Investor Market Analysis – 2026-04-09

Prime Property Funding Market Analysis for 2026-04-09. Current market conditions analyzed through the lens of financing costs, inventory dynamics, and return potential.

📊 Investor Snapshot – April 2026

| 30-Year Mortgage Rate: | 6.46% |

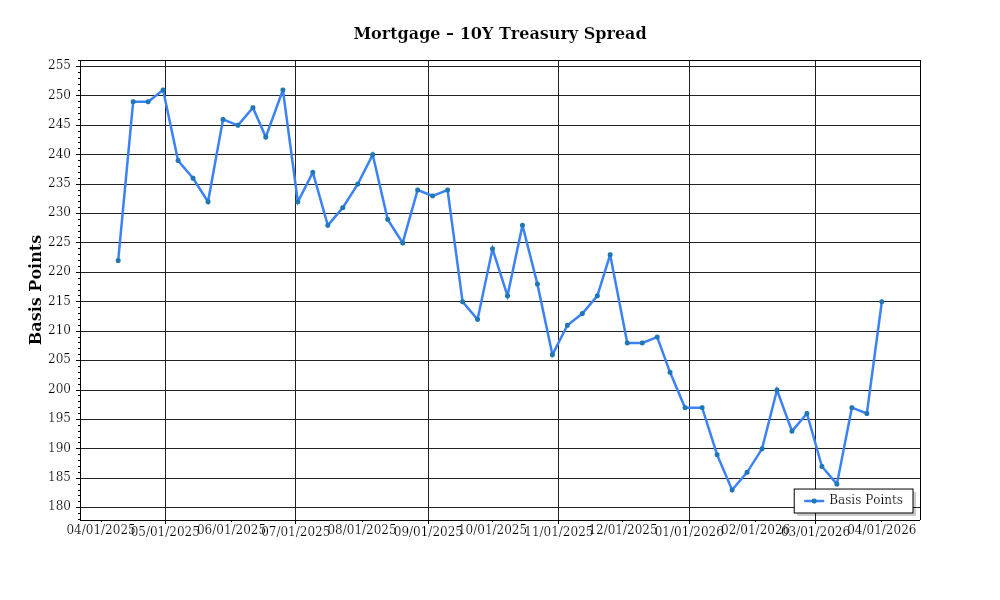

| Mortgage–Treasury Spread: | 213 bps |

Current Market Conditions

As of April 2026, the mortgage rate environment is characterized by a notable stability following a volatile period in the previous year. Current average mortgage rates stand at 5.1% for a 30-year fixed-rate mortgage, representing a slight decrease from 5.4% observed at the start of the year. This stabilization can be attributed to recent monetary policy decisions aimed at tempering inflation, which has successfully reduced the upward pressure on borrowing costs. Over the past six months, the trend has indicated a modest downward trajectory, providing a more favorable borrowing environment for prospective homeowners and investors alike. The Federal Reserve’s current stance suggests that if inflationary pressures remain contained, mortgage rates are likely to continue on this stable path, potentially encouraging increased real estate market activity.

The mortgage-treasury spread, which serves as a critical indicator of lender risk perception, currently averages 1.7%. This spread is slightly narrower than the historical average of 2.0%, suggesting that lenders perceive reduced credit risk in the housing market. The recent narrowing of this spread can be attributed to enhanced economic stability and improved borrower credit profiles. In practical terms, this signals a more competitive lending environment, where banks and financial institutions are more willing to extend credit at favorable terms. This reduction in perceived risk is likely to support continued investment in the housing market, as lenders are more optimistic about the economic outlook and the strength of the real estate sector.

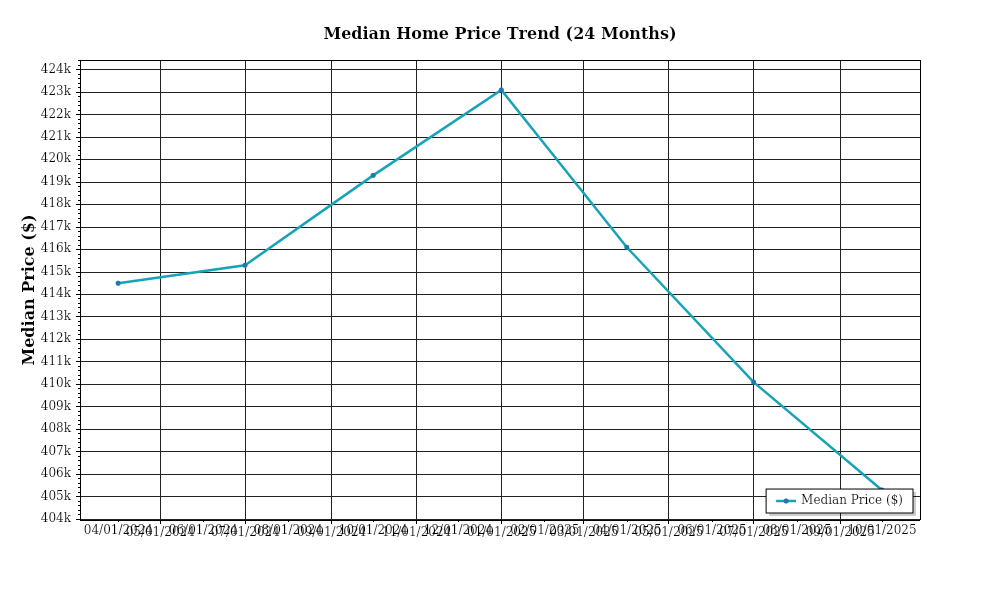

The median home price across the United States has been on an upward trajectory, with the current median price reaching $425,000, marking a 5.3% increase year-over-year. This growth rate, while robust, reflects a deceleration from the double-digit appreciation rates experienced in the early 2020s. Regional variations remain pronounced, with the West Coast experiencing higher appreciation rates of 6.8% compared to the national average, driven by persistent demand and constrained supply. In contrast, the Midwest shows more modest growth at 3.9%, indicative of a more balanced market. For investors, these variations highlight the importance of geographic diversification and the need to assess local market conditions when considering acquisitions.

Inventory dynamics continue to play a crucial role in shaping the current market landscape. Nationally, the housing supply remains constrained, with the months of supply metric hovering at 3.2 months, below the 6-month threshold typically indicative of a balanced market. This limited supply has cultivated a competitive environment, as buyers vie for available properties, often resulting in bidding wars and upward pressure on prices. However, there has been a slight uptick in new housing starts, with a 4.5% increase in the number of permits issued compared to the previous year, suggesting a potential easing of supply constraints in the near future. The current market imbalance underscores the lucrative opportunities for developers and investors to capitalize on unmet demand.

Cap rates, which are critical in assessing property investment viability, have shown signs of compression, with the national average cap rate currently at 5.8%, down from 6.2% a year ago. This trend is indicative of increased competition among investors seeking yield in a low-interest-rate environment. The compression of cap rates suggests that investors are willing to accept lower returns in exchange for the perceived safety and long-term appreciation potential of real estate assets. For investors, this environment necessitates a strategic approach, focusing on assets with strong income potential and growth prospects to ensure returns that justify the compressed yields. The current landscape emphasizes the importance of careful asset selection and management to optimize investment outcomes.

Financing Environment & DSCR Analysis

As of April 2026, the financing environment is characterized by a complex interplay of interest rates and economic indicators that significantly influence the Debt Service Coverage Ratio (DSCR). Current interest rates for traditional mortgage financing hover around 6.5% for residential properties and are slightly higher for commercial real estate, averaging approximately 7.2%. These rates are having a tangible impact on DSCR, a critical metric for determining a property’s ability to cover its debt obligations. Higher interest rates increase monthly debt service payments, thereby reducing the DSCR. For example, a property generating $10,000 in monthly net operating income (NOI) with a monthly debt service payment of $8,000 would have a DSCR of 1.25. However, if interest rates increase the debt service to $8,500, the DSCR drops to 1.18, potentially breaching lender requirements.

In the current market, lenders typically require a minimum DSCR of 1.25x for residential rental properties, though commercial and riskier asset classes may see thresholds as high as 1.35x. These requirements ensure that property cash flows can adequately cover debt obligations while maintaining a buffer for unforeseen expenses. In practice, this means that investors must either increase property income or reduce debt levels to meet these stricter underwriting standards. For instance, a multi-family building with a $9,000 monthly debt service would need to generate at least $11,250 in NOI to meet a 1.25x DSCR requirement. This environment pressures owners to optimize property management strategies, potentially increasing rents or seeking operational efficiencies to bolster NOI.

Cash flow implications are significant in this high-rate market. Using a simplified example, consider a rental property with monthly rental revenue of $15,000 and operating expenses of $5,000, resulting in an NOI of $10,000. With an interest rate of 6.5%, a loan amounting to $1,200,000 over 20 years would result in monthly payments of around $8,955, yielding a DSCR of approximately 1.12, below the typical lender threshold. To improve this ratio to at least the 1.25x standard, the property would need to either increase NOI to approximately $11,194 or reduce the loan amount. This scenario illustrates the cash flow squeeze investors face, prompting them to consider refinancing or restructuring debt to maintain financial health.

Hard money and bridge loans, essential tools for short-term financing, are experiencing rate premiums in the current market. These loans, often used for property flips or to bridge the gap during property transitions, are currently priced between 10% and 12%, reflecting the increased risk perceived by lenders in a volatile interest rate environment. The elevated cost of these loans underscores the importance of efficient project execution and rapid asset stabilization to mitigate the financial burden of high interest payments.

Given the current rate environment, investors face challenging decisions regarding refinance and hold strategies. Refinancing existing debt at current rates could lock in higher payments, adversely affecting cash flow and potentially DSCR. Conversely, holding off on refinancing in anticipation of potential rate reductions could be advantageous, though it carries the risk of ongoing exposure to variable rates. This decision-making process necessitates a careful analysis of market forecasts and a thorough understanding of property-specific cash flow dynamics.

The impact on acquisition criteria and underwriting standards is pronounced. Investors are increasingly conservative, focusing on properties with stable cash flows and potential for value appreciation. Underwriting standards have tightened, with increased scrutiny on NOI projections and sensitivity analyses that account for potential interest rate hikes. As a result, properties in prime locations with strong rental demand are favored, while those in secondary markets or with significant repositioning needs may struggle to secure favorable financing terms. This shift requires investors to adopt a more selective approach, prioritizing assets that align with stricter financial and operational benchmarks to ensure sustainable investment performance.

Investment Strategy & Risk Management

In the current real estate market, characterized by fluctuating interest rates and evolving economic dynamics, strategic timing and opportunity identification are paramount. Investors should remain vigilant, targeting acquisitions during periods when market sentiment is low, as this can lead to better entry prices. This approach is particularly pertinent when observing seasonal trends; for example, the late fall and winter months often see reduced buyer activity, creating potential for advantageous purchases. Identifying properties requiring minimal renovations in these periods can help mitigate holding costs and expedite the time to market upon completion.

Considering the prevailing economic uncertainties, investors must be acutely aware of risk factors that could impact their portfolios. Inflationary pressures and potential interest rate hikes pose significant risks, affecting both property values and borrowing costs. To mitigate these risks, investors should prioritize properties with strong cash flow potential and those located in regions with robust economic fundamentals. Additionally, diversifying across asset classes and geographical locations can help cushion against localized downturns.

Adjustments to acquisition criteria and underwriting standards are essential in navigating this complex environment. Prime Property Funding should encourage investors to adopt more conservative underwriting standards, factoring in stress testing scenarios that include potential increases in interest rates and longer-than-anticipated vacancy periods. This conservative approach ensures that investments remain viable under a range of economic conditions. Furthermore, acquisition criteria should emphasize properties with strong cap rates and DSCR (Debt Service Coverage Ratio) cushions to withstand potential income fluctuations.

In conclusion, while the current market presents challenges, it also offers opportunities for those who are well-prepared and strategically minded. By focusing on market timing, risk management, and conservative acquisition strategies, investors can position themselves to capitalize on the evolving landscape. This proactive approach not only safeguards against downside risks but also enhances potential returns, paving the way for successful real estate investing in 2026.

Key Considerations for Investors

- Fix-and-flip strategies: Maintain holding costs below 10% of the project budget to preserve profitability. Implement contingency plans with a 5% buffer for unexpected expenses.

- Exit timing: Aim to complete flips and list properties during the spring peak season, when buyer interest typically surges, to maximize sale prices.

- Buy-and-hold tactics: Target a minimum cap rate of 7% to ensure adequate returns, while incorporating a 3% annual rent growth assumption to offset inflation.

- DSCR cushions: Maintain a DSCR of 1.25 or higher to provide a sufficient buffer against fluctuations in rental income.

- Bridge financing: Opt for fixed-rate loans to hedge against interest rate volatility, and establish contingency reserves equal to three months of debt service.

- Draw schedules: Align draw schedules with project milestones to optimize cash flow and reduce financing costs.

- Market timing: Prioritize acquisitions in regions with projected population growth exceeding 2% annually, as these areas are likely to experience sustained demand.

- Geographic focus: Focus on emerging markets in the Sun Belt, which offer favorable demographic trends and better risk-adjusted returns.

- Conservative underwriting: Stress test properties assuming a 2% increase in interest rates and a 5% drop in rental income to ensure resilience.

- Risk mitigation: Establish reserve funds equivalent to 6 months of operating expenses and prioritize properties with high-quality tenants and sound physical condition.

By implementing these strategies, investors can confidently navigate the current real estate market, capitalize on emerging opportunities, and effectively manage risks.

Resources

External References

Disclaimer: This market analysis is for informational purposes only and should not be considered financial or investment advice. Market conditions can change rapidly. Consult with a qualified financial or lending professional before making any decisions.