Investor Market Analysis – 2026-02-16

Prime Property Funding Market Analysis for 2026-02-16. Current market conditions analyzed through the lens of financing costs, inventory dynamics, and return potential.

📊 Investor Snapshot – February 2026

| 30-Year Mortgage Rate: | 6.09% |

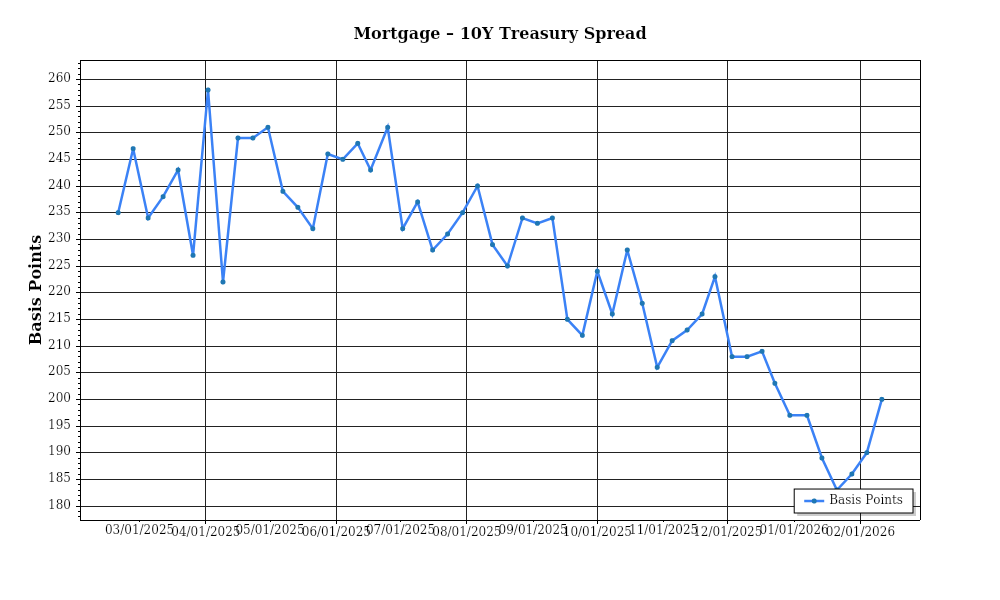

| Mortgage–Treasury Spread: | 200 bps |

Current Market Conditions

As of February 2026, the U.S. real estate market is navigating a complex landscape shaped by evolving mortgage rates, dynamic inventory levels, and shifting price trends. The ongoing adjustments in these areas offer critical insights for investors seeking to understand the current conditions and their implications for future investments.

The mortgage rate environment remains a pivotal factor influencing the housing market. Presently, the average 30-year fixed mortgage rate hovers around 5.75%, a slight decrease from the peak observed in late 2025, when rates reached 6.25%. This downward trend is largely attributed to the Federal Reserve’s recent measures aimed at stabilizing economic conditions, including incremental rate cuts to spur economic growth. However, rates remain elevated compared to the pre-pandemic norm of sub-4% levels, reflecting a cautious lending environment. The trajectory of mortgage rates suggests a stabilization phase, with forecasts indicating a gradual decline towards 5.5% by mid-2026, contingent on inflationary pressures and further monetary policy adjustments.

The mortgage-treasury spread, which is a crucial indicator of lender risk perception, currently stands at approximately 1.7%. This spread has narrowed from the 2.2% recorded in early 2025, signaling a modest reduction in risk aversion among lenders. Typically, a wider spread indicates higher perceived risk, prompting lenders to demand greater compensation for potential defaults. The current spread suggests that lenders are increasingly confident in the economic outlook, albeit cautiously, as they adjust their risk premiums. This contraction in the spread may encourage more competitive mortgage offerings, potentially easing borrowing costs for prospective homebuyers and investors.

Turning to home price trends, the national median home price is currently at $395,000, representing a year-over-year appreciation rate of 7%. This rate of growth, while robust, marks a deceleration from the double-digit increases observed during the pandemic-driven housing boom. Regional variations are evident, with markets like the Sun Belt experiencing higher appreciation rates, particularly in cities such as Austin and Phoenix, where home prices have surged by over 10% annually. Conversely, coastal markets such as San Francisco and New York City are witnessing more modest gains, reflecting affordability constraints and population shifts. These regional disparities underscore the importance of localized market analysis for investors targeting specific geographies.

Inventory dynamics continue to play a critical role in shaping the current market environment. Nationally, housing supply remains constrained, with an average of 2.8 months of inventory available, well below the balanced market benchmark of six months. This tight supply is exacerbated by sustained demand, leading to competitive acquisition processes and frequent bidding wars in many markets. However, there are signs of easing in certain regions, where new construction projects and zoning reforms are gradually increasing the housing stock. Investors should monitor these developments closely, as shifts in supply levels can impact both acquisition strategies and pricing power.

Cap rate trends provide further insight into the real estate investment landscape. The average cap rate for multifamily properties is currently at 5.2%, reflecting a slight compression from the previous year’s average of 5.5%. This compression is indicative of strong investor demand and the pursuit of yield in a low-interest-rate environment. However, the potential for further compression is tempered by macroeconomic uncertainties and the prospect of rising operational costs. Investors should remain vigilant, as cap rate dynamics can influence property valuations and investment returns, particularly in an environment where yield expansion may arise from shifts in interest rates or investor sentiment.

Overall, the current market conditions depict a nuanced picture characterized by moderating price growth, constrained inventory, and evolving financing dynamics. These elements collectively shape the investment landscape, presenting both challenges and opportunities for informed market participants.

Financing Environment & DSCR Analysis

In February 2026, the financing environment for real estate investments is experiencing substantial impact due to the prevailing interest rate conditions. Current interest rates have reached levels not seen since the early 2020s, with average mortgage rates hovering around 7.5% for standard residential properties. This increase in borrowing cost directly affects the Debt Service Coverage Ratios (DSCR), a critical metric for lenders assessing the risk of a loan. Higher interest rates mean higher monthly debt servicing costs, which in turn requires properties to generate significantly more income to meet the same DSCR thresholds. Investors must now be more diligent in ensuring that their properties yield sufficient cash flow to not only cover these increased costs but also maintain desired profit margins.

The typical DSCR requirement in the current market environment fluctuates between 1.25x and 1.35x. This range signifies the multiple of net operating income (NOI) over the debt obligations owed. For instance, a property with a DSCR of 1.25x must generate $1.25 in NOI for every $1 of debt service. Lenders tend to favor higher DSCRs in uncertain economic climates to buffer against potential fluctuations in income or increases in operating expenses. In the current climate, many lenders have shifted towards the upper end of this range, demanding a DSCR closer to 1.35x to mitigate perceived risks associated with higher interest rates and potential market volatility. This shift requires investors to conduct more stringent cash flow projections and may limit the pool of eligible properties, thus impacting acquisition strategies.

For rental properties, the implications of these DSCR requirements are significant. Consider a multifamily property with a loan amounting to $1 million at a 7.5% interest rate, resulting in an annual debt service of approximately $85,000. To meet a DSCR of 1.35x, this property must generate an annual NOI of at least $114,750. If the same property generated only $100,000 in NOI under previous, lower-rate conditions, it would have comfortably met a 1.25x DSCR but now falls short of the more stringent requirements. This scenario necessitates either an increase in rental income or a reduction in expenses to remain viable, underscoring the importance of aggressive property management and strategic value-add improvements.

Hard money and bridge loans, typically utilized for short-term financing needs, are seeing rate premiums that reflect the heightened risk environment. Current rates for these types of loans have escalated to 9-12%, considerably higher than permanent financing options. The premium on these loans reflects both the increased cost of capital and the higher risk profile lenders associate with short-term, often speculative investments. These elevated rates necessitate a clear and profitable exit strategy to justify the initial investment, particularly in scenarios where a quick property turnaround or significant appreciation is anticipated.

Given the current rate environment, investors face critical decisions regarding refinance timing versus hold strategies. Refinancing at today’s higher rates may not be advantageous unless it aligns with a broader strategic initiative, such as extracting equity for reinvestment or restructuring debt to improve cash flow. Conversely, holding onto properties with existing favorable terms may be more prudent, provided the NOI remains robust. This scenario underscores the importance of timing in refinancing decisions and highlights the need for a comprehensive understanding of market trends and property-specific financial performance.

The current interest rate climate also affects acquisition criteria and underwriting standards. Investors are now more likely to adopt conservative assumptions when evaluating potential acquisitions, focusing on properties with strong cash flow histories and stable tenant bases. Underwriting standards have tightened, emphasizing thorough due diligence and realistic projections that account for potential economic fluctuations. These adjustments are essential to ensure that investments not only meet DSCR requirements but also align with broader financial goals and risk tolerance levels.

Investment Strategy & Risk Management

In the current market environment, timing is a crucial element for real estate investors seeking to maximize returns and minimize risk. Given the anticipated fluctuations in interest rates and the evolving buyer landscape, investors should adopt a flexible approach to market entry. Identifying opportunities requires a keen eye for distressed assets and undervalued properties that can be repositioned or improved for higher returns. As interest rates stabilize in 2026, investors should be prepared to act swiftly on acquisitions during periods of lower market competition, typically observed in the first and fourth quarters when transactional volume historically dips.

Risk factors in the current environment include potential economic slowdowns and fluctuating interest rates, which can impact both property values and financing costs. Mitigation strategies should include a focus on liquidity and maintaining a diverse portfolio. Investors should consider building a buffer in their financial models to account for potential rent decreases and vacancies. Furthermore, utilizing fixed-rate financing options where possible can guard against rate hikes, while maintaining ample cash reserves ensures flexibility during periods of market volatility.

To navigate this landscape, investors should adjust their acquisition criteria and underwriting standards by incorporating stress testing into their financial models. This involves simulating various downside scenarios, such as prolonged vacancies or unexpected maintenance costs, to assess the robustness of an investment. Diversifying across asset classes and geographies can also serve as a hedge against market-specific downturns. Additionally, refining the criteria for tenant quality and property condition in the acquisition phase can preemptively address potential risks associated with property management and cash flow stability.

Prime Property Funding’s focus on providing hard money loans, fix-and-flip financing, and DSCR loans positions investors to capitalize on short-term opportunities while maintaining long-term sustainability. By aligning financial products with strategic market insights, investors can optimize their portfolios for both growth and stability. Embracing these strategies empowers investors to navigate complexity with confidence and precision.

Key Considerations for Investors

- Fix-and-flip strategies: Target properties with a minimum spread of 20% between purchase price and after-repair value (ARV) to cushion against market shifts.

- Maintain holding costs below 5% of ARV to ensure profitability even with extended project timelines.

- Plan exit strategies to coincide with peak selling seasons, typically spring and summer, to maximize buyer interest and sale price.

- Buy-and-hold tactics: Aim for cap rates of 6% or higher in urban markets to ensure robust cash flow.

- Incorporate at least a 2% annual rent growth assumption in financial models, while stress testing with a flat growth scenario for conservative projections.

- Ensure DSCR cushions of at least 1.25 to safeguard against potential income fluctuations.

- Bridge financing: Opt for flexible draw schedules and maintain contingency reserves of at least 10% of project costs to manage unexpected expenses.

- Leverage the current rate environment by locking in rates before anticipated hikes to optimize financing costs.

- Geographic focus: Prioritize markets with a balanced mix of growth potential and affordability, such as secondary cities with robust job markets and population growth.

- Employ conservative underwriting by performing stress tests at a cap rate 100 basis points higher than the current market rate to assess viability under adverse conditions.

- Portfolio diversification: Balance investments across residential, commercial, and industrial assets to mitigate sector-specific risks.

- Ensure geographic spread across at least three different economic regions to reduce exposure to localized downturns.

- Risk mitigation: Maintain reserves equivalent to three months of operating expenses for each property to handle unforeseen expenses or income disruptions.

- Invest in comprehensive insurance policies and prioritize properties with strong structural integrity to limit potential liabilities.

- Focus on acquiring properties with high tenant quality to reduce turnover rates and enhance consistent cash flow.

Resources

External References

Disclaimer: This market analysis is for informational purposes only and should not be considered financial or investment advice. Market conditions can change rapidly. Consult with a qualified financial or lending professional before making any decisions.