Investor Market Analysis – 2026-03-25

Prime Property Funding Market Analysis for 2026-03-25. Current market conditions analyzed through the lens of financing costs, inventory dynamics, and return potential.

📊 Investor Snapshot – March 2026

| 30-Year Mortgage Rate: | 6.22% |

| Mortgage–Treasury Spread: | 188 bps |

Current Market Conditions

As of March 2026, the mortgage rate environment remains a critical factor in the real estate market’s trajectory. Current average mortgage rates for 30-year fixed-rate loans are hovering around 5.8%, a notable decrease from the highs of 7.1% observed in 2024. This decline has been gradual, with rates falling approximately 20 basis points over the past six months. The decrease is largely attributed to the Federal Reserve’s recent adjustments in monetary policy, which have aimed to stabilize economic growth. While rates remain elevated compared to pre-pandemic levels, the downward trend provides a more favorable borrowing environment for prospective homebuyers and investors, increasing affordability and potentially stimulating demand in the housing market.

A significant metric to consider is the mortgage-treasury spread, which currently sits at 1.6%. This spread has compressed from earlier levels of 2.2% seen in late 2024. The reduction in this spread indicates a lower perceived risk among lenders, suggesting that credit conditions have eased somewhat. This compression reflects improved economic stability and a more optimistic outlook from lenders, who are more confident in borrowers’ ability to repay loans. However, it’s essential to monitor this spread closely, as any widening could signal increased risk aversion and potential tightening of credit conditions.

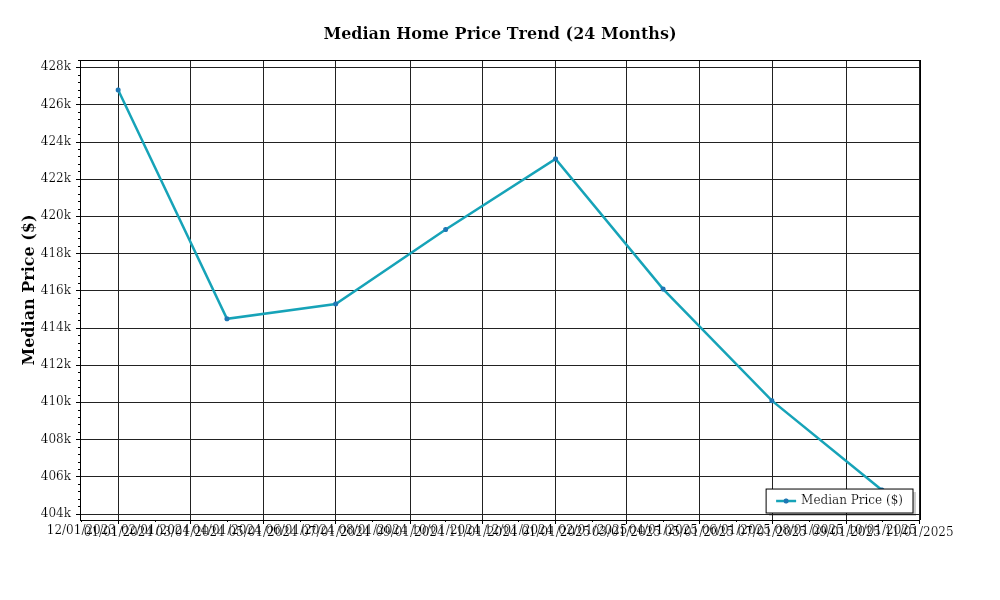

The median home price in the United States stands at $420,000, representing a 5% year-over-year increase. While this appreciation rate marks a deceleration from the double-digit growth rates witnessed during the pandemic-fueled housing boom, it indicates a return to more sustainable levels. Regional variations are evident, with the Southeast experiencing the highest appreciation at 7.5%, driven by robust job growth and population influx. In contrast, the Midwest sees more modest gains of 3% due to slower economic expansion. These disparities highlight the importance of regional market dynamics in driving home price trends, impacting investment strategies across different geographic areas.

Inventory dynamics continue to play a pivotal role in shaping the real estate landscape. Nationally, housing inventory levels have increased by 12% year-over-year, with approximately 1.3 million units now available. This rise in inventory has eased some of the intense competition witnessed in previous years, pushing the market toward a more balanced state. However, the months’ supply of homes remains at 3.5 months, indicating that the market still favors sellers overall. This metric suggests that while buyers have more options, they must act swiftly to secure desirable properties, particularly in high-demand areas.

Cap rate trends provide further insight into the current market conditions. Nationally, cap rates have remained stable at around 5.5%, reflecting a balance between property income and value expectations. However, variations persist across different property types and locations. Multifamily properties in urban centers show slight yield compression, with cap rates averaging 4.8%, driven by sustained demand for rental units. Conversely, retail properties in suburban areas exhibit yield expansion, with cap rates reaching 6.3% due to ongoing challenges in the retail sector. These trends indicate investors’ cautious optimism, balancing risk and return as they navigate evolving market conditions.

Financing Environment & DSCR Analysis

In March 2026, the financial landscape for real estate investors is shaped by an interest rate environment that remains elevated compared to historical norms. The current average interest rate for a 30-year fixed mortgage hovers around 6.5%, which is significantly higher than the sub-4% rates seen in early 2020. This increased cost of borrowing directly impacts the Debt Service Coverage Ratio (DSCR), a critical metric for lenders assessing the risk associated with property loans. The DSCR, calculated by dividing net operating income (NOI) by total debt service, is under pressure as higher interest rates increase monthly debt obligations, reducing the ratio unless offset by proportionate increases in rental income.

Typical DSCR requirements in this current environment are tightening. Lenders are generally expecting a minimum DSCR of 1.35x, a step up from the more lenient 1.25x threshold commonly accepted when rates were lower. This higher threshold is a protective measure, ensuring that properties generate sufficient income to cover increased debt costs and provide a buffer. For example, a rental property generating $100,000 in NOI would need to service no more than $74,074 in debt annually to meet a 1.35x DSCR requirement. This compares to $80,000 in allowable debt service under a 1.25x requirement, illustrating a significant tightening in lending standards.

The implications for cash flow are profound. Consider a rental property purchased for $2 million, with a 20% down payment and a $1.6 million mortgage. At an interest rate of 6.5%, the annual debt service is approximately $121,632. To meet the stricter 1.35x DSCR requirement, the property must generate at least $164,204 in NOI. If rental income does not sufficiently cover these increased debt costs, investors may face negative cash flow, necessitating either rental rate increases, expense reductions, or additional equity injections to maintain the desired cash flow levels.

In this high-rate environment, hard money and bridge loans are commanding significant premiums. Current rates for these short-term financing solutions can exceed 10%, reflecting both the additional risk and the scarcity of capital willing to engage in these high-leverage, high-risk loans. Investors utilizing these mechanisms face even greater pressure on DSCR, often needing to demonstrate ratios well above standard thresholds to secure favorable terms. This makes refinancing into traditional, lower-rate products a key strategy, assuming rates stabilize or decrease in the near future.

The dilemma of refinance timing versus hold strategies is particularly acute. Given the elevated rates, immediate refinancing may not be advantageous unless securing significantly better terms. However, holding on to current financing and waiting for potential rate declines involves risk, particularly if economic conditions worsen or if property values decline. This uncertainty requires careful consideration of market trends, future rate forecasts, and property-specific factors like tenant stability and lease structures.

Finally, the current financing environment significantly impacts acquisition criteria and underwriting standards. Investors and underwriters are more cautious, focusing on properties with strong cash flow histories and resilient location-based demand. Underwriting is more stringent, with greater emphasis on thorough due diligence, including sensitivity analyses that account for potential interest rate fluctuations and stress testing rental income scenarios. Properties with stable, long-term lease agreements and tenants with strong credit profiles are favored, as they offer more predictable income streams to support DSCR requirements.

In summary, the current financing environment presents challenges and opportunities for real estate investors. The impact of high interest rates on DSCR, coupled with tighter lending standards, necessitates a strategic approach to property acquisition and management. Understanding these dynamics and effectively managing cash flow and refinancing strategies is crucial for navigating this complex market.

Investment Strategy & Risk Management

In the current market environment, strategic timing and opportunity identification are crucial for maximizing returns on real estate investments. As we progress through 2026, market dynamics are influenced by several factors, including changing interest rates, shifting economic policies, and evolving consumer preferences. Investors should focus on identifying markets with strong growth potential and favorable demographic trends. Timing plays a pivotal role; investors need to weigh the potential benefits of immediate acquisitions against the risks of holding costs in uncertain economic conditions. Understanding seasonal patterns and local market cycles can provide a competitive edge, allowing investors to enter and exit positions profitably.

Risk factors in the present environment are multifaceted, with economic volatility, regulatory changes, and potential market corrections leading the charge. To mitigate these risks, investors should adopt a multifaceted approach. Diversification across asset classes and geographical locations can buffer against localized downturns. Additionally, maintaining liquidity reserves and insurance policies can provide financial cushioning. Employing conservative underwriting standards is essential; stress testing financial models against worst-case economic scenarios can ensure robustness. Investors should also enhance due diligence processes, focusing on tenant quality and property conditions to minimize operational risks.

Adjusting acquisition criteria and underwriting standards is imperative in this fluctuating environment. Investors should increase their focus on cash flow stability and robustness of income sources. Adjusting cap rate targets to reflect current economic realities, and carefully evaluating rent growth assumptions can better align expectations with market conditions. More stringent DSCR (Debt Service Coverage Ratio) requirements and cash-on-cash return thresholds should be implemented to ensure investments can withstand economic pressures. As the lending landscape evolves, maintaining flexibility in financing structures and focusing on the terms of bridge loans, including rate environments and draw schedules, is vital.

As Prime Property Funding continues to provide essential financial services such as hard money loans and DSCR loans, the emphasis must be on strategic foresight and proactive risk management. By aligning financial products with market conditions and investor needs, the firm can help investors navigate the complexities of the current real estate landscape with confidence and precision.

Key Considerations for Investors

- Fix-and-flip strategies: Prioritize properties with holding costs under 5% of ARV to minimize financial strain during project overruns.

- Exit timing: Aim for a completion and sale before Q4 to avoid seasonal slowdowns that could impact valuation and buyer interest.

- Contingency planning: Set aside at least 10% of the project budget as a contingency reserve to cover unexpected expenses.

- Buy-and-hold tactics: Target properties with cap rates above 6% to ensure adequate returns in a high-interest-rate environment.

- DSCR cushions: Maintain a minimum DSCR of 1.25 to buffer against fluctuations in income and expenses.

- Bridge financing: Lock in fixed rates where possible and establish draw schedules aligned with project milestones to manage cash flow.

- Geographic focus: Consider secondary markets showing population growth over 3% annually for better risk-adjusted returns.

- Conservative underwriting: Apply stress tests assuming a 20% decline in property values to ensure resilience.

- Portfolio diversification: Allocate no more than 30% of the portfolio to any single asset class or geographic region to mitigate concentration risk.

- Risk mitigation: Ensure properties have comprehensive insurance coverage and conduct thorough tenant screenings to reduce operational risks.

In conclusion, by adopting a disciplined approach to market timing, risk management, and investment criteria adjustments, investors can effectively navigate the complexities of the 2026 real estate market. With strategic foresight and robust planning, Prime Property Funding and its investors are well-positioned to capitalize on opportunities and achieve sustainable growth.

Resources

External References

Disclaimer: This market analysis is for informational purposes only and should not be considered financial or investment advice. Market conditions can change rapidly. Consult with a qualified financial or lending professional before making any decisions.