Investor Market Analysis – 2026-04-02

Prime Property Funding Market Analysis for 2026-04-02. Current market conditions analyzed through the lens of financing costs, inventory dynamics, and return potential.

📊 Investor Snapshot – April 2026

| 30-Year Mortgage Rate: | 6.38% |

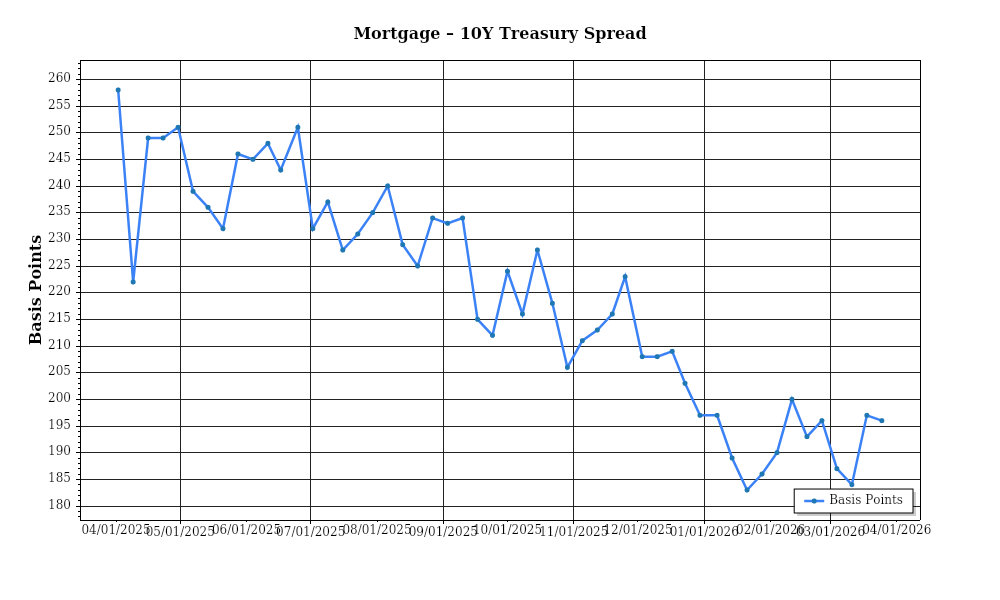

| Mortgage–Treasury Spread: | 208 bps |

Current Market Conditions

The U.S. residential real estate market is currently navigating a complex landscape shaped by fluctuating mortgage rates, evolving lender risk perceptions, and shifting demand-supply dynamics. As of April 2026, the average mortgage rate for a 30-year fixed loan stands at 5.8%, marking a significant increase from the 4.3% observed in April 2025. This rise in rates follows the Federal Reserve’s continued efforts to counter inflationary pressures by tightening monetary policy. The trajectory of mortgage rates has been upward over the past year, with monthly increases averaging around 0.1% since January 2025. This trend is likely to persist as economic indicators suggest sustained inflationary trends, potentially dampening homebuyer affordability and demand.

The mortgage-treasury spread, a critical indicator of lender risk perception, offers further insights into current market conditions. As of April 2026, the spread between the 30-year mortgage rate and the 10-year U.S. Treasury yield is approximately 2.4%. Historically, this spread hovers around 1.8% to 2.0%, indicating that lenders perceive greater risk in the mortgage market today than in previous periods. This expansion in the spread suggests heightened caution among lenders, likely driven by macroeconomic uncertainties and potential borrower credit risks. The elevated spread can signal tighter lending standards ahead, which could further constrain credit availability and impact homebuyer activity.

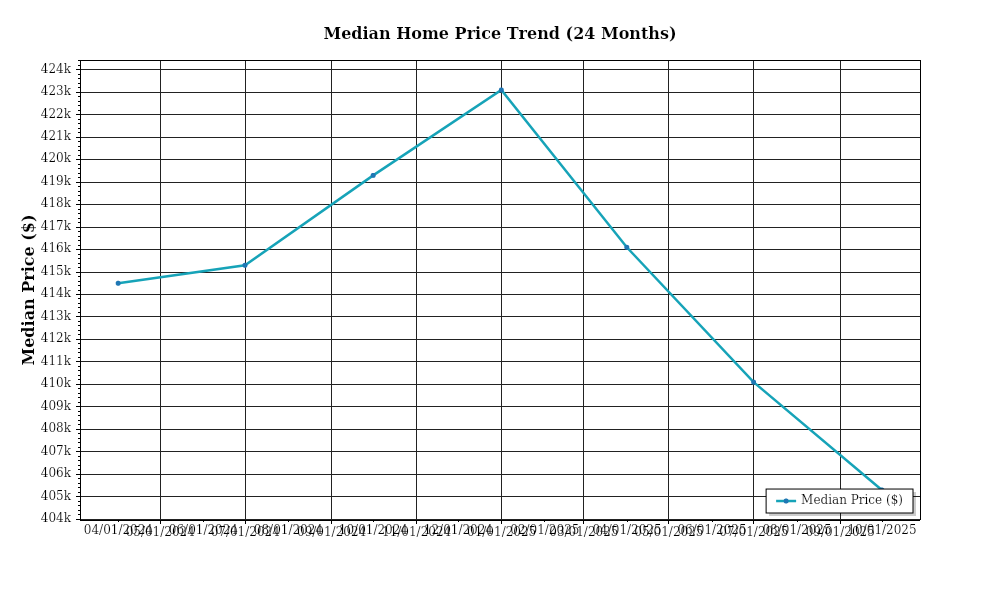

Median home prices have continued to appreciate, albeit at a moderated pace compared to the double-digit growth seen during the pandemic years. Nationally, the median home price as of April 2026 is $437,000, reflecting a year-over-year increase of 6%. This rate of appreciation is a deceleration from the 9% observed in April 2025, aligning with the cooling effects of rising mortgage rates. Regional variations are notable, with the South and Midwest experiencing higher appreciation rates of 7% and 8% respectively, driven by continued in-migration and relatively affordable housing. In contrast, the Northeast and West have seen more modest increases of 3% and 4%, impacted by affordability constraints and plateauing demand.

Inventory dynamics remain a critical factor in understanding current market conditions. As of April 2026, national housing inventory levels are at 1.4 million units, representing a 5% increase from the previous year. Despite this rise, the market continues to exhibit characteristics of a seller’s market, with months’ supply of homes at 3.2 months, below the balanced market threshold of six months. Competition for acquisitions remains fierce, particularly in suburban and rural areas where demand has outstripped supply. The increased inventory has provided some relief to prospective buyers, yet the market remains skewed towards sellers due to persistent low supply levels relative to demand.

Cap rate trends in the residential real estate sector further illustrate the current market dynamics. The average cap rate for single-family rental properties stands at 5.2% in April 2026, down from 5.5% in April 2025, indicating yield compression. This trend reflects strong investor demand for real estate assets as a hedge against inflation, coupled with expectations of continued property value appreciation. However, the narrowing of cap rates suggests that investors are accepting lower yields, potentially increasing their risk exposure. This yield compression is particularly pronounced in high-demand regions such as the Sun Belt, where cap rates have fallen by 0.4% percentage points over the past year, driven by robust rental demand and limited supply growth.

In summary, the current real estate market is characterized by rising mortgage rates, an expanded mortgage-treasury spread, moderate home price appreciation, constrained inventory levels, and cap rate compression. These factors collectively paint a picture of a market in transition, with potential headwinds from tightening financial conditions and evolving investor strategies.

Financing Environment & DSCR Analysis

In April 2026, the current interest rate landscape presents significant challenges and opportunities for real estate investors, particularly those seeking to optimize their Debt Service Coverage Ratios (DSCR). With average interest rates for commercial real estate loans hovering around 6.5%, the impact on DSCR is profound. Higher interest rates increase monthly debt obligations, thus requiring properties to generate more income to maintain healthy coverage ratios. As a result, investors must meticulously assess their properties’ income potential to ensure compliance with lender requirements.

The typical DSCR requirements in this environment have become more stringent, with many lenders favoring a threshold of 1.35x over the previously common 1.25x. This shift reflects lenders’ increased caution and desire for a greater buffer against potential income fluctuations. For example, on a property with an annual debt service of $100,000, a 1.35x DSCR requirement necessitates a net operating income (NOI) of at least $135,000, compared to $125,000 under a 1.25x requirement. This higher threshold can significantly impact investors’ ability to secure financing, particularly for properties with tight profit margins.

The implications for cash flow are substantial. Consider a rental property generating $12,000 in monthly gross income, with operating expenses totaling $4,000. This leaves a monthly NOI of $8,000. With a 6.5% interest rate on a loan of $1,500,000, the monthly debt service is approximately $9,500, resulting in a DSCR of 0.84x, which is below acceptable levels. To achieve a 1.35x DSCR, the property would need to generate an NOI of $12,825, necessitating either a significant rent increase or cost reduction, both of which present their own challenges in a competitive rental market.

In this context, hard money and bridge loan rate premiums have become more pronounced. With rates often 2-3% higher than traditional loans, these options, while offering quick access to capital, demand careful consideration. Hard money loans currently average around 9% to 10%, which can push the DSCR further down if the increased interest burden isn’t matched by proportional revenue gains. Investors must weigh the benefits of rapid acquisition or renovation capabilities against the financial strain of higher interest costs.

Given this rate environment, the timing of refinancing vs holding becomes crucial. Investors with existing loans at lower fixed rates may opt to hold to avoid locking in higher rates through refinancing. Conversely, those with adjustable-rate loans facing potential hikes may consider refinancing sooner to secure slightly better terms or diversify into fixed rates. The decision hinges on projected rate trends, property performance, and broader market conditions.

Finally, these dynamics significantly shape acquisition criteria and underwriting standards. Investors must prioritize properties with proven income stability and growth potential to meet elevated DSCR thresholds. Underwriting standards have tightened, with lenders demanding more rigorous income documentation and stress testing against potential interest rate increases. This emphasizes the importance of comprehensive due diligence and realistic income projections when assessing new acquisitions.

In summary, the current financing environment demands heightened vigilance and strategic planning. By understanding the intricacies of DSCR requirements and interest rate impacts, investors can make informed decisions to optimize their portfolios while mitigating financial risks.

Investment Strategy & Risk Management

In the current real estate market of April 2026, investors should be acutely aware of timing their entries and exits to maximize returns while minimizing risks. The market is displaying signs of stabilization after a period of volatility, offering opportunities for both fix-and-flip and buy-and-hold strategies, but careful consideration must be given to market cycles and economic indicators. Investors should focus on identifying undervalued properties in emerging neighborhoods where appreciation is likely, leveraging Prime Property Funding’s financial products tailored for such scenarios.

Risk factors in the current environment include potential interest rate hikes and regulatory changes impacting financing options. To mitigate these risks, investors can employ strategies such as locking in fixed interest rates where possible and maintaining flexible exit strategies. Additionally, diversification across asset classes and geographic locations helps spread risk. For instance, while coastal markets might offer high returns, they also come with increased risk, thus balancing investments in stable inland markets could mitigate potential losses.

Adjusting acquisition criteria and underwriting standards is crucial in this environment. Investors should focus on properties with high-profit margins and ensure thorough due diligence is performed. Acquisition criteria should include a strong emphasis on property condition and location desirability. Underwriting standards must stress test various economic scenarios, incorporating conservative rent growth projections and cap rate analyses to ensure investments remain viable under different market conditions.

Moreover, investors should refine their portfolio strategies to include a mix of short-term and long-term investments, capitalizing on market fluctuations. Employing data-driven decision-making and leveraging advanced analytics to forecast trends will enhance investment outcomes. The integration of technology in market analysis can provide insights that were previously unavailable, aiding in more precise decision-making.

Key Considerations for Investors

- **Fix-and-flip strategies**: Allocate a contingency reserve of at least 10% of the total project cost to handle unforeseen expenses, ensuring projects remain profitable despite market fluctuations.

- **Exit timing**: Aim to complete and sell fix-and-flip projects within a 6-9 month window to capitalize on seasonal market peaks and avoid prolonged holding costs.

- **Buy-and-hold tactics**: Target a minimum cap rate of 6% to account for potential increases in interest rates and ensure sustainable cash flow.

- **Rent growth assumptions**: Assume a conservative annual rent growth rate of 3% to stress test cash flow projections and maintain positive cash-on-cash returns.

- **Bridge financing**: Opt for draw schedules that align with project milestones and maintain a contingency reserve of 15% of the financing amount to buffer against unexpected delays.

- **Market timing**: Balance acquisition opportunities with holding costs by identifying properties that can be acquired at a discount during slower market periods but sold at a premium during peak seasons.

- **Geographic focus**: Consider secondary markets with growth potential, such as those in the Sun Belt, which offer better risk-adjusted returns compared to over-saturated coastal areas.

- **Conservative underwriting**: Implement stress testing for 1.5x DSCR under various economic conditions to ensure financial resilience.

- **Portfolio diversification**: Diversify across asset classes such as residential, commercial, and industrial properties to balance risk and capitalize on different market trends.

- **Risk mitigation**: Maintain a reserve fund covering at least six months of operating expenses and prioritize properties in good condition with high tenant quality to minimize vacancy and maintenance costs.

By integrating these strategies, investors can navigate the real estate market with confidence, making informed decisions that optimize returns while safeguarding against potential risks.

Resources

External References

Disclaimer: This market analysis is for informational purposes only and should not be considered financial or investment advice. Market conditions can change rapidly. Consult with a qualified financial or lending professional before making any decisions.