Investor Market Analysis – 2026-03-11

Prime Property Funding Market Analysis for 2026-03-11. Current market conditions analyzed through the lens of financing costs, inventory dynamics, and return potential.

📊 Investor Snapshot – March 2026

| 30-Year Mortgage Rate: | 6.00% |

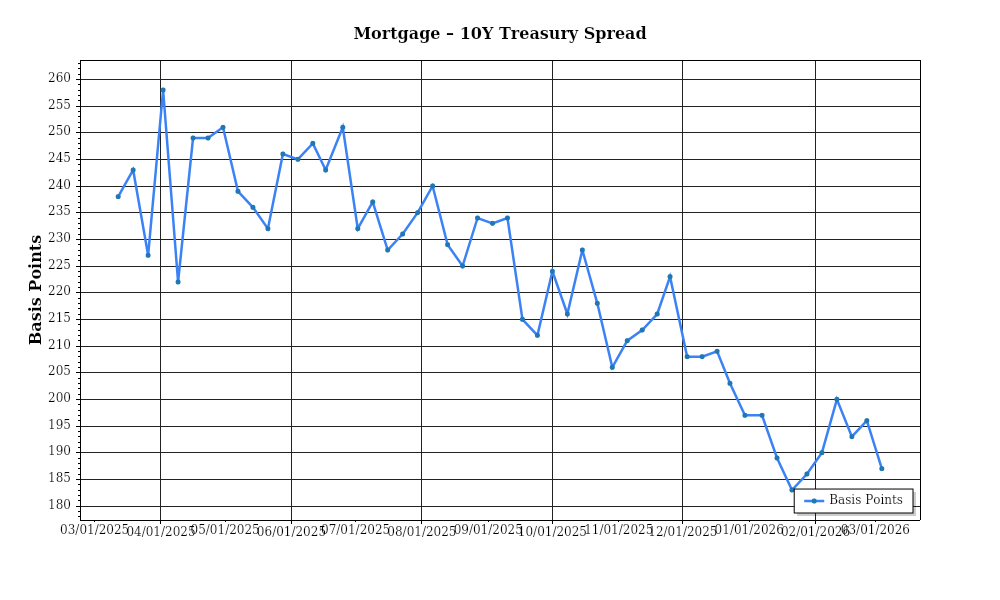

| Mortgage–Treasury Spread: | 188 bps |

Current Market Conditions

As of March 2026, the mortgage rate environment is experiencing considerable fluctuations characterized by a delicate interplay of macroeconomic forces. Current mortgage rates are holding steady at an average of 5.2% for a 30-year fixed-rate mortgage, which represents a slight increase from 4.9% in December 2025. This uptick is largely a response to the Federal Reserve’s recent decision to maintain a more hawkish stance on inflation, which has resulted in incremental rate hikes over the past year. The trajectory of mortgage rates suggests a cautious upward trend as the Fed aims to balance inflation control with sustaining economic growth. In practical terms, this environment translates to increased borrowing costs for homebuyers, which may temper demand growth and put pressure on affordability, particularly in high-cost regions.

An analysis of the mortgage-treasury spread reveals significant insights into lender risk perception in the current market. As of March 2026, the spread between the average 30-year fixed mortgage rate and the 10-year Treasury yield stands at approximately 210 basis points. This spread has narrowed from 230 basis points recorded in the same period last year, signaling a shift in how lenders perceive risk. The compression of this spread suggests that lenders are exhibiting increased confidence in borrower creditworthiness and economic stability. However, it also indicates a competitive mortgage lending environment where institutions are vying for market share, potentially leading to more lenient lending criteria. For investors, a narrower spread could signal a favorable borrowing environment, albeit with increased scrutiny on the sustainability of such narrow margins.

The median home price in the United States continues to exhibit robust growth, driven by persistent demand and constrained supply. As of the latest data, the national median home price is $405,000, reflecting a year-over-year appreciation rate of 6.5%. This appreciation shows a deceleration from the previous year’s rate of 8.1%, indicating a potential cooling in the market. Regionally, variations are pronounced, with the South and West experiencing higher median prices—$420,000 and $450,000 respectively—compared to the Midwest at $320,000. The Northeast remains relatively stable at $380,000. These figures suggest that while growth is evident, regional disparities are influenced by factors such as local economic conditions, employment rates, and population shifts, affecting long-term investment strategies.

Inventory dynamics are critical to understanding current market balance and competition levels. Recent data indicates that the housing market is operating with a supply level of approximately 3.2 months, which is below the balanced market threshold of 6 months. This low inventory level points to a seller’s market, characterized by high competition among buyers and upward pressure on pricing. The constrained supply is exacerbated by factors such as labor shortages in the construction industry and regulatory hurdles, which have hampered new housing developments. For investors, this environment underscores the importance of strategic acquisitions and the potential for capital appreciation, albeit with considerations for timing and regional market nuances.

Cap rate trends are a crucial metric for real estate investors, reflecting the yield on investment properties. Currently, cap rates for prime properties are averaging 5.4%, down from 5.7% in the previous year, indicating yield compression. This trend of declining cap rates is a result of strong investor demand driving up property prices faster than rental income growth. While lower cap rates usually signify a robust market, they also hint at reduced potential returns, particularly in high-demand areas. Investors need to weigh the implications of yield compression against the backdrop of rising property values and consider alternative strategies to achieve desired returns, such as value-add investments or exploring secondary markets where cap rates remain more favorable.

Financing Environment & DSCR Analysis

In March 2026, the prevailing interest rates continue to exert a significant influence on the debt service coverage ratios (DSCR) for real estate investments. With mortgage rates hovering around 6.5%, higher than the historical average, the cost of borrowing has increased, thereby impacting the DSCR calculation. Specifically, a higher interest rate elevates the debt service, reducing the DSCR unless counterbalanced by increased rental income. For instance, on a $1 million property with an annual net operating income (NOI) of $75,000 and annual debt service of $60,000, the DSCR is 1.25x. However, if the interest rate rise pushes the debt service to $70,000, the DSCR falls to 1.07x, reflecting a less favorable investment condition.

In the current financing environment, lenders typically require a minimum DSCR of 1.25x for approval, with many preferring 1.35x to mitigate risk exposure. This threshold ensures that the property generates sufficient income to cover debt obligations comfortably, providing a buffer against market fluctuations. The higher threshold is increasingly common due to economic uncertainties and the need for lenders to safeguard their investments. Consequently, investors must carefully evaluate rental income streams and operational expenses to meet these requirements. For example, for a property with a $100,000 annual debt service, the NOI must be at least $135,000 to meet the 1.35x criteria, a condition that might necessitate rent increases or cost reductions to achieve.

The increase in interest rates also has direct cash flow implications for rental properties. Higher debt payments reduce the cash flow available for reinvestment, maintenance, or distributions to investors. Consider a scenario where an investor owns a multifamily property generating an NOI of $150,000. With a previous debt service of $100,000, the DSCR was 1.5x. However, as rates increase, the debt service requirement rises to $120,000, reducing the DSCR to 1.25x and the cash flow from $50,000 to $30,000 annually. This reduction in free cash flow can pressure property owners to either increase rental rates or optimize operational efficiencies to maintain profitability.

In the current market, hard money and bridge loans command significant rate premiums, often exceeding conventional loan rates by 300 to 500 basis points. These loans, typically used for short-term financing needs or transitional properties, come with interest rates ranging from 9% to 12%. The premium reflects the higher risk and shorter term associated with these financial products. Investors utilizing these loans must be acutely aware of the increased debt service cost and its impact on cash flows and DSCR. For example, if an investor uses a bridge loan at 10% interest for a $500,000 loan amount, the annual debt service could reach $50,000, requiring an NOI of $62,500 to meet a 1.25x DSCR.

Given the interest rate environment, refinancing strategies often involve careful timing. The decision to refinance or hold a property hinges on anticipated rate movements and the potential for improved cash flows. A hold strategy might be advisable if rates are expected to decrease, allowing investors to capitalize on lower future refinancing costs. Conversely, if rates are predicted to rise further, refinancing sooner might secure a more favorable rate. Evaluating these strategies requires a thorough understanding of market trends and forecasts.

Finally, the current rate environment significantly impacts acquisition criteria and underwriting standards. Investors must adapt to stricter underwriting to ensure properties meet higher DSCR thresholds. This often means focusing on properties with strong cash flow potential, robust tenant demand, and opportunities for value-add improvements. Underwriting now involves more stringent stress testing of interest rates and cash flow scenarios to safeguard against adverse financial conditions. In essence, investors need to be more selective and strategic, favoring properties that can withstand the pressures of elevated financing costs.

Investment Strategy & Risk Management

In today’s dynamic real estate market, understanding the intricacies of market timing and opportunity identification is crucial for investors. As we stand in March 2026, the market presents both challenges and opportunities. For those in the fix-and-flip segment, timing is everything. The ability to identify undervalued properties with the potential for quick appreciation is key. Investors should focus on areas with strong demographic trends and economic growth, which can lead to faster turnover and higher profit margins. By closely monitoring local market conditions, investors can better anticipate shifts and capitalize on emerging trends.

Navigating the current environment requires a keen awareness of risk factors and strategic mitigation. Interest rates remain volatile, influencing borrowing costs and investor returns. To mitigate interest rate risk, investors should consider locking in rates when possible and using adjustable-rate financing cautiously. In addition, supply chain disruptions and labor shortages continue to affect renovation timelines and costs. Building a network of reliable contractors and suppliers can help minimize these risks. Furthermore, maintaining a robust contingency plan that includes financial reserves can provide a buffer against unexpected expenses and delays.

Adjusting acquisition criteria and underwriting standards is paramount in this environment. With fluctuating economic conditions, it is essential to stress-test assumptions and adopt conservative projections. Investors should focus on properties that offer the potential for both immediate cash flow and long-term appreciation. This dual focus can help balance risk and reward. Ensuring that underwriting standards reflect current market realities, such as higher construction costs and potential rent fluctuations, is essential for sustainable success.

In summary, the current real estate landscape requires a proactive and informed approach. By emphasizing strategic acquisition, risk management, and conservative underwriting, investors can navigate the complexities of today’s market with confidence. Prime Property Funding is committed to supporting investors in achieving their goals through tailored financing solutions and expert insights.

Key Considerations for Investors

- Fix-and-flip strategies: Target properties with a minimum 20% gross margin to account for holding costs and market fluctuations.

- Holding costs: Keep reserves equal to at least 6 months of projected expenses to cushion against market delays.

- Spread risk: Diversify flip projects across multiple neighborhoods to mitigate localized downturns.

- Buy-and-hold tactics: Aim for a cap rate of at least 6% to ensure adequate cash flow in a fluctuating market.

- Rent growth assumptions: Project conservative rent increases of 2-3% annually to align with economic conditions.

- Bridge financing: Structure draw schedules to align with project milestones, mitigating interest expenses.

- Rate environment: Consider fixed-rate loans to lock in current rates and protect against future hikes.

- Geographic focus: Prioritize markets with population growth above 1.5% annually for better long-term returns.

- Conservative underwriting: Stress test financial models with a 5% vacancy rate to ensure viability.

- Risk mitigation: Maintain insurance coverage that includes natural disaster protection, reflecting increasing climate risks.

By adopting these strategies, investors can position themselves for success, leveraging Prime Property Funding’s expertise to navigate the evolving real estate market with confidence and foresight.

Resources

External References

Disclaimer: This market analysis is for informational purposes only and should not be considered financial or investment advice. Market conditions can change rapidly. Consult with a qualified financial or lending professional before making any decisions.