Investor Market Analysis – 2026-06-12

Prime Property Funding Market Analysis for 2026-06-12. Current market conditions analyzed through the lens of financing costs, inventory dynamics, and return potential.

📊 Investor Snapshot – June 2026

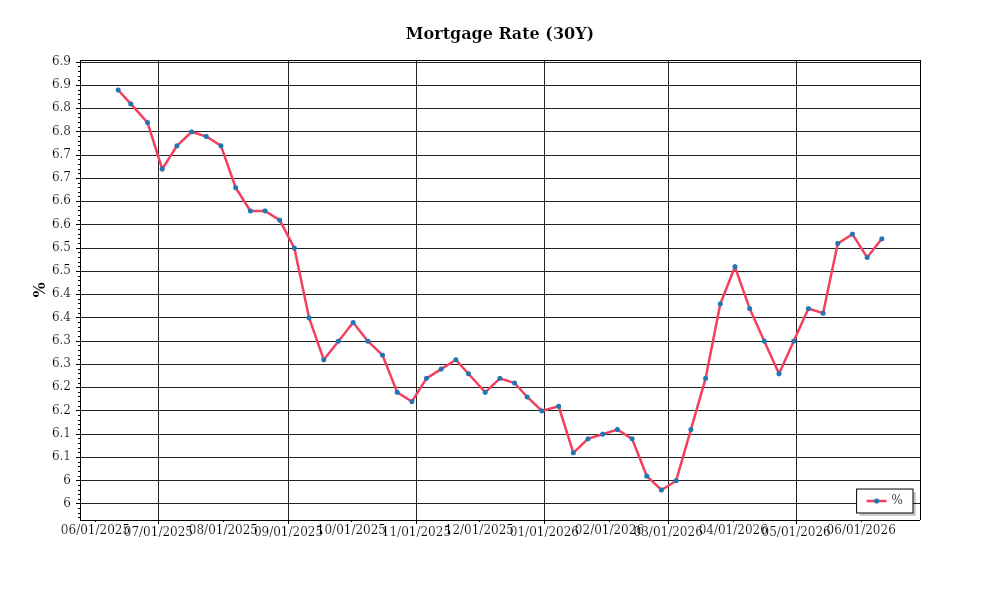

| 30-Year Mortgage Rate: | 6.52% |

| Mortgage–Treasury Spread: | 197 bps |

Current Market Conditions

As of June 2026, the real estate market is navigating a complex landscape characterized by fluctuating mortgage rates, shifting inventory levels, and evolving investment dynamics. The mortgage rate environment remains a critical factor in the real estate market. Currently, the average 30-year fixed mortgage rate stands at 6.3%, reflecting a stabilization from the volatility observed in the past year. Over the past six months, rates have fluctuated between 5.8% and 6.5%, largely influenced by Federal Reserve policies aiming to curb inflation. This pattern suggests a gradual upward trajectory, albeit at a slower pace compared to the rapid increases witnessed in 2025. The stabilization of rates at this level implies a more predictable cost for homebuyers, potentially encouraging more consistent buyer activity as the market adjusts to this new normal.

The spread between mortgage rates and 10-year Treasury yields, a critical indicator of lender risk perception, currently averages 180 basis points. This spread has narrowed slightly from the 200 basis points observed in late 2025, indicating that lenders perceive a reduction in market risk. A narrower spread suggests that lenders are becoming more confident in the economic environment and the creditworthiness of borrowers. However, this spread remains above the long-term average of 150 basis points, signaling a lingering caution among lenders. The implications for investors are significant; lower perceived risk typically leads to more favorable lending conditions, potentially supporting increased real estate investment and acquisition activity.

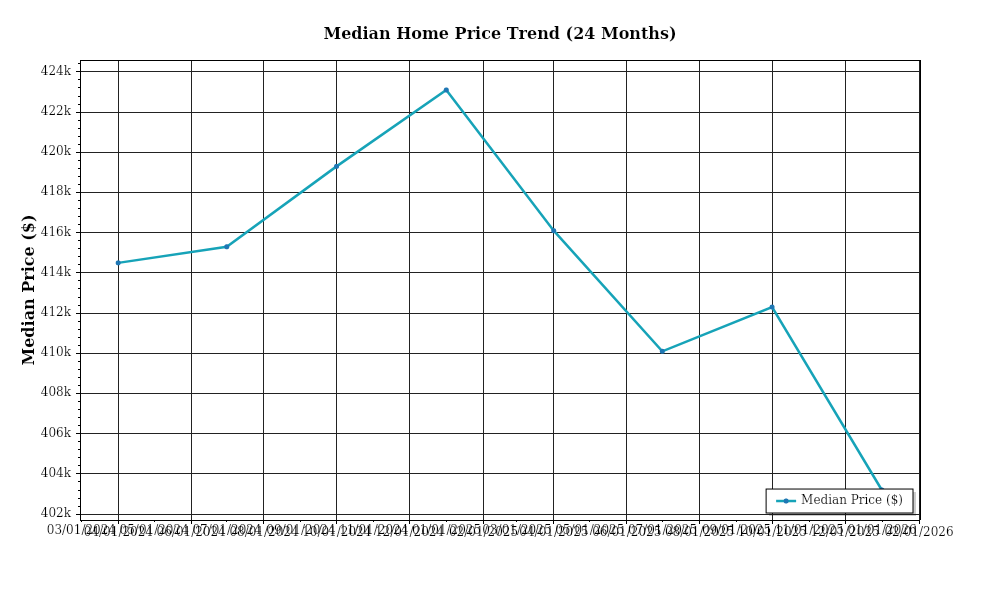

Median home prices continue to show robust growth, with the national median home price now at $420,000, marking a 4.8% increase year-over-year. This appreciation rate, while substantial, represents a tapering from the double-digit growth seen in 2024 and 2025, indicative of a cooling yet resilient market. Regional variations are pronounced, with the South and West experiencing the highest gains at 6% and 5.5% respectively, driven by ongoing population growth and economic expansion in these areas. Conversely, the Northeast sees a modest increase of 2.5%, reflecting demographic shifts and saturation in urban centers. These trends suggest a continued attractiveness of growth markets for investors seeking capital appreciation.

Inventory dynamics reveal a market still grappling with supply constraints, though there are signs of gradual improvement. Current housing inventory stands at 3.4 months of supply, a slight increase from the 3.1 months recorded earlier this year. This uptick suggests a slow movement towards a more balanced market, though the metric still falls short of the 5-6 months considered indicative of a balanced market. The competition for acquisitions remains intense, particularly in the entry-level and mid-market segments, where demand continues to outstrip supply. This scenario underscores ongoing opportunities for developers and investors to capitalize on pent-up demand, especially in regions experiencing significant population growth.

Cap rate trends provide further insight into the market’s investment dynamics. The average cap rate for commercial real estate currently stands at 5.2%, reflecting a slight compression from 5.5% at the start of the year. This compression is indicative of strong investor demand and limited supply of high-quality assets, leading to upward pressure on prices. Notably, sectors such as industrial and multifamily are experiencing the most significant cap rate compression, driven by robust demand fundamentals. For investors, yield compression signals potential capital appreciation but also requires careful consideration of asset selection and risk management strategies to ensure sustainable returns.

In summary, the real estate market as of June 2026 presents a mixed picture of stabilization in mortgage rates, cautious optimism among lenders, regional disparities in home price appreciation, and ongoing supply constraints. These dynamics underscore the importance of strategic decision-making for investors looking to navigate this evolving landscape effectively.

Financing Environment & DSCR Analysis

As of June 2026, the financing environment for real estate investments is characterized by rising interest rates, which significantly influence the Debt Service Coverage Ratios (DSCR) across the sector. Current interest rates have climbed to approximately 7.5%, a notable increase from the sub-4% rates seen just a few years ago. This escalation has direct implications for DSCR, a critical metric used by lenders to assess a property’s ability to cover its debt obligations. Higher interest rates result in increased monthly mortgage payments, thereby reducing the cash flow available for debt service. For instance, a loan amount of $1 million at a 7.5% interest rate over 30 years yields a monthly payment of approximately $6,992. In contrast, the same loan at a 4% interest rate would require around $4,774 monthly. This increase of over $2,200 significantly impacts the DSCR, necessitating higher rental income to maintain traditional DSCR thresholds.

In this high-rate environment, lenders are adjusting their expectations, with typical DSCR requirements now trending towards the upper end of the spectrum. While the industry standard often hovers around a 1.25x DSCR, many lenders are now requiring a 1.35x DSCR to cushion against potential income fluctuations and increased debt service costs. This shift places additional pressure on property investors to either enhance revenue streams or seek properties with inherently higher income potential. For example, to meet a 1.35x DSCR on the aforementioned mortgage payment of $6,992, a property would need to generate a monthly net operating income (NOI) of approximately $9,439, compared to $8,740 for a 1.25x DSCR. This adjustment compels investors to rigorously evaluate a property’s income-producing capabilities before acquisition.

The cash flow implications for rental properties under these conditions are profound. Properties that previously maintained robust cash flows might now find themselves under tighter constraints. Consider a multifamily property generating $10,000 in monthly NOI. Under a 1.35x DSCR requirement, the allowable debt service would be approximately $7,407, leaving a narrow margin for the $6,992 payment. In this scenario, even minor rental income disruptions could jeopardize cash flow stability. Therefore, investors must closely analyze tenant profiles, market rent trends, and potential operational efficiencies to safeguard against cash flow volatility.

In the current market, hard money and bridge loans are commanding substantial premiums over traditional financing, with rates typically ranging between 9% and 12%. These rates reflect the increased risk and short-term nature of such loans, making them suitable for investors needing quick capital for competitive acquisitions or property improvements. However, the high cost necessitates a swift transition to traditional financing to optimize long-term returns. Investors should carefully strategize the timing of refinancing to capitalize on any potential rate drops, balancing the cost of holding high-interest debt against the benefits of securing a long-term, lower-rate mortgage.

The prevailing interest rate environment is also influencing acquisition criteria and underwriting standards. Investors are increasingly cautious, focusing on properties with strong income histories and resilient market positions. Underwriting now often involves stress-testing against potential vacancy spikes or rent reductions to ensure DSCR thresholds remain intact. Additionally, acquisition teams are prioritizing properties in locations with robust economic indicators and potential for rent growth to mitigate interest rate impacts. As such, investors are advised to exercise diligence in evaluating property fundamentals and market dynamics, ensuring alignment with evolving lender expectations and financial objectives.

Investment Strategy & Risk Management

In the current real estate climate, characterized by rising interest rates and a fluctuating economic landscape, timing and strategic opportunity identification are crucial for successful investments. **Market timing** is particularly important as economic indicators suggest potential shifts in property values. Investors should target acquisitions during periods of lower market activity, typically in the third and fourth quarters, when sellers are more motivated and prices may soften. Identifying properties in emerging neighborhoods or those poised for gentrification can offer significant upside potential.

Risk factors are notably pronounced due to economic uncertainty and interest rate volatility. **Mitigation strategies** include diversifying portfolios by incorporating a mix of asset classes and geographic locations to buffer against localized market downturns. Additionally, implementing conservative underwriting standards is essential. Stress testing assumptions on interest rates, vacancy rates, and rental income helps ensure resilience in adverse conditions. Investors should maintain higher cash reserves to manage unforeseen expenses, thus reducing reliance on financing during periods of tight monetary policy.

Adjustments in acquisition criteria and underwriting standards are necessary to navigate the turbulent market. Prioritize properties with strong cash flow potential and lower leverage ratios to reduce financial stress. Incorporating conservative rent growth assumptions and higher **Debt Service Coverage Ratios (DSCR)** can better withstand economic shocks. Additionally, focusing on properties that offer intrinsic value through renovation or strategic location advantages can enhance returns and mitigate risks.

In this dynamic environment, Prime Property Funding should emphasize flexibility in their loan products, catering to investors who are adept at identifying and seizing opportunities in a rapidly changing market. Offering competitive rates for **fix-and-flip** ventures and ensuring robust due diligence processes can help investors mitigate risks associated with holding costs and market timing. For **buy-and-hold** strategies, investors should prioritize properties with strong **cap rates** and potential for rent appreciation, ensuring stable cash flow and long-term value appreciation.

Key Considerations for Investors

- Fix-and-flip strategies: Limit holding costs by selecting projects with timelines under 6 months and buffer for a 10-15% contingency on budget overruns.

- Spread risk: Diversify fix-and-flip projects across different property types and price points to hedge against specific market segment downturns.

- Exit timing: Align project completions with peak selling seasons (spring and early summer) to maximize market exposure and price premiums.

- Buy-and-hold tactics: Target properties with cap rates of at least 7% to ensure sufficient cash flow and account for potential market fluctuations.

- DSCR cushions: Aim for a DSCR of 1.4 or higher to provide more room for error in rental income projections.

- Bridge financing: Secure flexible draw schedules that accommodate project pacing, and maintain a contingency reserve of at least 10% of the total project cost.

- Market timing: Actively monitor local economic indicators to anticipate acquisition opportunities that align with market cycles.

- Geographic focus: Concentrate efforts on secondary markets with strong job growth and population influx, such as Austin, TX, and Raleigh, NC, for better risk-adjusted returns.

- Conservative underwriting: Implement stress tests assuming a 2% increase in interest rates and a 5% increase in vacancy rates to ensure robustness.

- Risk mitigation: Build reserves to cover at least 6 months of operating expenses, and prioritize properties with stable tenant histories and good condition to minimize unexpected repairs.

By employing these strategic approaches, investors can position themselves to capitalize on opportunities in the evolving real estate landscape while effectively managing risks.

Resources

External References

Disclaimer: This market analysis is for informational purposes only and should not be considered financial or investment advice. Market conditions can change rapidly. Consult with a qualified financial or lending professional before making any decisions.