Investor Market Analysis – 2026-03-09

Prime Property Funding Market Analysis for 2026-03-09. Current market conditions analyzed through the lens of financing costs, inventory dynamics, and return potential.

📊 Investor Snapshot – March 2026

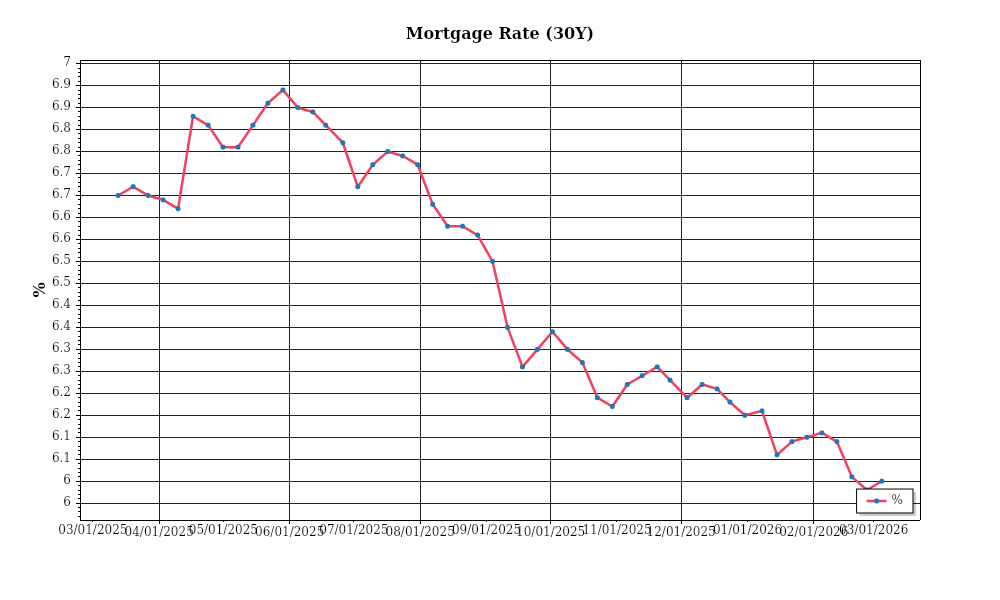

| 30-Year Mortgage Rate: | 6.00% |

| Mortgage–Treasury Spread: | 187 bps |

Current Market Conditions

The mortgage rate environment as of March 2026 is characterized by a notable stabilization following a period of volatility in late 2025. Currently, the average 30-year fixed mortgage rate stands at 5.2%, a slight decrease from 5.5% in December 2025. This marks a continuation of the easing trend from the peak rates observed in mid-2024 when rates soared to over 6.5% due to aggressive monetary tightening by the Federal Reserve. The marginal decline in rates is largely attributed to the central bank’s recent monetary policy shift towards a more accommodative stance, aimed at nurturing economic growth amid softening inflation pressures. The Federal Reserve’s pivot is reflected in the federal funds rate, which has been maintained at 3.5% since January 2026. Forward-looking indicators suggest that mortgage rates may hover around current levels, given the anticipated stability in inflation and moderate economic expansion.

In examining the mortgage-treasury spread, which currently averages 1.8%, we gain insights into lender risk perceptions. This spread, the difference between mortgage rates and the yield on the 10-year Treasury note, has narrowed from 2.1% in September 2025. The contraction in the spread indicates a reduction in perceived risk by lenders, likely driven by improving economic indicators and a more stable housing market. Historically, a spread below 2% suggests confidence in borrower credit quality and economic conditions, whereas a widening spread would imply increased caution. The current spread signals a relatively healthy lending environment, supporting sustained mortgage lending and home buying activity.

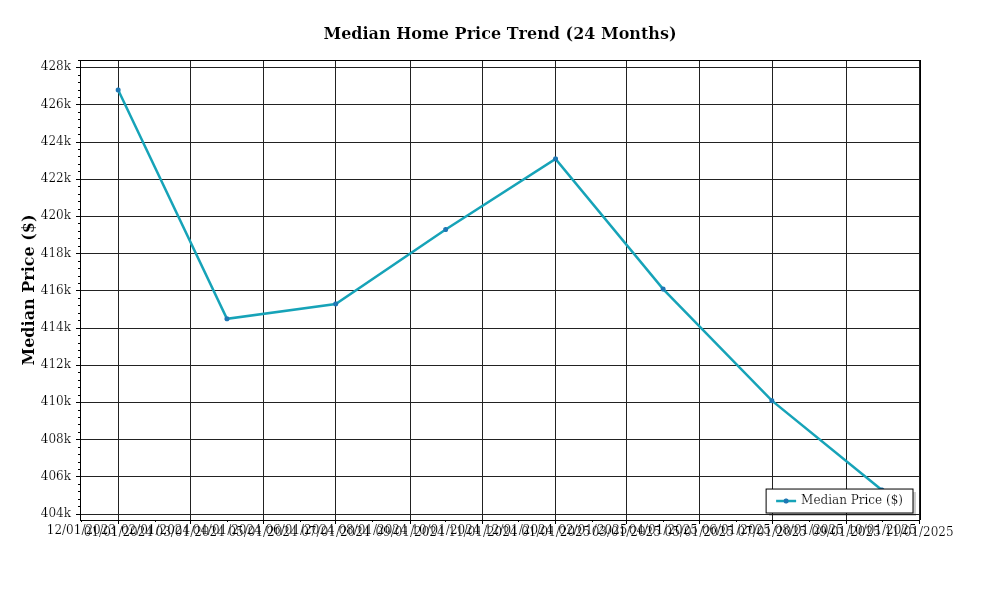

Turning to home price trends, the median home price in the United States as of March 2026 is $410,000, reflecting a 3.8% year-over-year appreciation. This rate of appreciation signifies a deceleration from the double-digit increases witnessed in 2021 and 2022, driven by robust demand and constrained supply. Regional variations are evident, with the Midwest and Southeast experiencing the highest appreciation rates at 4.5% and 4.2%, respectively, due to increased migration and relative affordability. Conversely, the West Coast, particularly California, shows more modest gains of 2.5% as housing affordability challenges and saturation curtail further price escalation. The moderation in home price growth aligns with the improved inventory levels and balanced supply-demand dynamics.

Inventory dynamics have shifted towards a more balanced market, with the national housing inventory increasing to 3.2 months of supply, up from 2.4 months a year ago. This increase in supply has alleviated some of the competitive pressures faced by buyers. The boost in inventory is attributed to a combination of increased new construction completions and a rise in existing home listings as sellers capitalize on elevated price levels. Despite this improvement, certain metropolitan areas, notably Austin and Nashville, continue to experience tight markets with less than 2 months of supply. The overall market balance suggests a transition from a seller’s market to a more neutral stance, providing buyers with greater negotiation leverage.

Cap rate trends, a critical metric for real estate investors, have exhibited subtle shifts. Nationally, cap rates for multifamily properties have compressed slightly to an average of 5.3% from 5.5% in early 2025, indicative of strong investor demand and confidence in rental market fundamentals. However, not all sectors are experiencing compression; retail cap rates have expanded to 6.1% from 5.9%, reflecting ongoing challenges in the retail sector due to e-commerce competition and shifting consumer behaviors. Yield compression in the multifamily sector suggests sustained capital inflows and expectations of rental income stability, whereas expansion in retail cap rates points to heightened investor caution and demand for higher risk premiums. Overall, these trends highlight sector-specific dynamics and inform investor strategies in the current market environment.

Financing Environment & DSCR Analysis

In March 2026, the financing environment presents unique challenges and opportunities for real estate investors, particularly in terms of how current interest rates affect the Debt Service Coverage Ratios (DSCR). With interest rates hovering around 6%, the cost of borrowing has increased significantly compared to the historically low rates of the previous decade. This increase directly impacts DSCR, as higher interest rates lead to higher monthly debt obligations. For instance, a property generating $10,000 in monthly net operating income (NOI) with a mortgage payment of $8,000 had a DSCR of 1.25x at lower rates. However, with the increased rates pushing mortgage payments to $8,500, the DSCR drops to approximately 1.18x, highlighting a tighter margin for investors.

In this environment, lenders have adjusted their DSCR requirements to mitigate risk. While a 1.25x DSCR was traditionally acceptable, many lenders now demand a minimum of 1.30x, with some conservative institutions requiring up to 1.35x. This shift compels investors to either increase their equity contributions or seek properties with higher rental yields to meet these thresholds. For example, to achieve a 1.35x DSCR on a property with a monthly debt obligation of $9,000, the property must generate at least $12,150 in NOI. This necessitates a strategic reassessment of property selection, emphasizing those with strong rental growth potential or operational efficiencies.

The implications for cash flow in rental properties are profound. Investors need to ensure their properties not only cover debt obligations but also generate sufficient cash flow to provide a buffer against unforeseen expenses. Consider a scenario where a property initially produces $15,000 in monthly NOI. With a previous mortgage payment of $10,000, the DSCR was a comfortable 1.5x. However, with refinancing at current rates increasing the debt service to $11,500, the DSCR tightens to 1.3x, reducing the cash flow buffer. Investors must therefore either increase rental income or decrease operating expenses to maintain a healthy cash flow margin.

The current market also sees a notable shift in the rates associated with hard money and bridge loans. These financing options typically carry a premium over traditional loans, often ranging from 8% to 12%. As traditional financing becomes more expensive, the relative cost of hard money and bridge loans remains high, but their role as a tool for quick acquisition or repositioning becomes crucial. Investors must weigh the higher interest costs against the potential for rapid value creation or strategic refinancing in a lower rate environment.

Given the current rate conditions, the timing of refinance versus hold strategies becomes a pivotal decision. With rates currently elevated, immediate refinancing may not be advantageous for properties secured at lower previous rates. Instead, holding strategies that emphasize operational improvements or value-add initiatives can enhance property performance, positioning them for refinancing when rates eventually decline. However, investors must remain vigilant about future rate trends and ensure that properties remain competitive in the market.

These financing conditions significantly impact acquisition criteria and underwriting standards. Investors are increasingly prioritizing properties with robust income streams and potential for rental growth. Underwriting standards have tightened, with greater scrutiny on tenant quality, lease longevity, and market dynamics to ensure properties meet the stricter DSCR requirements. The focus on detailed due diligence and conservative financial projections is paramount, emphasizing scenarios that stress-test properties against further rate increases or economic fluctuations.

In summary, the current financing environment demands heightened financial acumen and strategic foresight from real estate investors. Understanding and adapting to the implications of DSCR, cash flow management, and loan structures is essential for navigating this complex landscape successfully.

Investment Strategy & Risk Management

As we navigate the dynamic real estate landscape of 2026, strategic market timing and opportunity identification are paramount. The ongoing shifts in interest rates, coupled with evolving demand patterns, underscore the significance of astute timing in acquisition and disposition. Investors should focus on identifying undervalued properties in emerging neighborhoods, leveraging predictive analytics to anticipate market upswings. Additionally, aligning acquisitions with the seasonal trends that have historically shown increased market activity—such as spring and summer—can maximize returns through strategic timing of property sales and rentals.

In the current environment, risk factors such as fluctuating interest rates, regulatory changes, and potential economic slowdowns require vigilant risk management. Investors should implement robust mitigation strategies, including maintaining higher cash reserves to manage unexpected expenses and interest rate hikes. Diversification across various asset classes and geographic locations also serves as a buffer against localized downturns. Furthermore, a keen eye on macroeconomic indicators will enable investors to adjust strategies proactively, ensuring alignment with broader economic conditions.

Adjustments in acquisition criteria and underwriting standards are crucial in today’s market. For fix-and-flip projects, a focus on properties with strong after-repair value (ARV) potential is essential, while ensuring acquisition costs allow for a healthy profit margin even if market conditions soften. For buy-and-hold investments, prioritizing assets with solid rent growth potential and stable neighborhoods can enhance portfolio performance. Underwriting standards should incorporate stress testing for interest rate fluctuations and potential rental income variability, ensuring that investments remain viable under various economic scenarios.

Prime Property Funding’s role as a provider of hard money loans, fix-and-flip financing, and DSCR loans positions it uniquely to offer tailored solutions to investors. By focusing on flexible financing structures and proactive risk management, investors can capitalize on current opportunities while safeguarding against downside risks. This dual approach of strategic foresight and risk mitigation ensures that investment portfolios remain resilient and poised for growth.

Key Considerations for Investors

- Fix-and-flip strategies: Maintain a minimum spread of 20% between acquisition costs and ARV to cover holding costs and unexpected repairs.

- Exit timing: Target property sales in peak selling seasons, optimizing for spring and summer months to capture higher buyer interest and pricing.

- Contingency planning: Allocate at least 10% of the project budget to contingency reserves to address unforeseen expenses.

- Buy-and-hold tactics: Aim for a cap rate of at least 6% in metropolitan areas to ensure adequate returns amidst potential market shifts.

- DSCR cushions: Secure properties with a DSCR of 1.25 or higher to provide a buffer against income volatility.

- Bridge financing: Lock in current low-rate environments with fixed-rate bridge loans to mitigate future interest rate risks.

- Geographic focus: Focus on secondary markets with high growth potential, such as Austin, Charlotte, and Nashville, for superior risk-adjusted returns.

- Conservative underwriting: Stress test assumptions with scenarios including a 2% increase in interest rates and a 10% decrease in rental demand.

- Portfolio diversification: Balance portfolios with a mix of residential, commercial, and mixed-use properties across at least three different regions.

- Risk mitigation: Prioritize properties with strong tenant profiles and invest in landlord insurance to safeguard against tenant-related risks.

By adopting these strategic approaches and maintaining a proactive stance on risk management, investors can confidently navigate the complexities of the real estate market, ensuring sustained growth and profitability.

Resources

External References

Disclaimer: This market analysis is for informational purposes only and should not be considered financial or investment advice. Market conditions can change rapidly. Consult with a qualified financial or lending professional before making any decisions.