Prime Property Funding Market Analysis for 2026-02-28. Current market conditions analyzed through the lens of financing costs, inventory dynamics, and return potential.

📊 Investor Snapshot – February 2026

| 30-Year Mortgage Rate: | 5.98% |

| Mortgage–Treasury Spread: | 196 bps |

Current Market Conditions

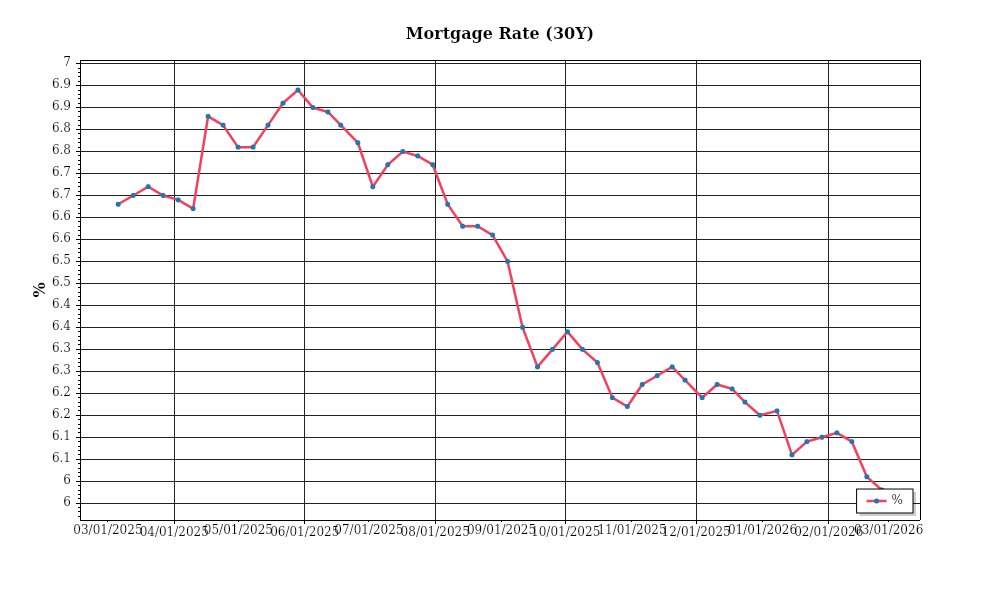

As of February 2026, the mortgage rate environment remains a pivotal driver of the real estate market. The average 30-year fixed mortgage rate currently stands at 5.75%, reflecting a slight decrease from the 6.00% mark observed in late 2025. This decrease aligns with the broader economic adjustments following the Federal Reserve’s decision to maintain interest rates steady since their last hike in December 2025. Over the past year, mortgage rates have fluctuated between 5.5% and 6.5%, indicating a relatively stable environment compared to the volatility experienced during the post-pandemic recovery phase. The trajectory of mortgage rates suggests a cautious optimism among lenders, as inflation pressures have shown signs of easing, potentially leading to more favorable borrowing conditions over the medium term.

The mortgage-treasury spread, which compares mortgage rates to the yield on 10-year Treasury bonds, provides insights into lender risk perception. As of February 2026, this spread is approximately 180 basis points, slightly above the historical average of 150 basis points. This wider spread indicates that lenders are pricing in a moderate level of risk, likely due to ongoing economic uncertainties, including geopolitical tensions and potential shifts in fiscal policy. The spread has narrowed from a peak of 220 basis points in mid-2025, suggesting that while lenders remain cautious, their risk assessments have improved somewhat. This spread is a critical indicator, as it reflects the balance between mortgage lending risk and the relative safety of treasury investments. A sustained narrowing of this spread could signal increased confidence among lenders, potentially leading to more competitive mortgage offerings.

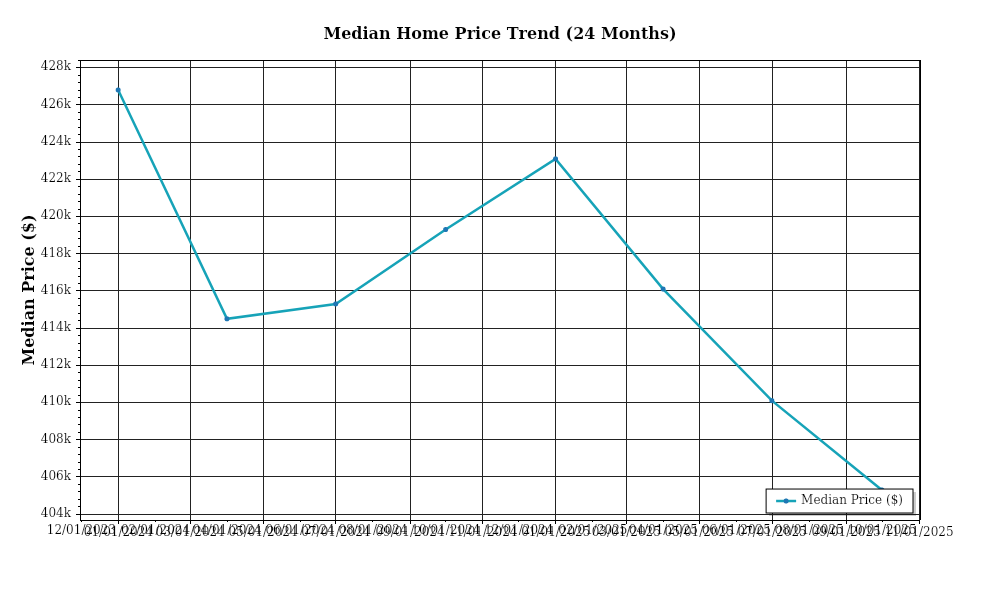

Median home prices continue to be a topic of significant interest. Nationally, the median home price is currently at $430,000, marking an annual appreciation rate of 4.2%, which is a deceleration from the 6.5% rate noted in 2025. Regional variations are pronounced, with the West Coast experiencing the highest median prices, around $680,000, driven by robust demand and limited supply. In contrast, the Midwest maintains more affordable levels, with median prices averaging $280,000. This regional disparity is largely attributed to differences in economic growth, employment opportunities, and housing supply constraints. The slowing appreciation rate signals a more balanced market, as increased construction activity in some regions has begun to address supply shortages.

Inventory dynamics remain a critical factor in assessing current market conditions. The national housing supply is currently at 4.1 months, indicating a slight shift towards a more balanced market compared to the 3.5 months supply seen a year ago. This increase in inventory levels is primarily due to new construction projects reaching completion and a moderate rise in existing homeowners listing properties. Despite this improvement, certain urban centers, particularly in the South and Southwest, continue to experience competitive acquisition environments with supply levels below 3 months. The market balance is gradually improving, which may ease upward pressure on prices if the trend continues.

Cap rate trends are essential for understanding the investment landscape in real estate. As of February 2026, average cap rates for prime commercial real estate are around 5.2%, reflecting a slight expansion from the 4.8% observed in early 2025. This expansion suggests a mild yield compression, as investors demand higher returns in response to potential economic uncertainties and rising interest rates. The increase in cap rates indicates that property values may not be appreciating as rapidly, potentially offering more attractive entry points for investors seeking to balance risk and return. However, cap rate trends vary significantly by sector, with industrial properties maintaining lower cap rates due to strong demand, while retail spaces are seeing higher cap rates as they adjust to shifting consumer behaviors and e-commerce growth.

These current market conditions provide a comprehensive snapshot of the real estate landscape, highlighting both challenges and opportunities for investors. Each metric offers valuable insights into the underlying dynamics influencing property values, financing conditions, and investment strategies.

Financing Environment & DSCR Analysis

In February 2026, the financing environment for real estate investment remains shaped by the prevailing interest rates, which significantly affect the Debt Service Coverage Ratios (DSCR) that investors can achieve. Current interest rates have settled at around 5.5% for conventional loans, reflecting a moderate increase from previous years. This rise in rates directly impacts the cost of borrowing and, consequently, the DSCR for investment properties. With higher interest rates, the debt service—the regular payments necessary to cover the interest and principal of a loan—increases, thereby placing pressure on achieving favorable DSCRs. Investors find that maintaining a DSCR above the typical 1.25x threshold has become more challenging, as the increased cost of borrowing reduces the net cash flow available to cover debt obligations.

The industry standard for DSCR requirements typically ranges between 1.25x and 1.35x, with lenders leaning towards the higher end of this spectrum in the current market. This shift is largely a response to the increased risk associated with higher interest rates. Lenders are more cautious, requiring stricter underwriting to ensure that borrowers can comfortably service their debts. A DSCR of 1.35x means that the property must generate income that is 35% higher than the debt obligations, providing a buffer against potential income fluctuations or unforeseen expenses. This higher threshold ensures that properties are more resilient to financial stress, but it also narrows the pool of eligible properties that can meet these criteria, potentially limiting investment opportunities.

For rental properties, this environment necessitates a closer examination of cash flow and profitability. Consider a property with an annual net operating income (NOI) of $150,000 and a debt service of $120,000, resulting in a DSCR of 1.25x. If interest rates increase the debt service to $130,000, the DSCR drops to 1.15x, which is below the acceptable threshold for many lenders. This scenario illustrates the importance of accurate forecasting and financial planning. Investors must ensure that rental income not only covers the increased debt service but also provides a sufficient return on investment. This may involve adjusting rental rates, seeking properties with higher income potential, or even reconsidering the leverage used in financing.

In the realm of hard money and bridge loans, rate premiums are more pronounced. These short-term financing options have seen rates climb to between 8% and 12%, reflecting the increased risk lenders associate with these products. Investors using hard money loans to acquire or renovate properties must be acutely aware of the cost implications and the impact on overall project viability. The steep rate premiums necessitate quick value-add strategies or rapid refinancing into more favorable long-term loans to mitigate financial strain.

Given the current rate environment, investors face strategic decisions regarding refinance timing versus hold strategies. With interest rates expected to stabilize or potentially decrease slightly in the coming years, some investors may choose to hold off on refinancing, waiting for more favorable conditions. However, this strategy carries the risk of continued rate increases, which could further erode cash flow. Conversely, refinancing now locks in current rates, providing stability but potentially at a higher cost than future rates might offer. The decision is contingent upon the investor’s risk tolerance, cash flow needs, and long-term investment goals.

The impact on acquisition criteria and underwriting standards is palpable, as investors and lenders both adjust to the evolving landscape. There is an increased emphasis on conservative financial projections and thorough due diligence. Properties must not only meet the higher DSCR thresholds but also offer robust income potential to justify the investment. Underwriting standards have tightened, with lenders scrutinizing income stability, market conditions, and borrower experience more closely than ever before. This cautious approach aims to mitigate risks associated with the current interest rate environment, ensuring that investments remain viable and profitable in a potentially volatile market.

Investment Strategy & Risk Management

As we navigate through 2026, market timing and opportunity identification remain pivotal for investors in real estate, particularly in the context of the services provided by Prime Property Funding. Given current economic indicators, such as interest rates and inflation forecasts, timing your market entry and exit can significantly impact your investment returns. Identifying opportunities involves a strategic focus on markets that demonstrate resilience and potential for growth. For instance, secondary and tertiary markets with robust employment growth and infrastructure development offer promising prospects. Investors should also monitor interest rate fluctuations closely, as they directly influence acquisition costs and financing structures.

The current environment presents several risk factors, including economic instability and fluctuating property values. To mitigate these risks, investors should adopt a multi-faceted approach. Diversification across different asset classes and geographic locations can help balance exposure and reduce volatility. Furthermore, incorporating stress testing into your underwriting standards will enable you to better anticipate and withstand adverse market conditions. This includes modeling various economic scenarios to assess potential impacts on cash flow and returns. By doing so, you can develop contingency plans that include liquidity reserves and alternative exit strategies, ensuring that your investments remain viable even in downturns.

Adjusting acquisition criteria and underwriting standards is crucial in today’s dynamic market. A more conservative approach that emphasizes solid fundamentals over speculative growth is advisable. Investors should prioritize properties with strong cash flow potential and reasonable cap rates. Additionally, maintaining a cushion in your Debt Service Coverage Ratio (DSCR) will provide a safety net against potential income disruptions. Given the increased cost of capital, it is also essential to scrutinize the cost and structure of financing. Bridge loans and other short-term financing options should be carefully evaluated for their rate environment and flexibility in draw schedules.

To effectively manage risk, investors should also focus on improving property conditions and tenant quality. Comprehensive due diligence, including property inspections and background checks on tenants, can significantly reduce the likelihood of unforeseen expenses and occupancy issues. Insurance policies that fully cover potential liabilities and damages are also a key component of a robust risk management strategy.

Key Considerations for Investors

- For fix-and-flip strategies, aim to minimize holding costs by targeting properties that require cosmetic rather than structural upgrades, reducing renovation timelines.

- Maintain a spread risk of at least 20% between purchase and expected sale prices to accommodate market volatility.

- Implement a contingency plan for potential delays in flipping, such as securing interim rental agreements to cover holding costs.

- Target a cap rate of at least 6% for buy-and-hold investments in urban areas, adjusting higher in more volatile markets.

- Assume a conservative rent growth rate of 2-3% annually to ensure sustainable cash flow projections.

- Ensure a DSCR cushion of 1.25x-1.5x to buffer against unexpected income shortfalls.

- In the current rate environment, lock in bridge financing with fixed rates or rate caps to manage interest rate risk.

- Establish exit strategies that consider seasonal market patterns, such as selling during peak spring and summer months.

- Focus on geographic markets like the Sun Belt for better risk-adjusted returns due to population growth and economic expansion.

- Pursue portfolio diversification by balancing residential, commercial, and industrial properties to stabilize overall returns.

By leveraging these strategic insights and maintaining a proactive approach to risk management, investors can confidently navigate the complexities of the current real estate market, positioning themselves for sustainable growth and success.

Resources

External References

Disclaimer: This market analysis is for informational purposes only and should not be considered financial or investment advice. Market conditions can change rapidly. Consult with a qualified financial or lending professional before making any decisions.