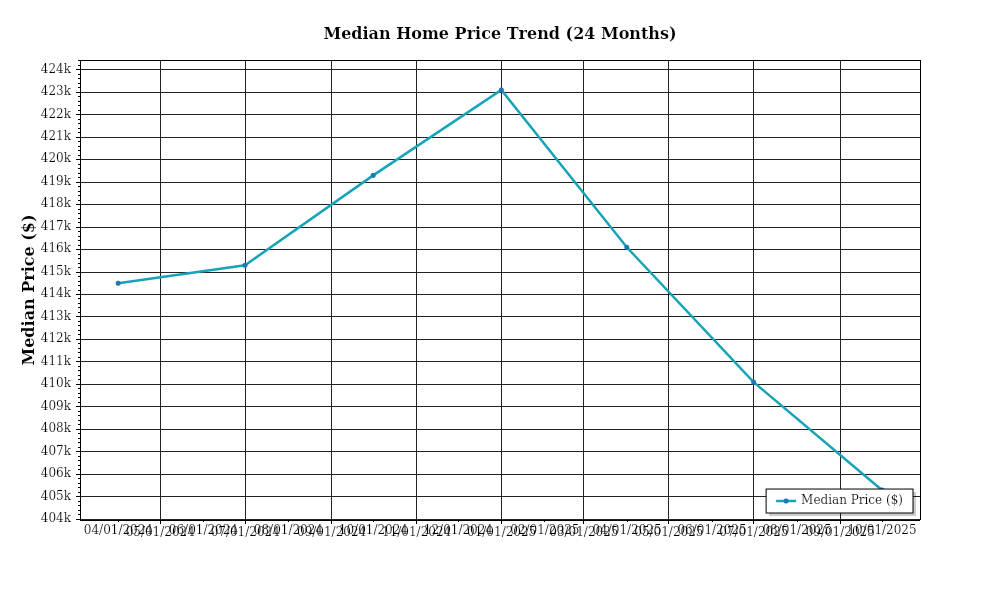

The median home price across the United States has seen a robust appreciation, currently at $410,000, up from $395,000 in April 2025. This represents an annual appreciation rate of approximately 3.8%, which marks a slowdown from the double-digit growth rates of the previous two years. Regionally, the South and West continue to lead in price growth, with cities like Austin and Phoenix experiencing increases of 5.2% and 4.7% respectively. Conversely, the Midwest and Northeast exhibit more modest growth, with cities like Cleveland and Boston showing appreciation rates of 2.5% and 2.8%. These regional variations highlight differing economic conditions and demand pressures, with the South and West benefiting from demographic shifts and robust job markets.

Inventory dynamics reveal a market in transition. The current national inventory level is approximately 1.3 million units, reflecting a 5% increase from last year. This rise in inventory indicates a shift towards a more balanced market, as supply begins to catch up with demand. The months’ supply of homes sits at 3.8 months, up from 3.2 months in April 2025, signaling an easing of the intense competition that characterized the market in 2024 and early 2025. Despite this increase, inventory levels remain below the six-month benchmark often associated with a balanced market, suggesting that while conditions are improving, buyers still face competitive pressures in many areas.

Cap rate trends in the real estate market provide additional insights into investment conditions. Currently, the average cap rate for commercial real estate is at 5.2%, showing a slight compression from 5.4% in April 2025. This compression indicates a high demand for real estate investments, as investors are willing to accept lower yields in anticipation of continued property appreciation and rental income growth. However, certain sectors, such as office space, are experiencing yield expansion due to shifts in work-from-home trends and reduced demand. For residential and industrial properties, yield compression continues, driven by strong rental demand and limited supply. These cap rate dynamics are crucial for investors assessing potential returns and risks in the current market environment.

Financing Environment & DSCR Analysis

As of April 2026, the financing environment continues to pose challenges and opportunities for real estate investors, primarily driven by interest rate fluctuations and stringent lending requirements. The current interest rate environment affects the Debt Service Coverage Ratios (DSCR), a critical metric for real estate investors assessing property viability and lender risk. Higher interest rates, which have seen a steady increase over the past two years, directly impact the DSCR. A higher interest rate increases the debt service cost, thereby reducing the DSCR unless rental income increases proportionately. For instance, if a rental property has a monthly income of $10,000 and the debt service is $7,500, the DSCR is 1.33x. An increase in interest rates that raises the debt service to $8,500 would lower the DSCR to 1.18x, which might not meet many lenders’ minimum requirements.

In today’s market, lenders typically require a DSCR of at least 1.25x to 1.35x. This range provides a cushion to ensure that rental income sufficiently covers debt obligations, accounting for potential income fluctuations or operating cost increases. The 1.25x threshold is often the minimum acceptable for conventional loans, but many lenders prefer the security of a 1.35x DSCR, especially in a volatile rate environment. This higher threshold ensures greater protection against interest rate hikes and potential vacancies or maintenance issues that may reduce net operating income. Investors must carefully evaluate their properties’ potential to meet these DSCR requirements amid rising rates.

The implications for cash flow in rental properties are significant. Suppose an investor owns a multi-family property generating $250,000 annually in gross rental income with operating expenses of $75,000. Initially, with a debt service of $100,000, the DSCR stands at 1.75x. If refinancing increases the debt service to $120,000, the DSCR drops to 1.46x. While still above the minimum threshold, the cushion is reduced, meaning less margin for error in rental income fluctuations or unexpected expenses. Investors must thus analyze potential scenarios where rental demand might dip or interest rates further increase, affecting their cash flow and financial stability.

Hard money and bridge loans, often used for short-term financing, command a premium over traditional financing, reflecting the higher risk and shorter duration. Currently, these loans have rates ranging from 8% to 12%, compared to conventional mortgage rates averaging around 6%. This premium can significantly impact short-term cash flow and DSCR calculations, as the increased cost of borrowing must be offset by either higher rental income or a quicker turnaround on property improvements and sales. Investors utilizing these financing options need a robust exit strategy to mitigate the higher interest burden, such as selling the property promptly or refinancing into a lower-rate loan once the holding period is completed.

The current rate environment necessitates a strategic approach to refinancing versus holding properties. With rates expected to stabilize but remain elevated in the short term, investors must weigh the benefits of locking in current rates against potential future rate declines. Holding strategies might favor properties with strong, stable cash flow and healthy DSCRs, while refinancing might be advantageous for properties with lower current rates that could benefit from restructuring to improve cash flow or release equity.

This environment influences acquisition criteria and underwriting standards as well. Investors are increasingly focused on properties with higher potential DSCRs and resilient rental income streams. Underwriting standards have tightened, placing greater emphasis on detailed cash flow projections and stress-testing against rate increases. Properties that offer opportunities for rent increases or operational efficiencies are particularly attractive, allowing investors to maintain or improve DSCRs despite rising debt service costs. This strategic focus on DSCR and cash flow management is essential for navigating the current financing landscape and ensuring long-term investment viability.

Investment Strategy & Risk Management

In the current real estate market landscape, strategic timing and opportunity identification are critical for investors seeking to optimize returns. As of April 2026, the market exhibits signs of stabilization after periods of volatility, making it crucial for investors to remain vigilant and agile. Recognizing the cyclical nature of real estate, savvy investors should focus on markets demonstrating signs of recovery and growth. This involves leveraging data analytics to predict market trends, identifying underpriced assets, and capitalizing on shifts in demand driven by macroeconomic conditions, such as changes in interest rates or demographic shifts.

Given the evolving market dynamics, understanding and mitigating risk factors is essential. Key risks include interest rate volatility, potential regulatory changes, and regional economic fluctuations. To navigate these, investors should employ a diversified portfolio strategy that spreads investments across different asset classes and geographies. Additionally, maintaining a strong liquidity position and securing flexible financing options can buffer against unexpected downturns. For Prime Property Funding, this means offering adaptable loan products that cater to the diverse needs of real estate investors, such as fix-and-flip financing with built-in contingencies and DSCR loans with adjustable terms.

Adjusting acquisition criteria and underwriting standards is a crucial step in aligning investment strategies with current market conditions. Investors should refine their criteria to focus on properties that meet stringent cash flow and profitability thresholds. This involves stress testing assumptions to account for potential rent stagnation or increases in holding costs. Underwriting should incorporate conservative assumptions about rent growth and expense ratios, ensuring that properties maintain a healthy cash flow under less favorable scenarios. For fix-and-flip projects, a meticulous assessment of renovation costs and timelines is fundamental to minimizing financial exposure and maximizing return on investment.

Ultimately, a comprehensive investment strategy that emphasizes informed decision-making, robust risk management, and adaptable criteria will empower investors to thrive in the current market. By aligning strategies with market realities and leveraging Prime Property Funding’s tailored financing solutions, investors can confidently navigate the complexities of the real estate landscape.

Key Considerations for Investors

- For fix-and-flip strategies, ensure holding costs do not exceed 2% of the project’s total budget to maintain profitability.

- Target a minimum spread risk of 25% between purchase price and after-repair value (ARV) to safeguard against market fluctuations.

- Implement an exit timing strategy with a maximum holding period of 90 days post-renovation to reduce exposure to market changes.

- Set cap rate targets for buy-and-hold investments at 6% or higher to ensure adequate returns in less volatile markets.

- Incorporate a DSCR cushion of at least 1.25 to absorb potential fluctuations in rental income and interest rates.

- Negotiate bridge financing with interest rates capped at 8% and ensure contingency reserves equal to 10% of the loan amount.

- Prioritize acquisition in markets with seasonal patterns that show higher transaction volumes in Q2 and Q3 to capitalize on demand.

- Focus on geographic regions with projected population growth rates above 3% annually for best risk-adjusted returns.

- Adopt conservative underwriting by stress testing property performance under scenarios with 10% lower rent growth than forecasted.

- Enhance portfolio diversification by balancing investments across at least three different asset classes and geographies.

Empowered by these strategies, investors can confidently engage the market, leveraging both cautious and opportunistic approaches to achieve robust, sustainable growth.

Resources

External References

Disclaimer: This market analysis is for informational purposes only and should not be considered financial or investment advice. Market conditions can change rapidly. Consult with a qualified financial or lending professional before making any decisions.