Investor Market Analysis – 2026-02-27

Prime Property Funding Market Analysis for 2026-02-27. Current market conditions analyzed through the lens of financing costs, inventory dynamics, and return potential.

📊 Investor Snapshot – February 2026

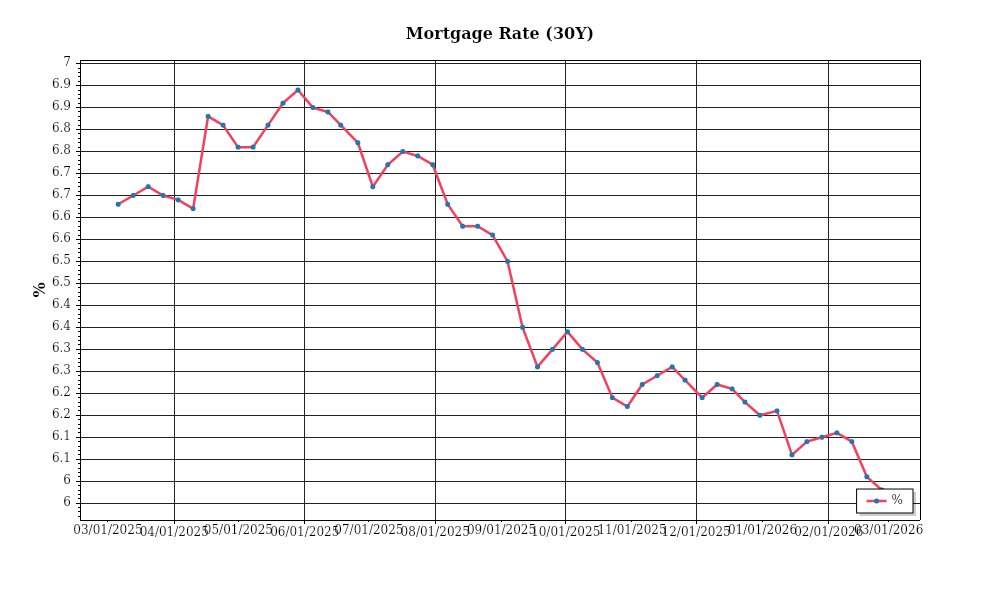

| 30-Year Mortgage Rate: | 5.98% |

| Mortgage–Treasury Spread: | 196 bps |

Current Market Conditions

As of February 2026, the mortgage rate environment is showing signs of stabilization after a period of significant fluctuation over the past year. The average 30-year fixed mortgage rate currently stands at 5.2%, reflecting a slight decrease from the 5.5% peak observed in mid-2025. Over the last six months, rates have generally hovered between 5.0% and 5.3%. This stabilization follows a year of aggressive rate hikes by central banks in response to post-pandemic inflation pressures. The current trajectory suggests a cautious optimism among lenders, as inflationary concerns have somewhat eased with central banks signaling a pause in further rate increases. In practical terms, these rates impact buyers’ purchasing power and monthly payment calculations, which can influence demand in the housing market.

The mortgage-treasury spread, a key indicator of lender risk perception, provides further insight into the current market dynamics. As of February 2026, the spread between the 30-year fixed mortgage rate and the 10-year Treasury yield is approximately 200 basis points. This spread has narrowed from a high of 250 basis points in late 2024, indicating a reduction in perceived risk from lenders. Typically, a narrow spread suggests that lenders are more confident in the housing market’s stability and economic outlook. However, it remains above the pre-pandemic average of 150 basis points, reflecting lingering caution regarding economic uncertainty and potential geopolitical factors that could impact market stability.

Median home price trends reveal a diverse landscape across different regions. Nationally, the median home price is currently at $410,000, showing an annual appreciation rate of approximately 4%. This rate of growth has moderated from the double-digit increases seen during the pandemic boom but remains robust, supported by steady demand and constrained supply. Regional variations are significant, with the Sun Belt experiencing the highest growth. For instance, cities like Austin and Phoenix report appreciation rates of 6% to 7%, driven by strong job markets and migration trends. In contrast, some Northeast markets, including New York and Boston, show more modest gains of around 2%, as these areas recover from pandemic-induced population shifts.

Inventory dynamics continue to play a crucial role in shaping market conditions. Current housing supply levels are characterized by limited availability, with the national housing inventory at 3.5 months of supply, below the balanced market benchmark of 6 months. This shortage fuels competition among buyers, particularly in high-demand markets, where multiple offers and quick sales are common. The constrained supply is largely due to a slowdown in new housing starts, which have been impacted by higher construction costs and labor shortages. Consequently, the market remains tilted in favor of sellers, though the pace of price increases has moderated as demand cools with rising mortgage costs.

Cap rate trends in the commercial real estate sector indicate a period of yield compression, with the average cap rate across major metropolitan areas currently at 5.1%. This represents a decrease from the 5.5% average observed in early 2025, reflecting increased investor demand for stable, income-generating assets in a low-yield environment. The compression is particularly pronounced in sectors such as multifamily and industrial real estate, which have benefitted from strong fundamentals and investor interest. However, some expansion is noted in office and retail sectors, where uncertainty around future work patterns and consumer behavior persists. This nuanced cap rate environment suggests that investors are selectively optimistic, prioritizing sectors with favorable long-term prospects while remaining cautious in areas exposed to structural changes.

Financing Environment & DSCR Analysis

In February 2026, the financing environment is characterized by a relatively stable interest rate climate, with the Federal Reserve maintaining a cautious stance. This stability, however, has not translated into significantly lower borrowing costs for real estate investors. Current mortgage rates for investment properties hover around 6.5% to 7%, impacting the Debt Service Coverage Ratios (DSCR) that lenders require for underwriting. The prevailing rates influence the DSCR by increasing the cost of debt service, thereby necessitating higher net operating income (NOI) to meet lender requirements. With these rates, achieving a DSCR of 1.25x can be challenging, particularly for properties with marginal cash flows. This situation compels investors to ensure properties generate sufficient income to cover debt obligations comfortably, thereby making underwriting standards more stringent.

In this environment, typical DSCR requirements have shifted slightly upwards, with many lenders now favoring a DSCR threshold of 1.35x over the traditional 1.25x. This stricter requirement reflects lenders’ cautious approach to mitigate potential risks associated with economic uncertainties and inflationary pressures. For investors, meeting a 1.35x DSCR translates into a need for higher rental income or reduced expenses. For instance, a property with an annual debt service of $50,000 would need to generate at least $67,500 in NOI to meet the 1.35x DSCR requirement, compared to $62,500 for a 1.25x threshold. Such requirements can significantly influence the feasibility of new acquisitions and necessitate a careful examination of property performance metrics.

The cash flow implications for rental properties under these conditions are substantial. For example, consider a multi-family property generating $80,000 in annual rental income, with operating expenses totaling $30,000. This leaves an NOI of $50,000. With a debt service obligation of $40,000 annually, the DSCR is 1.25x. However, if the lender requires a 1.35x DSCR, the property would need an NOI of $54,000, necessitating either an increase in rents or a reduction in expenses. Such adjustments may not be feasible in all markets, especially where rent increases are regulated or market rents have plateaued. As a result, investors may need to enhance property management efficiency or explore value-add strategies to boost income.

The current market conditions have also affected the rates for hard money and bridge loans, which now come with premiums ranging from 8% to 12%. This is notably higher than traditional financing options, reflecting the increased risk associated with these short-term, high-leverage loans. These loan types remain attractive for investors pursuing quick acquisitions or property improvements before refinancing. However, the higher cost of capital requires careful consideration of the payback period and exit strategy to ensure profitability.

In terms of refinance timing versus hold strategies, the decision hinges on the interest rate outlook and property performance. Given the stable yet relatively high interest rates, refinancing may not yield significant immediate savings unless there is a substantial drop in rates. Thus, holding the current financing arrangements while focusing on improving property performance or waiting for a more favorable rate environment could be prudent. Investors must weigh potential long-term savings against immediate refinancing costs, keeping in mind that a well-timed refinance could enhance cash flow and property valuation.

Lastly, the impact of the current financing environment on acquisition criteria and underwriting standards cannot be overstated. Investors are increasingly prioritizing properties with robust cash flow and potential for value addition. Underwriting standards now emphasize conservative income projections and stress testing against interest rate fluctuations. This cautious approach helps mitigate risks and ensures that investments remain viable under varying economic conditions. As a result, properties that demonstrate resilience in cash flow and adaptability in management are likely to attract more interest and command premium valuations in today’s market.

Investment Strategy & Risk Management

In the current market landscape of February 2026, real estate investors are navigating a complex interplay of market timing and opportunity identification. Given the cyclical nature of real estate, timing the market effectively can significantly enhance profitability. With interest rates stabilizing after a period of volatility, opportunities for strategic acquisitions are emerging. Investors need to be vigilant, identifying properties undervalued due to temporary market conditions. Properties with a strong value-add potential, especially in areas showing signs of economic revitalization, present lucrative opportunities. The key is to balance immediate acquisition benefits against potential holding costs, particularly in markets experiencing seasonal fluctuations.

Risk factors in the current environment are substantial but manageable with the right strategies. Economic indicators suggest a moderate growth trajectory, but the potential for unexpected shifts in interest rates and consumer confidence remains a concern. To mitigate these risks, investors should stress-test their assumptions, particularly focusing on cash flow projections and debt service coverage ratios (DSCR). A conservative approach to underwriting is crucial, ensuring that any investment can withstand market downturns without jeopardizing returns. Building a diverse portfolio across asset classes and geographical locations can further insulate investors from localized economic shocks.

Adjusting acquisition criteria and underwriting standards is essential in today’s market. Investors should emphasize robust due diligence, including comprehensive market analyses and property inspections to assess potential risks and returns accurately. Acquisition criteria should prioritize properties that meet specific cap rate thresholds, ensuring that returns are aligned with investor expectations. Underwriting standards need to be stringent, with particular attention paid to stress-testing scenarios under various economic conditions. This approach not only safeguards against unforeseen downturns but also positions investors to capitalize on opportunities as they arise.

Prime Property Funding clients, particularly those utilizing hard money loans, fix-and-flip financing, and DSCR loans, should consider these strategies to optimize their investments. By focusing on conservative acquisition criteria, rigorous risk management, and strategic opportunity identification, investors can navigate the current market with confidence. This approach not only mitigates potential risks but also sets the stage for sustainable long-term growth in the real estate sector.

Key Considerations for Investors

- Fix-and-flip strategies: Ensure a minimum spread of 25% between purchase and sale price to cover holding costs and unforeseen expenses.

- Exit timing: Plan flips to coincide with peak selling seasons, typically spring and summer, to maximize exposure and selling price.

- Contingency planning: Allocate at least 15% of total project costs for contingencies to address unexpected repairs or market changes.

- Buy-and-hold tactics: Target properties with cap rates above 6% to ensure sufficient return on investment in both high and low-growth markets.

- DSCR cushions: Aim for a DSCR of 1.25 or higher to maintain positive cash flow and reduce default risk.

- Bridge financing: Secure fixed-rate terms when possible to protect against potential rate increases and include a minimum 6-month reserve for interest payments.

- Geographic focus: Prioritize emerging markets in the Sun Belt region, which currently offer the best risk-adjusted returns due to population growth and economic expansion.

- Conservative underwriting: Implement stress testing scenarios assuming a 10% drop in rental income to ensure portfolio resilience.

- Risk mitigation: Maintain a reserve fund equal to 3-6 months of operating expenses to cover shortfalls and unexpected vacancies.

- Portfolio diversification: Diversify across asset classes, aiming for a mix of residential, commercial, and industrial properties to balance risk and reward.

By adhering to these strategic guidelines, investors can effectively navigate the current real estate landscape, positioning themselves for success in both the short and long term. With a focus on risk management and strategic opportunity identification, investors can confidently pursue opportunities that align with their financial goals.

Resources

External References

Disclaimer: This market analysis is for informational purposes only and should not be considered financial or investment advice. Market conditions can change rapidly. Consult with a qualified financial or lending professional before making any decisions.