Investor Market Analysis – 2026-04-12

Prime Property Funding Market Analysis for 2026-04-12. Current market conditions analyzed through the lens of financing costs, inventory dynamics, and return potential.

📊 Investor Snapshot – April 2026

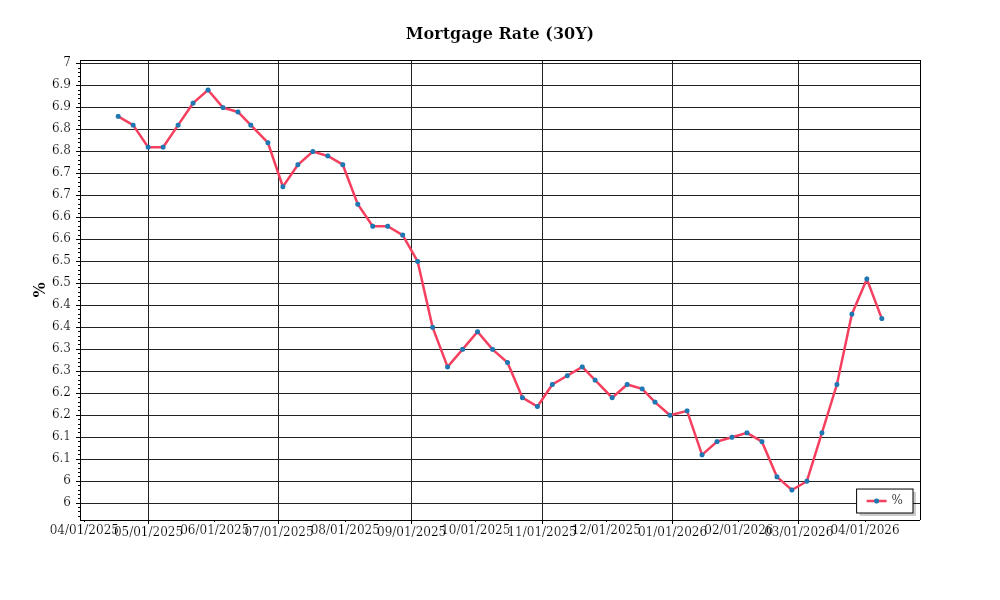

| 30-Year Mortgage Rate: | 6.37% |

| Mortgage–Treasury Spread: | 208 bps |

Current Market Conditions

As of April 2026, the mortgage rate environment remains a critical factor influencing the real estate market. Mortgage rates currently average around 6.1% for a 30-year fixed-rate mortgage, reflecting a slight increase from the 5.8% average recorded in December 2025. This upward trajectory is consistent with the Federal Reserve’s ongoing efforts to control inflation, which saw a series of rate hikes through late 2025 and early 2026. Analysts project that mortgage rates could stabilize by late 2026, but there is significant uncertainty due to potential economic volatility and geopolitical tensions. The current rate environment places upward pressure on monthly mortgage payments, potentially dampening demand among first-time buyers and those looking to refinance existing loans.

The mortgage-treasury spread, a critical indicator of lender risk perception, is currently at 170 basis points—a slight increase from the 165 basis points observed in January 2026. This spread, which represents the difference between mortgage rates and the yield on 10-year U.S. Treasury notes, provides insight into the risk premium lenders require to compensate for potential borrower defaults. The widening of this spread suggests that lenders are cautiously assessing the economic landscape and are pricing in higher risk. This adjustment reflects broader concerns about economic stability and potential shifts in borrower creditworthiness, which might lead to tighter lending standards and impact the availability of credit for potential homebuyers.

Examining median home price trends, the national median home price stands at approximately $410,000, marking a 3.5% increase year-over-year. However, this rate of appreciation has decelerated compared to the 6.2% increase observed during the same period last year, indicating a cooling market. Regional variations remain pronounced; for instance, the Sun Belt states, such as Arizona and Texas, are experiencing above-average appreciation rates of around 5.8%, driven by continued population growth and economic expansion. In contrast, coastal markets like California and New York are seeing more moderate increases of about 2.3%, as affordability concerns and high living costs begin to temper demand.

Inventory dynamics continue to play a pivotal role in shaping the real estate landscape. Nationally, the total housing inventory stands at approximately 1.2 million units, representing a 3.1-month supply at the current sales pace. This is a slight improvement from the 2.9-month supply recorded six months prior, yet it remains well below the 6-month benchmark typically associated with a balanced market. The constrained supply, paired with steady demand, sustains a competitive environment for acquisitions. Bidding wars, although less frequent than during the peak pandemic years, still occur in high-demand areas, particularly for properties at or below the median price point.

Lastly, cap rate trends reveal important insights into investment dynamics and yield expectations. The average cap rate for commercial real estate is currently at 6.2%, reflecting a 30 basis point increase from late 2025. This shift indicates a trend toward yield expansion, as rising interest rates put upward pressure on capitalization rates. Investors are recalibrating their expectations in response to the higher cost of capital, leading to a more cautious approach to acquisitions. Despite these pressures, certain sectors like industrial real estate continue to show resilience, maintaining cap rates around 5.8% due to robust demand for logistics and distribution facilities.

In summary, the current real estate market is navigating a complex interplay of rising mortgage rates, cautious lender sentiment, regional price variations, tight inventory conditions, and evolving cap rate trends. These factors collectively shape the strategic considerations for investors as they assess opportunities and risks in 2026.

Financing Environment & DSCR Analysis

The current interest rate environment as of April 2026 plays a pivotal role in shaping the debt service coverage ratios (DSCR) for real estate investments. With average interest rates hovering around 5.75% for standard 30-year fixed commercial mortgages, investors are experiencing significant effects on their DSCR calculations. A higher interest rate increases the monthly debt obligations, thus reducing the net operating income (NOI) coverage over debt service. For instance, a property generating $120,000 in NOI with a monthly debt payment of $8,000 would have a DSCR of 1.25x. However, if the interest rate increases, leading to a $9,000 monthly payment, the DSCR drops to 1.11x, potentially disqualifying it from financing under typical lending standards.

In this environment, lenders are generally requiring a minimum DSCR of 1.25x for stabilized properties, while more conservative institutions are setting the bar higher at 1.35x. This means that for every dollar of debt service, the property must generate at least $1.25 to $1.35 in NOI. These thresholds ensure a buffer against potential income fluctuations or unexpected expenses, maintaining the lender’s risk at a manageable level. However, this also signifies that potential acquisitions must demonstrate robust income streams or be acquired at a discount to meet these stringent requirements. As a result, properties with previously acceptable cash flows may now fall short under new loan conditions.

The implications of these requirements on cash flow for rental properties are profound. For instance, consider a multifamily property with a purchase price of $1.5 million and an annual NOI of $180,000. Under a 5.75% interest scenario, the annual debt service on an 80% LTV loan is approximately $105,000. The resulting DSCR is 1.71x, comfortably above the 1.35x threshold. However, should the interest rate rise to 6.5%, the debt service increases to $111,000, reducing the DSCR to 1.62x. While still above lender requirements, the reduced margin may affect investor decisions on refinancing or holding, as cash flow tightens and reserves become crucial for sustainability.

Hard money and bridge loans, often employed for short-term financing needs or value-add projects, currently carry rate premiums of around 8% to 10%. These higher rates reflect the increased risk and shorter loan durations involved. The premium impact is substantial—consider a $500,000 bridge loan at 10% interest; the annual cost is $50,000, which substantially eats into the cash flow, requiring properties to generate higher returns to justify the investment. Investors must weigh the cost of such financing against potential property appreciation or increased rental rates to ensure profitability.

Regarding refinance timing and hold strategies, the current rate environment suggests a cautious approach. With the uncertainty of future rate hikes or cuts, investors might opt to lock in current rates if they align with their long-term cash flow projections. Conversely, if a rate cut is anticipated, holding off on refinancing could be advantageous. This decision should factor in current and projected NOI, DSCR maintenance, and potential equity growth. For instance, a property with a strong DSCR might refinance now to secure stable long-term payments, whereas a property with marginal DSCR might benefit from waiting for a more favorable rate.

The existing interest rates also impact acquisition criteria and underwriting standards. Investors must now prioritize properties with high initial yields or those with clear paths to increased NOI through renovations or rent escalations. Underwriting standards are tightening, with increased scrutiny on rental histories, market comparables, and tenant quality. This shift necessitates a thorough analysis of potential acquisitions, focusing on both current income stability and future growth potential. The ability to meet or exceed DSCR thresholds without compromising on acquisition price or property quality becomes a crucial determinant in successful real estate investments.

Investment Strategy & Risk Management

In the current real estate climate, timing and strategic identification of opportunities are pivotal. As of April 2026, market fluctuations are pronounced due to recent economic volatility and interest rate adjustments. For investors utilizing Prime Property Funding’s services, identifying the right timing for acquisitions is critical. The focus should be on capitalizing on opportunities in markets where property values are temporarily suppressed but show strong potential for recovery. This often means targeting areas with robust job growth and infrastructure development, which are indicators of long-term appreciation. Investors should employ detailed market analysis to spot these opportunities, leveraging local market insights and macroeconomic indicators.

Risk factors in the current environment include rising interest rates and inflationary pressures, which can erode profit margins if not managed properly. Mitigation strategies involve adopting a more conservative approach to underwriting and acquisition. This means setting stricter criteria for property selection, such as higher minimum cap rates and ensuring assets are located in economically resilient areas. Additionally, maintaining a diversified portfolio across different asset classes and geographical locations can buffer against localized downturns. Investors should also stress-test financial models against various economic scenarios to ensure resilience.

Adjusting acquisition criteria and underwriting standards is essential in this uncertain market. Investors need to focus on properties that offer not only immediate cash flow but also long-term growth potential. This might involve prioritizing properties with existing tenancy and stable income streams over speculative development projects. Underwriting standards should include comprehensive due diligence processes, with an increased focus on tenant quality and lease terms. A conservative approach to debt structuring, such as securing fixed-rate loans rather than variable ones, can hedge against future interest rate hikes.

In summary, the key to navigating the current real estate market is a balanced approach that combines cautious optimism with rigorous risk management. By focusing on sustainable growth and resilient investment strategies, investors can effectively mitigate risks while positioning themselves for future success.

Key Considerations for Investors

- Fix-and-flip strategies: Ensure holding costs do not exceed 10% of the total project budget to maintain profitability.

- Spread risk: Diversify projects across at least three distinct property types or geographic regions.

- Exit timing: Align project completions with seasonal demand spikes, typically in spring and summer, to maximize sales prices.

- Contingency planning: Allocate a minimum of 15% contingency reserves in project budgets to manage unforeseen expenses.

- Buy-and-hold tactics: Target cap rates above 6% to ensure adequate risk-adjusted returns.

- Rent growth assumptions: Project conservative rent growth of no more than 3% annually to avoid overestimation risks.

- DSCR cushions: Maintain a DSCR of at least 1.25 to ensure sufficient income coverage over debt obligations.

- Bridge financing: Opt for draw schedules that align with project milestones to minimize interest costs.

- Geographic focus: Concentrate on emerging markets with a minimum forecasted job growth of 2% annually for best risk-adjusted returns.

- Risk mitigation: Maintain insurance coverage that exceeds replacement costs by at least 10% and conduct quarterly property inspections to ensure tenant compliance and property condition.

By adhering to these strategies and considerations, investors can confidently navigate the complexities of the current market environment, positioning themselves for both security and success.

Resources

External References

Disclaimer: This market analysis is for informational purposes only and should not be considered financial or investment advice. Market conditions can change rapidly. Consult with a qualified financial or lending professional before making any decisions.