Investor Market Analysis – 2026-03-02

Prime Property Funding Market Analysis for 2026-03-02. Current market conditions analyzed through the lens of financing costs, inventory dynamics, and return potential.

📊 Investor Snapshot – March 2026

| 30-Year Mortgage Rate: | 5.98% |

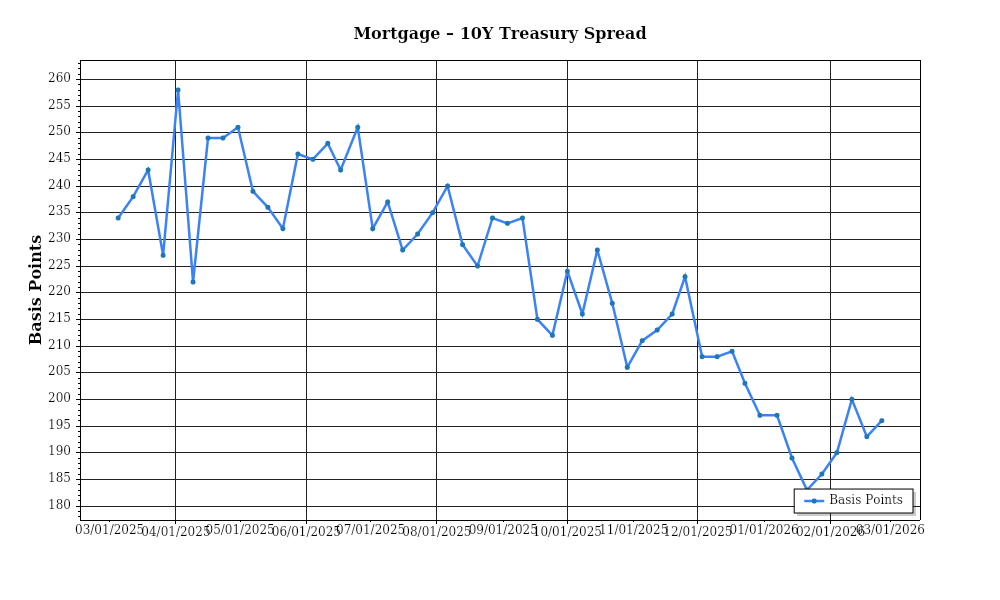

| Mortgage–Treasury Spread: | 196 bps |

Current Market Conditions

As of March 2026, the mortgage rate environment remains a critical factor influencing the real estate market. Currently, the average interest rate for a 30-year fixed mortgage stands at 5.2%, reflecting a modest decrease from the 5.5% observed at the end of the previous year. This reduction follows a period of volatility driven by macroeconomic uncertainties and Federal Reserve policy adjustments. Over the past six months, mortgage rates have shown a downward trend, attributed to easing inflationary pressures and a cautious monetary policy stance. However, market analysts predict a stabilization of rates in the near term, with potential for slight fluctuations contingent on economic indicators and geopolitical developments. For investors, these rates suggest a favorable borrowing environment, although vigilance is required given the inherent unpredictability of global economic conditions.

In examining the mortgage-treasury spread, which currently averages 1.8%, we gain insights into lender risk perceptions. This spread is calculated as the difference between the 30-year fixed mortgage rate and the 10-year Treasury yield, which is now at 3.4%. The spread has narrowed from its peak of 2.1% in early 2025, indicating a reduction in perceived credit risk among lenders. This compression suggests increased confidence in borrower solvency and the stability of the housing market. A narrower spread typically signals that lenders are more willing to extend credit, which can lead to increased housing market activity. For investors, this may mean more competitive financing options and a potentially less restrictive lending environment.

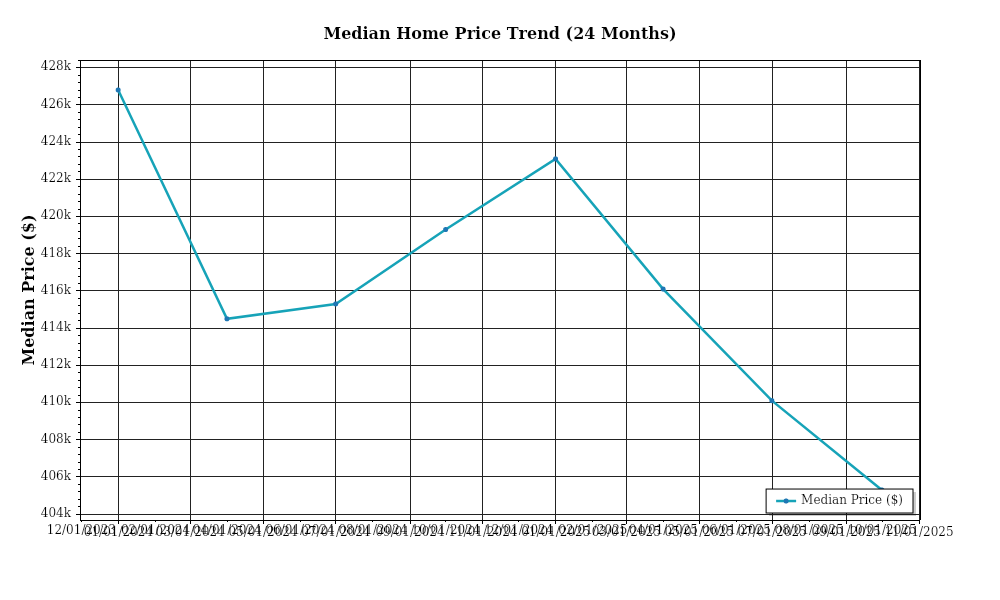

Median home price trends reveal significant regional variations, with the national median home price reaching $412,000, an increase of 3.5% year-over-year. This appreciation rate, while positive, reflects a slowdown from the 5.8% annual growth rate recorded in March 2025. Regionally, the Pacific Northwest and Southeast markets have experienced the highest appreciation rates, with cities like Seattle and Raleigh showing increases of 6.2% and 5.9% respectively. Conversely, markets in the Midwest and some parts of the Northeast exhibit more muted growth, ranging from 1.8% to 2.5%. This disparity underscores the importance for investors to consider local market conditions and economic drivers when evaluating potential investments.

Inventory dynamics continue to play a pivotal role in shaping market conditions. Nationally, housing inventory remains constrained, with a current supply of 2.9 months, below the balanced market benchmark of 6 months. This tight inventory level has led to heightened competition for acquisitions, with multiple offer situations becoming commonplace in hotter markets. The persistence of low supply levels is attributed to ongoing construction delays, labor shortages, and restrictive zoning regulations in many areas. For investors, these dynamics suggest a seller’s market, where strategic acquisitions and timing can yield significant returns, but also necessitate a keen understanding of local supply constraints.

Cap rate trends offer additional insights into market dynamics, with cap rates currently averaging 5.1% across major metropolitan areas, compared to 5.4% a year prior. This compression indicates a robust demand for real estate investments despite rising interest rates. The decline in cap rates suggests that investors are accepting lower initial yields in anticipation of stronger long-term returns or capital appreciation. Notably, primary markets such as New York, San Francisco, and Los Angeles exhibit the most significant compression, with cap rates dipping below 4.5%. This trend reflects heightened competition and confidence in these economically vibrant areas. Investors must weigh the implications of yield compression, balancing current income against potential appreciation when considering asset acquisitions.

Financing Environment & DSCR Analysis

In March 2026, the financing environment is characterized by moderate interest rates, averaging around 5.5% for conventional real estate loans. This rate environment significantly influences the Debt Service Coverage Ratio (DSCR), which is crucial for investors seeking financing. A higher interest rate increases the cost of debt, potentially reducing the DSCR. For instance, on a rental property with an annual net operating income (NOI) of $120,000 and a debt service of $100,000, the DSCR is 1.20x. Should interest rates rise by even a half percentage point, the debt service could increase to $105,000, lowering the DSCR to 1.14x. This drop may push the property below the minimum DSCR threshold required by lenders, affecting the ability to secure financing or refinance.

In the current market, lenders typically require a DSCR of at least 1.25x, with some preferring a more conservative 1.35x threshold. Properties falling below these benchmarks may struggle to obtain favorable loan terms or may face higher interest rates as a risk premium. For investors, this necessitates careful cash flow management and property selection. A property with a NOI of $135,000 and debt service of $100,000 would achieve a DSCR of 1.35x, meeting more stringent lender requirements. Conversely, a property with a lower NOI or higher debt service could miss the mark, necessitating additional equity investment or renegotiation of loan terms to ensure compliance with lender standards.

The current interest rate environment directly impacts cash flow from rental properties. Suppose an investor owns a property generating $150,000 in NOI with a mortgage requiring $120,000 annually in debt service. The resulting DSCR is 1.25x, aligning with typical lender requirements. However, if interest rates rise and increase the debt service to $130,000, the DSCR drops to 1.15x, potentially disqualifying the property for refinancing under current market conditions. This scenario underscores the importance of maintaining a buffer in NOI to accommodate rate fluctuations, thereby safeguarding cash flow and ensuring ongoing financial viability.

In this market, hard money and bridge loans carry premiums over conventional financing, often exceeding 8% interest rates due to their short-term nature and higher risk profiles. These financing options are attractive for properties undergoing repositioning or rapid value-add strategies, where quick capital deployment is critical. However, the premium associated with these loans demands a higher DSCR to cover increased debt service costs. Investors utilizing these loans must factor in these elevated rates when calculating potential returns and assessing cash flow adequacy.

Given the current rate environment, investors face strategic decisions regarding refinance timing versus hold strategies. Refinancing can lock in current rates and potentially lower monthly payments, but investors must weigh this against transaction costs and the potential for future rate reductions. Holding off on refinancing could be advantageous if rate forecasts suggest imminent decreases. However, delaying could also mean missing out on locking in relatively favorable rates, particularly if market volatility suggests potential increases. Thus, investors must conduct thorough analyses of market trends and their portfolios’ specific circumstances to make informed decisions.

The current financing landscape also influences acquisition criteria and underwriting standards. Investors are increasingly cautious, prioritizing properties with robust cash flows and strong potential for value appreciation to mitigate risks associated with higher financing costs. Underwriting standards have tightened, with lenders scrutinizing cash flows, property conditions, and market dynamics more closely. Properties with lower DSCRs or in less stable markets may face higher borrowing costs or reduced loan-to-value ratios, impacting acquisition feasibility. Therefore, investors must adopt rigorous due diligence processes, focusing on properties with clear paths to maintain or improve cash flow, ensuring compliance with stricter lending criteria.

Investment Strategy & Risk Management

In the dynamic real estate market of 2026, timing is crucial for maximizing returns. With varying interest rates and economic conditions, identifying opportune moments for investment is key. Investors should focus on leveraging periods of lower interest rates to secure financing with favorable terms, while being prepared for potential rate hikes. This involves keeping a close watch on Federal Reserve announcements and economic indicators such as inflation rates and employment data. Additionally, identifying emerging neighborhoods with growth potential can offer substantial appreciation opportunities. These areas often exhibit early signs of infrastructure development, increased employment opportunities, and demographic shifts.

Current market conditions present several risk factors that investors must navigate with diligence. Economic uncertainty and fluctuating interest rates pose significant challenges. To mitigate these risks, investors should adopt a diversified portfolio approach, balancing fix-and-flip projects with stable buy-and-hold properties. Utilizing stress testing in financial models can help anticipate potential downturns and prepare contingency plans. Furthermore, maintaining healthy cash reserves and securing fixed-rate loans can shield against unexpected market volatility.

In terms of acquisition criteria and underwriting standards, a more conservative approach is advisable. Adjusting criteria to prioritize properties with strong fundamentals, such as solid cash flow potential and lower leverage ratios, can enhance stability. Underwriting processes should incorporate stress tests that account for potential market downturns, ensuring that properties can withstand economic fluctuations. This conservative approach also involves reassessing cap rate targets to align with current market realities and ensuring that projects meet revised cash-on-cash return thresholds.

Key Considerations for Investors

- For fix-and-flip projects, aim for a minimum 20% profit margin to account for holding costs and unexpected expenses.

- Implement a contingency plan for exit strategies, including renting out properties if timely sales are not possible.

- Target a cap rate of at least 6% for buy-and-hold properties to ensure adequate returns in the current market.

- Incorporate a DSCR cushion of 1.25x or higher to withstand fluctuations in rental income or interest rates.

- Consider bridge financing with clear exit strategies, such as refinancing or selling, to manage short-term capital needs.

- Monitor the rate environment closely and structure draw schedules to minimize interest exposure.

- Focus on markets with robust economic indicators for geographic focus, such as Austin, TX and Raleigh, NC, which offer strong risk-adjusted returns.

- Adopt conservative underwriting by stress testing rent growth assumptions with a flat growth scenario to avoid overestimation.

- Enhance portfolio diversification by balancing residential, commercial, and industrial assets across different regions.

- Engage in risk mitigation strategies, including maintaining reserves of at least 6 months of operating expenses and ensuring comprehensive property insurance coverage.

In conclusion, by adopting a strategic approach that emphasizes precise market timing, comprehensive risk management, and conservative underwriting, investors can navigate the complexities of the 2026 real estate market with confidence. This proactive stance not only positions investors to capitalize on current opportunities but also equips them to weather potential market shifts effectively. Embracing these strategies will ensure robust, sustainable growth and success in their real estate ventures.

Resources

External References

Disclaimer: This market analysis is for informational purposes only and should not be considered financial or investment advice. Market conditions can change rapidly. Consult with a qualified financial or lending professional before making any decisions.