Investor Market Analysis – 2026-06-13

Prime Property Funding Market Analysis for 2026-06-13. Current market conditions analyzed through the lens of financing costs, inventory dynamics, and return potential.

📊 Investor Snapshot – June 2026

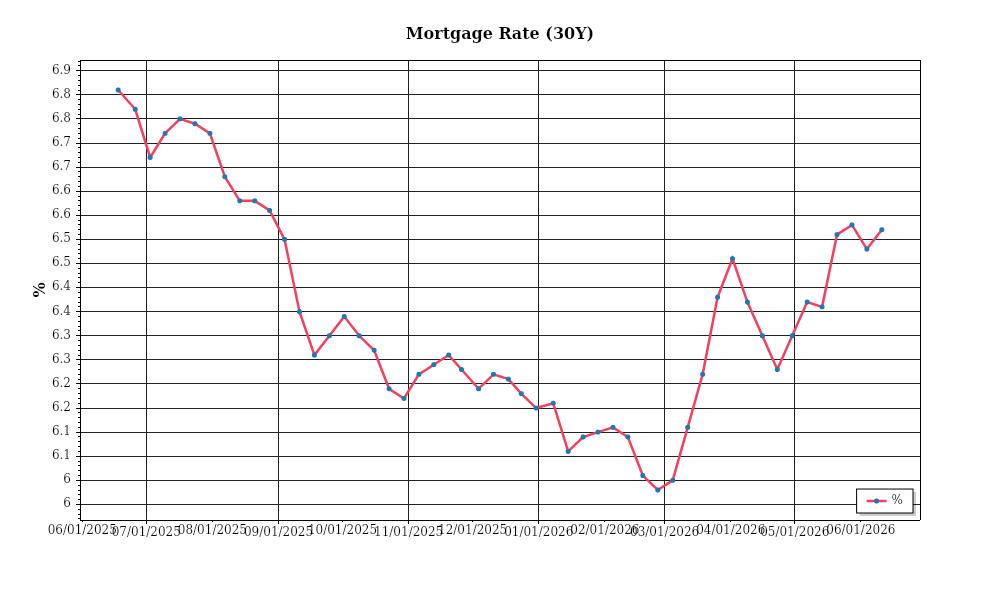

| 30-Year Mortgage Rate: | 6.52% |

| Mortgage–Treasury Spread: | 207 bps |

Current Market Conditions

As we analyze the real estate market in June 2026, we begin with the mortgage rate environment. Currently, the average 30-year fixed mortgage rate stands at 6.2%, showing a slight increase from the 5.8% average rate recorded in January 2026. This rise in mortgage rates can be attributed to the Federal Reserve’s continued efforts to curb inflation by gradually increasing interest rates over the last two years. The upward trend suggests a tightening monetary policy environment, which has been a consistent theme since late 2024 when rates were at a low of 3.5%. The trajectory indicates that mortgage rates could continue to rise, potentially reaching 6.5% by the end of 2026, should the Federal Reserve maintain its current policy stance. This environment places upward pressure on borrowing costs for consumers, which may dampen housing demand in the near term.

Examining the mortgage-treasury spread offers insights into lender risk perception. As of June 2026, the spread between the 30-year mortgage rate and the 10-year Treasury yield is approximately 1.75%. This figure is slightly above the historical average spread of 1.5%, indicating that lenders are factoring in higher perceived risks in the current economic environment. The widening spread often signals economic uncertainty or increased risk of borrower default, prompting lenders to demand higher compensation for the risk associated with long-term lending. The stability of this spread over the past year suggests that while risk perception is heightened, it is not escalating at an alarming rate. It offers a nuanced understanding of the mortgage market’s risk landscape, suggesting that lenders are cautious but not overly alarmed.

In terms of median home price trends, the national median home price in June 2026 is $425,000, reflecting a year-over-year appreciation rate of 4.2%. This is a deceleration compared to the 6.8% appreciation seen in 2025, pointing to a cooling market as affordability challenges and higher borrowing costs weigh on buyers. Regionally, variations are significant. For instance, the Southeast, particularly areas like Atlanta and Charlotte, continues to see robust growth with appreciation rates of 5.5% to 6%, driven by strong job markets and population inflows. Conversely, the West Coast has experienced a more modest growth of 2.5%, with cities like San Francisco and Los Angeles facing affordability constraints and a slowdown in tech sector growth impacting demand.

Inventory dynamics are also painting a picture of evolving market conditions. The total housing inventory at the end of June is 1.3 million units, which represents a 5.1% increase from a year ago. This rise in supply is partially attributed to an uptick in new housing starts, which have gradually rebounded post-pandemic. Despite this increase, the market remains somewhat competitive, with an average property staying on the market for 45 days, down from 60 days last year. This indicates a still-strong buyer interest, though not as fervent as during the peak pandemic-induced housing boom. The market balance is shifting slightly towards buyers, yet it remains firmly a seller’s market in many regions due to continued inventory constraints.

Cap rate trends are integral to understanding investment property dynamics. Currently, cap rates for commercial real estate average 5.1%, reflecting a slight compression from the 5.4% seen twelve months earlier. This compression signifies a continued high demand for investment properties, albeit at a slower pace. The yield compression suggests investors are accepting lower returns in exchange for perceived stability and potential capital appreciation. However, as interest rates rise, there might be upward pressure on cap rates, particularly in sectors with weaker fundamentals. Investors are advised to watch these trends closely, as even slight movements can significantly impact property valuations and investment strategies.

Financing Environment & DSCR Analysis

The financing environment in June 2026 is characterized by lingering high interest rates, which significantly impact the debt service coverage ratios (DSCR) for real estate investments. As the Federal Reserve maintains a cautious approach to inflationary pressures, interest rates remain elevated, leading to higher borrowing costs. The increased cost of capital has a direct effect on DSCR, as investors must ensure that their rental income sufficiently covers their debt obligations. With current mortgage rates hovering around 7%, the ability to meet or exceed the typical DSCR thresholds of 1.25x to 1.35x becomes more challenging. This environment necessitates that investors conduct thorough cash flow analyses to ensure their properties can generate enough income to cover increased interest payments without jeopardizing financial stability.

In this interest rate climate, lenders exhibit a preference for higher DSCR requirements to mitigate risk. While a DSCR of 1.25x has historically been a common threshold, the current environment often sees lenders favoring a minimum DSCR of 1.35x. This shift reflects the need for a stronger buffer to absorb potential fluctuations in rental income or unexpected vacancies. For example, consider a property generating $120,000 annually in net operating income (NOI). At a DSCR of 1.25x, the maximum allowable debt service would be $96,000. However, with a 1.35x requirement, this figure drops to approximately $88,888, thereby limiting the loan amount and affecting the leverage investors can apply.

The implications for cash flow in rental properties are pronounced. With higher interest rates, investors must ensure that their rental properties produce sufficient income to meet these stricter DSCR requirements. Using the above example, if a property’s mortgage payment increases from $7,500 to $8,000 monthly due to higher interest rates, the annual debt service rises to $96,000 from $90,000. If the property was initially yielding a DSCR of 1.25x, this increase in debt service would push the ratio down, potentially below the acceptable threshold. To maintain financial health, investors may need to explore rent increases, operational efficiencies, or even additional revenue streams to bolster NOI.

In terms of alternative financing, the demand for hard money and bridge loans has increased, albeit with notable premiums. These short-term financing solutions often carry interest rates 2-4 percentage points higher than traditional loans, reflecting the added risk lenders assume. Current hard money loans might command rates upwards of 10%, placing further pressure on cash flow and DSCR. Investors utilizing these loans must be particularly astute in their exit strategies, ensuring that refinancing or property sales occur before interest obligations erode profitability.

The current rate environment also influences decisions around refinancing and holding strategies. With interest rates expected to stabilize but remain high in the near term, investors face a dilemma: refinance now to lock in rates before potential further hikes, or hold in anticipation of a more favorable future rate environment. Timing is crucial, and the decision hinges on individual property performance and market conditions. Investors must weigh the immediate benefits of refinancing against the long-term potential of holding until rates decrease, which could enhance property values and cash flow.

Finally, the acquisition criteria and underwriting standards are tightening. With lenders demanding higher DSCRs and risk premiums, investors need to adopt more conservative approaches. This includes scrutinizing property locations, tenant quality, and lease terms more rigorously. Properties that demonstrate robust NOI potential and resilience under various economic scenarios become increasingly attractive in this environment. Underwriting standards now emphasize stress testing against potential interest rate hikes and vacancy risks, ensuring that properties can withstand financial pressures without compromising profitability. The current financing climate demands meticulous financial planning and strategic decision-making to optimize returns while navigating heightened lending standards.

Investment Strategy & Risk Management

In the current real estate climate, effective market timing and opportunity identification are crucial for optimizing investment returns. Given the cyclical nature of real estate markets, investors should focus on timing their acquisitions to align with local market trends. As of June 2026, the market is experiencing a moderate cooling phase following a period of rapid appreciation. This offers strategic opportunities for those prepared to capitalize on reduced competition and softer pricing. Investors should target properties with value-add potential, specifically in markets where inventory levels are rising, and price corrections are underway. Such conditions present a fertile ground for both fix-and-flip and buy-and-hold strategies, provided investors are diligent in their due diligence.

The current environment poses several **risk factors** that need strategic mitigation. With interest rates relatively high compared to the past decade, financing costs have become a significant concern. Investors should focus on **fixed-rate financing** options to hedge against further rate hikes and ensure predictable cash flows. Additionally, market volatility necessitates a conservative approach to underwriting. Stress testing assumptions such as vacancy rates, rent growth, and cap rate fluctuations will be vital in safeguarding against potential downturns. Building a substantial **contingency reserve** is recommended to cover unforeseen expenses and market shifts.

Adjusting **acquisition criteria** and underwriting standards is essential in navigating this landscape. Investors should prioritize properties with strong **fundamental metrics**, such as robust cash flow potential and favorable location attributes. For fix-and-flip ventures, this means targeting undervalued properties in neighborhoods with a high demand for renovated homes. For buy-and-hold investments, pursuing properties with a cap rate of at least 6% and a strong rental demand will be key. Furthermore, leveraging technology and data analytics to refine investment models can enhance decision-making and identify hidden opportunities.

Key Considerations for Investors

- Focus on **fix-and-flip** properties with holding costs below 1.5% of the acquisition price per month to maintain profitability.

- Pursue a **spread risk** strategy by targeting properties with a minimum 15% profit margin after renovation costs.

- Ensure **exit timing** aligns with seasonal peaks in local markets, typically spring and early summer, to maximize sales potential.

- Incorporate a **contingency planning** buffer of at least 10% of the renovation budget to accommodate unexpected expenses.

- Set **cap rate targets** at a minimum of 6% for buy-and-hold properties to ensure adequate cash flow and risk-adjusted returns.

- Assume conservative **rent growth** projections of 3-4% annually to buffer against economic fluctuations.

- Maintain a **DSCR cushion** of at least 1.25x to ensure loan servicing capability amidst potential revenue declines.

- Leverage **bridge financing** with flexible draw schedules and negotiate for interest-only terms to optimize cash flow.

- Prioritize markets with strong fundamentals such as low unemployment and population growth for **geographic focus** to achieve best risk-adjusted returns.

- Adopt **conservative underwriting** practices by stress testing properties under worst-case scenarios, including a 10% decline in property values.

By embracing these strategies and insights, Prime Property Funding and its investors can confidently navigate the evolving real estate landscape, seizing opportunities while effectively managing risk. The current environment, with its unique challenges and opportunities, is ripe for strategic action and well-informed decision-making, empowering investors to achieve their financial goals.

Resources

External References

Disclaimer: This market analysis is for informational purposes only and should not be considered financial or investment advice. Market conditions can change rapidly. Consult with a qualified financial or lending professional before making any decisions.