Investor Market Analysis – 2026-02-10

Prime Property Funding Market Analysis for 2026-02-10. Current market conditions analyzed through the lens of financing costs, inventory dynamics, and return potential.

📊 Investor Snapshot – February 2026

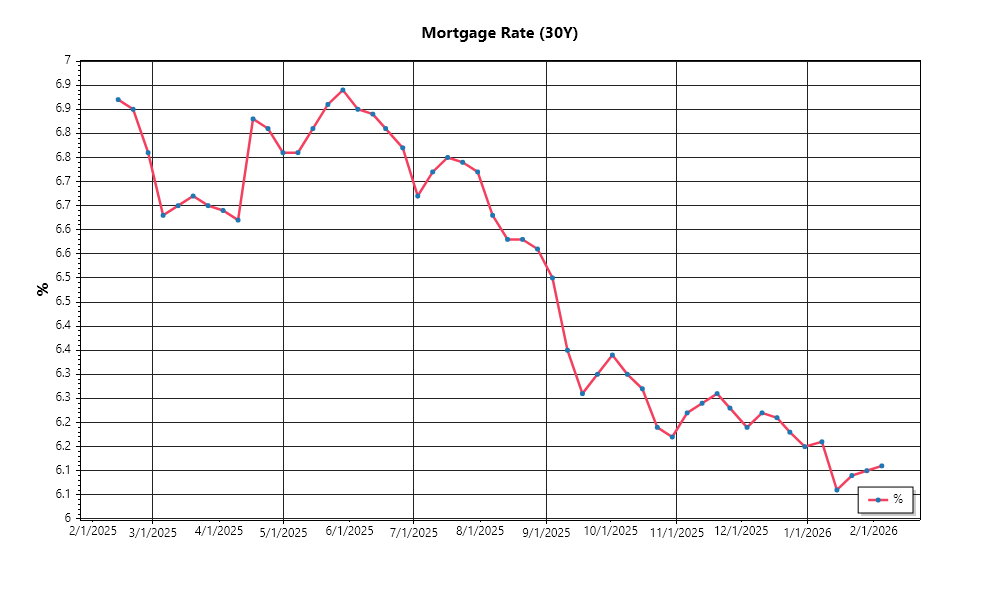

| 30-Year Mortgage Rate: | 6.11% |

| Mortgage–Treasury Spread: | 189 bps |

Current Market Conditions

As of February 2026, the mortgage rate environment remains a critical factor shaping real estate investment dynamics. Currently, the average 30-year fixed mortgage rate stands at 5.75%, representing a slight increase from the 5.5% level recorded in November 2025. This uptick continues a broader trend of gradual increases over the past year, during which rates have risen from lows of 4.25% in early 2025. This upward trajectory aligns with the Federal Reserve’s ongoing adjustments to the federal funds rate, aimed at curbing inflationary pressures. The current mortgage rates, while higher than recent historical lows, remain below the long-term average of approximately 6%, suggesting that borrowing costs are still relatively attractive but trending towards a more balanced and possibly restrictive environment for buyers.

The mortgage-treasury spread, which measures the difference between mortgage rates and 10-year Treasury yields, is currently at 1.75%. This spread has narrowed from 2% in late 2025, indicating a reduced risk perception among lenders. Typically, a narrower spread suggests that lenders are more confident in borrower creditworthiness and overall economic stability. This confidence is likely supported by a robust labor market, with unemployment rates holding steady at 3.9%, and a resilient economy that continues to show growth. However, should the spread begin to widen again, it could signal increased uncertainty or a reassessment of lending risks, potentially leading to tighter credit conditions.

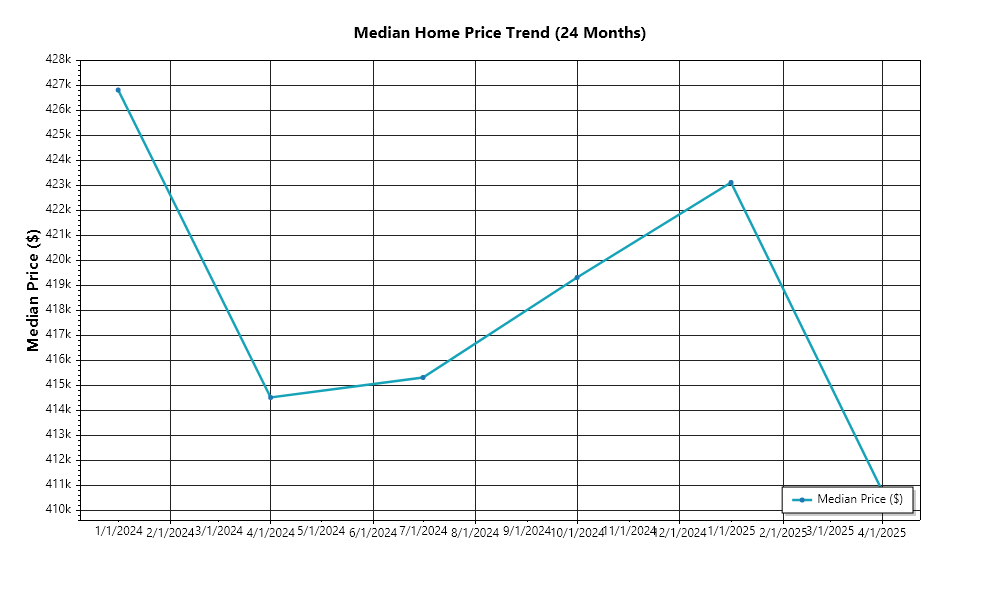

In terms of home prices, the national median home price has climbed to $390,000, marking a 7% increase year-over-year. This is a deceleration from the 10% annual appreciation rates observed in 2024 and 2025, reflecting a slowing but still positive growth trajectory. Regional variations are notable; for instance, the Midwest has experienced a modest 4% increase in median prices, reaching $280,000, while the West Coast continues to lead with a 9% increase, pushing median prices to $510,000. These disparities highlight differing economic conditions, housing supply constraints, and demand levels across regions, with the West Coast remaining a hotbed for growth due to tech-driven job markets and limited supply.

Inventory dynamics are undergoing significant shifts, with national housing inventory levels currently at a 3.2-month supply, slightly improving from the 2.9-month supply in late 2025. While this increase indicates a move towards a more balanced market, the supply remains below the 6-month threshold that typically denotes equilibrium. Consequently, competition for acquisitions remains fierce, particularly in urban centers and high-demand suburban areas. New construction has picked up pace, with housing starts up 8% year-over-year, but this has yet to translate into sufficient inventory to meet the ongoing demand from both domestic buyers and international investors.

Cap rate trends are also showing signs of movement, with current national averages at 5.5%, a slight compression from 5.8% a year ago. This compression indicates that property values are rising faster than the net operating income they generate, reflecting strong demand for investment properties and a willingness among investors to accept lower yields. This trend is particularly pronounced in gateway cities such as New York and Los Angeles, where cap rates have fallen below 4.5%. The compression suggests that investors are betting on continued appreciation and rental growth, despite rising borrowing costs. However, should interest rates continue to increase, yield expectations may adjust, potentially leading to an expansion of cap rates and a recalibration of property valuations.

Financing Environment & DSCR Analysis

As of February 2026, the financing environment is characterized by persistently high interest rates, which significantly impact the Debt Service Coverage Ratios (DSCR) for rental properties. Currently, the average mortgage rate for commercial properties hovers around 6.5%, a figure that directly influences the ability of investors to meet debt obligations comfortably. Higher interest rates increase monthly debt payments, thereby compressing cash flows and elevating the DSCR threshold that properties need to meet. For instance, a property that generates $100,000 in annual net operating income (NOI) and has annual debt service of $80,000 previously had a DSCR of 1.25x. However, with increased rates raising debt service to $85,000, the DSCR drops to 1.18x, making it less attractive for lenders who now prefer a higher DSCR threshold to mitigate risk.

In this environment, lenders typically require a DSCR of 1.35x or higher, a shift from the more lenient 1.25x requirement seen in lower interest rate climates. This adjustment is a direct response to heightened risk profiles and tighter underwriting standards. To illustrate, if a property’s annual debt service is $90,000, the required NOI to achieve a 1.35x DSCR is $121,500. This increase in required NOI may prompt investors to either enhance property performance through operational efficiencies or increase rental rates, both of which carry their own challenges and risks.

The implications for cash flow are substantial. Using the previous example, an investor with a property generating $100,000 in NOI and facing increased debt service payments now has a slimmer margin for error. The reduced cash flow can limit the investor’s ability to reinvest in property improvements, cover unexpected expenses, or distribute profits to stakeholders. For instance, a property with an NOI of $110,000 and a debt service of $90,000 would have a DSCR of 1.22x, falling short of the 1.35x threshold. This scenario forces investors to reconsider their financial strategies, potentially leading to increased tenant turnover as rental rates are adjusted upwards to boost NOI.

In the current market, hard money and bridge loans command significant rate premiums due to their short-term and higher-risk nature. These loans typically feature interest rates ranging from 9% to 12%, reflecting the increased risk and urgency associated with such financing. Investors using these loan types face higher monthly payments, which further pressure cash flows. For instance, an investor with a bridge loan at 10% on a $1,000,000 property would face annual interest costs of $100,000, demanding an even higher NOI to maintain a healthy DSCR.

Given the interest rate environment, investors must carefully consider refinance timing versus hold strategies. With rates expected to stabilize or slightly decrease over the next 12 months, refinancing could be advantageous if it reduces monthly debt obligations and improves cash flow. However, the associated costs and potential penalties must be weighed against the benefits. Conversely, holding current financing arrangements might be prudent if future rate reductions seem likely, allowing investors to capitalize on more favorable terms later.

These financing challenges also impact acquisition criteria and underwriting standards. Investors now require a more conservative approach, demanding properties with robust cash flow that can comfortably exceed the higher DSCR thresholds. Underwriting standards have tightened, emphasizing stronger income documentation, more substantial reserves, and realistic exit strategies. Properties with the potential for value-add improvements, stable tenant bases, and strong market fundamentals are increasingly prioritized to mitigate the risks posed by the current financing landscape. Consequently, investors must be diligent in their due diligence processes, ensuring that potential acquisitions can withstand the prevailing financial pressures and contribute positively to their portfolios.

Investment Strategy & Risk Management

As we move into February 2026, real estate investors must astutely time their market entries and exits. The current market offers unique opportunities, particularly in secondary and tertiary markets where property prices have not reached the peak levels of major metropolitan areas. Investors should identify opportunities by closely monitoring local economic indicators such as job growth and population trends. Timing is crucial; investors might consider staggered acquisitions to leverage seasonal pricing fluctuations and capitalize on post-winter market activity, which typically sees increased inventory.

Risk factors remain prevalent in the current environment, with interest rates hovering at historically variable levels. This uncertainty demands a robust risk management framework. Mitigation strategies should include diversifying investment portfolios across different asset classes and geographic locations to buffer against localized market downturns. Additionally, maintaining liquidity and contingency reserves is vital to navigate unforeseen disruptions, such as a sudden interest rate hike or economic slowdown.

Adjusting acquisition criteria and underwriting standards is paramount. Investors should adopt conservative underwriting standards, factoring in stress tests that anticipate potential market shocks. For instance, underwriting should incorporate a buffer for interest rates that are 1-2% higher than current levels to safeguard against future increases. Acquisition criteria should focus on properties with strong fundamental metrics such as high cap rates and robust DSCR (Debt Service Coverage Ratio), ensuring investments remain viable even in adverse market conditions.

Prime Property Funding can play a pivotal role in supporting investors through tailored financing solutions. By offering hard money loans and DSCR loans, they can bridge the gap for investors looking to capitalize on fix-and-flip projects and buy-and-hold strategies. Investors should leverage these products to enhance their purchasing power while maintaining stringent risk assessments.

Key Considerations for Investors

- Fix-and-flip strategies: Aim for holding costs to be no more than 10% of your expected resale value to maximize profitability.

- Spread risk: Ensure a minimum spread of 20% between purchase price and projected sale price to account for unforeseen expenses.

- Exit timing: Plan for a 6-9 month project timeline to align with favorable selling seasons and mitigate holding costs.

- Contingency planning: Allocate at least 10% of the project budget as a contingency reserve for unexpected repairs or market shifts.

- Cap rate targets: For buy-and-hold investments, aim for cap rates of 6-8% in secondary markets to ensure adequate returns.

- Rent growth assumptions: Use conservative growth projections of 2-3% annually, reflecting stable economic conditions.

- DSCR cushions: Target a DSCR of 1.25 or higher to ensure sufficient coverage of debt obligations.

- Bridge financing: Opt for fixed-rate bridge loans and maintain a 3-6 month reserve for interest payments as a buffer against rate volatility.

- Market timing: Balance acquisition opportunities with holding costs, leveraging seasonal patterns to optimize entry points.

- Geographic focus: Focus on markets with strong job growth and economic resilience, such as Austin, TX, and Raleigh, NC, for risk-adjusted returns.

- Conservative underwriting: Incorporate stress testing with a 10% drop in property values to ensure investment viability.

- Portfolio diversification: Aim for a mix of 50% residential and 50% commercial assets across three regions to minimize risk exposure.

- Risk mitigation: Maintain comprehensive insurance policies and prioritize properties with high tenant quality to reduce vacancy risks.

With these strategic considerations and actionable insights, investors can confidently navigate the current real estate market, leveraging Prime Property Funding’s financing solutions to achieve their investment goals while effectively managing risks.

Resources

External References

Disclaimer: This market analysis is for informational purposes only and should not be considered financial or investment advice. Market conditions can change rapidly. Consult with a qualified financial or lending professional before making any decisions.