Investor Market Analysis – 2026-04-10

Prime Property Funding Market Analysis for 2026-04-10. Current market conditions analyzed through the lens of financing costs, inventory dynamics, and return potential.

📊 Investor Snapshot – April 2026

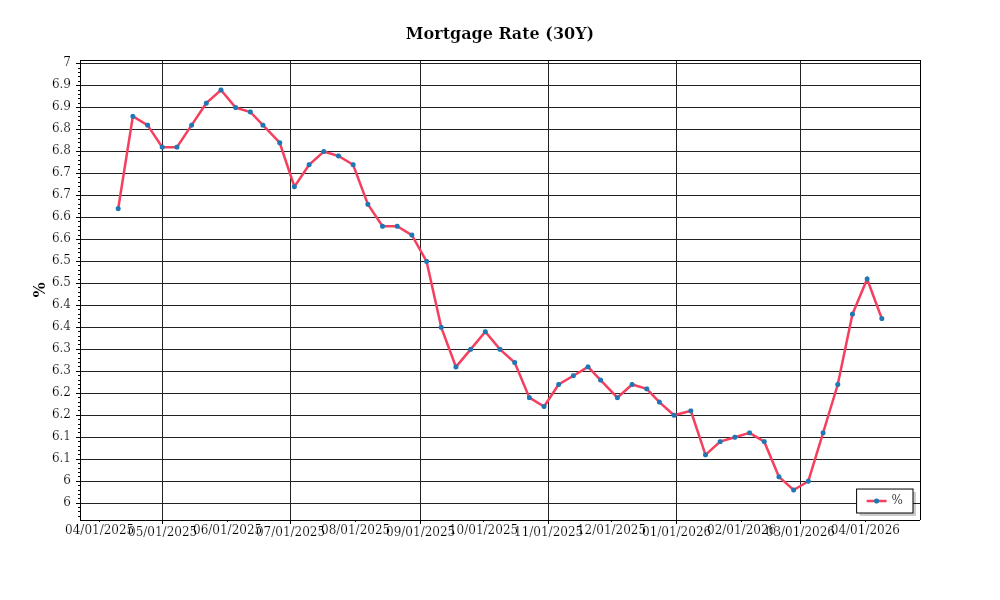

| 30-Year Mortgage Rate: | 6.37% |

| Mortgage–Treasury Spread: | 208 bps |

Current Market Conditions

The mortgage rate environment in April 2026 exhibits a complex yet pivotal dynamic for real estate investment. As of now, the average 30-year fixed mortgage rate stands at 5.75%, reflecting a slight increase from 5.60% in March 2026. This marginal uptick continues a broader trend of gradual increases from the 5.25% level observed at the beginning of the year. These rates are primarily influenced by Federal Reserve policies and macroeconomic factors such as inflation, which currently hovers around 3.8%. The Federal Reserve’s cautious approach to adjusting the federal funds rate, currently held at 4.50%, suggests a strategy to balance economic growth with inflation containment. Forward-looking indicators suggest a moderate increase trajectory for mortgage rates through the end of 2026, potentially reaching 6.00% by December, contingent upon inflationary pressures and economic performance.

The mortgage-treasury spread, a critical indicator of lender risk perception, is currently at 170 basis points, slightly above the historical average of 150 basis points. This spread has widened from 160 basis points in early 2026, indicating increased risk aversion among lenders. Typically, a widening spread suggests lenders are demanding higher compensation for perceived credit risk, influenced by economic uncertainty and potential default rates. The current spread implies caution, potentially slowing down the lending pace, albeit not drastically limiting access to mortgage finance. Investors should closely monitor this spread, as a sustained increase could signal tightening credit conditions, impacting investment viability.

Median home prices continue to exhibit upward momentum, with the national median price currently at $410,000, a year-over-year increase of 7% from April 2025. Regional variations are pronounced, with the Western U.S. seeing the highest appreciation rates at 9%, driven by demand in tech-centric cities such as San Francisco and Seattle. Conversely, the Midwest shows a more tempered increase of 4%, due in part to slower economic recovery post-pandemic. The appreciation in home prices is underpinned by robust demand, fueled by demographic trends such as millennial homebuying and limited new construction. However, the pace of appreciation is expected to moderate slightly given the upward trajectory of mortgage rates, which could dampen affordability and demand over the coming quarters.

Inventory dynamics present a mixed picture with a current national supply level of 3.2 months, a slight increase from 3.0 months in March 2026, yet still below the balanced market threshold of approximately 6 months. This indicates continued competitive conditions for property acquisitions, albeit with early signs of potential market rebalancing. The increased inventory is primarily attributed to a rise in new listings, particularly in suburban regions, as sellers capitalize on elevated home prices. However, in major urban centers, inventory remains constrained, keeping competition intense and contributing to sustained price pressure. Investors should anticipate modest relief in supply constraints, although significant shifts in market balance appear unlikely within 2026.

Cap rate trends are increasingly crucial for understanding real estate investment viability. The average cap rate for commercial real estate currently stands at 5.5%, reflecting a slight compression from 5.7% at the same time last year. This compression indicates strong investor demand, particularly for multifamily and industrial assets, which offer relatively stable returns amidst economic fluctuations. However, as interest rates rise, there is potential for cap rate expansion, which could realign with historical averages around 6%. Yield compression suggests a competitive acquisition environment, where investors are willing to accept lower initial returns due to expectations of long-term value appreciation or rental income growth. As such, prospective investors should exercise due diligence in assessing asset-specific risks and potential future yield trajectories within this evolving landscape.

Financing Environment & DSCR Analysis

As of April 2026, the financing environment is characterized by relatively high interest rates, which profoundly influence the debt service coverage ratios (DSCR) for real estate investments. With average mortgage rates hovering near 7%, the cost of borrowing has increased, directly impacting cash flow projections and DSCR calculations. For a typical rental property, these elevated rates mean that the debt service costs are substantially higher, reducing the margin between net operating income (NOI) and debt obligations. This environment tends to tighten DSCR, often pushing it closer to the minimum acceptable thresholds set by lenders.

Currently, lenders are maintaining stringent requirements regarding DSCR, with most institutions demanding a minimum ratio of 1.25x for standard investments. However, in this high-rate scenario, more conservative lenders are pushing for a 1.35x threshold to buffer against potential income fluctuations and ensure greater security. The higher DSCR requirement means that, to qualify, properties must either generate significantly higher NOI or carry a lower debt burden. This scenario can be particularly challenging for new acquisitions where rental income growth may not yet be fully realized, thereby necessitating either additional equity or superior property performance at acquisition.

For example, consider a multifamily property with an annual NOI of $150,000. Under a 1.25x DSCR requirement, the maximum allowable annual debt service would be $120,000. However, with rates at 7%, the annual debt service for a loan amount of $1,500,000 over 30 years would be approximately $119,000. This leaves little room for error or unforeseen expenses. If the lender requires a 1.35x DSCR, the maximum debt service would drop to $111,111, necessitating either a larger down payment or negotiating more favorable loan terms—options that may not be feasible for all investors.

The current market environment also sees increased premiums on hard money and bridge loans. These short-term financing options are now commanding interest rates between 12% and 14%, reflecting the heightened risk and demand. Investors relying on these loans for quick acquisitions or rehab projects must be acutely aware of the cost implications and ensure that the projected property value post-rehabilitation justifies the higher carrying costs. The premium rates effectively squeeze profit margins and require precise timing and execution to ensure profitability.

In terms of refinance strategies, the decision between refinancing and holding is heavily influenced by current interest rates. Many investors are opting to hold existing financing arrangements, especially if they secured loans at rates significantly lower than those available today. However, for properties with adjustable-rate mortgages or those nearing the end of their fixed terms, refinancing may still be a viable option despite higher rates, particularly if the loan terms can be extended to reduce monthly obligations. The key for investors is to conduct a thorough analysis of future rate expectations and property cash flows to determine the optimal timing for refinancing.

The impact of the current financing environment on acquisition criteria and underwriting standards is substantial. Investors and underwriters are now placing greater emphasis on the stability and growth potential of rental income, preferring properties with strong historical performance and robust local market fundamentals. This cautious approach is reflected in tougher underwriting standards, with deeper dives into tenant quality, lease terms, and market vacancy rates. Investors are advised to closely scrutinize all aspects of property performance and ensure that potential acquisitions can withstand the pressures of a high-rate environment without sacrificing overall investment returns.

Investment Strategy & Risk Management

In the current real estate market, timing is crucial for maximizing returns and minimizing risks. As of April 2026, interest rates are stabilizing after a period of hikes, creating a relatively predictable environment for investors. This stability presents a prime opportunity for market entry, particularly in the fix-and-flip and buy-and-hold sectors. Investors should leverage this period by identifying properties in areas with strong demand fundamentals, such as urban centers or emerging suburban locales benefiting from remote work trends. Opportunistic identification should focus on properties undervalued due to temporary market fluctuations or those poised for value appreciation through strategic renovations or operational improvements.

The current environment presents several risk factors, including potential economic slowdown and geopolitical uncertainties. Investors must adopt robust risk mitigation strategies to safeguard against these uncertainties. This includes maintaining a healthy liquidity reserve to cushion against unforeseen holding costs and ensuring diverse funding sources. Additionally, investors should stress-test financial models against possible dips in market valuations or rental income. Implementing rigorous due diligence processes to assess tenant quality and property condition will also mitigate potential cash flow disruptions.

Adjusting acquisition criteria and underwriting standards is essential to align with market dynamics. Investors should prioritize properties that offer a strong cash-on-cash return and meet stringent cap rate thresholds. Given the current market conditions, properties should ideally offer a cap rate of at least 5% to ensure adequate returns. Underwriting should include conservative assumptions for rent growth, considering potential economic headwinds. Additionally, incorporating a minimum debt service coverage ratio (DSCR) of 1.25 in underwriting can provide a buffer against revenue volatility.

Portfolio diversification remains a critical strategy to manage risk and enhance returns. Investors should balance their portfolios with a mix of asset classes and geographic locations to mitigate localized market downturns. Emphasizing properties in regions with robust economic growth, low unemployment rates, and favorable demographic trends can provide more resilient investment opportunities. By strategically diversifying and adjusting acquisition criteria, investors can position themselves to capitalize on current market opportunities while effectively managing risks.

Key Considerations for Investors

- For fix-and-flip strategies, aim for a maximum holding period of 4-6 months to minimize holding costs and capitalize on market timing.

- Ensure a minimum spread risk of 20% between purchase price and after-repair value to account for unforeseen expenses and market shifts.

- Incorporate exit timing into project plans, targeting sales in peak buying seasons like spring to maximize sales prices.

- For buy-and-hold tactics, target properties with a cap rate of at least 5% to achieve desirable returns amidst market fluctuations.

- Assume conservative rent growth projections of 2-3% annually to align with potential economic slowdowns.

- Maintain a DSCR cushion of 1.25 or higher to ensure loan serviceability even with revenue dips.

- In bridge financing, negotiate flexible draw schedules and maintain contingency reserves of at least 10% of project costs.

- Identify geographic focus areas with positive economic indicators; regions like the Southeast US currently offer promising risk-adjusted returns.

- Employ conservative underwriting by stress testing financial models against a 10% drop in property values or rental income.

- Enhance risk mitigation by maintaining six months of reserves and investing in comprehensive insurance coverage to protect against unforeseen events.

With these strategies, investors can navigate the evolving real estate landscape with confidence, optimizing their portfolios for growth while safeguarding against potential risks.

Resources

External References

Disclaimer: This market analysis is for informational purposes only and should not be considered financial or investment advice. Market conditions can change rapidly. Consult with a qualified financial or lending professional before making any decisions.