Investor Market Analysis – 2026-06-11

Prime Property Funding Market Analysis for 2026-06-11. Current market conditions analyzed through the lens of financing costs, inventory dynamics, and return potential.

📊 Investor Snapshot – June 2026

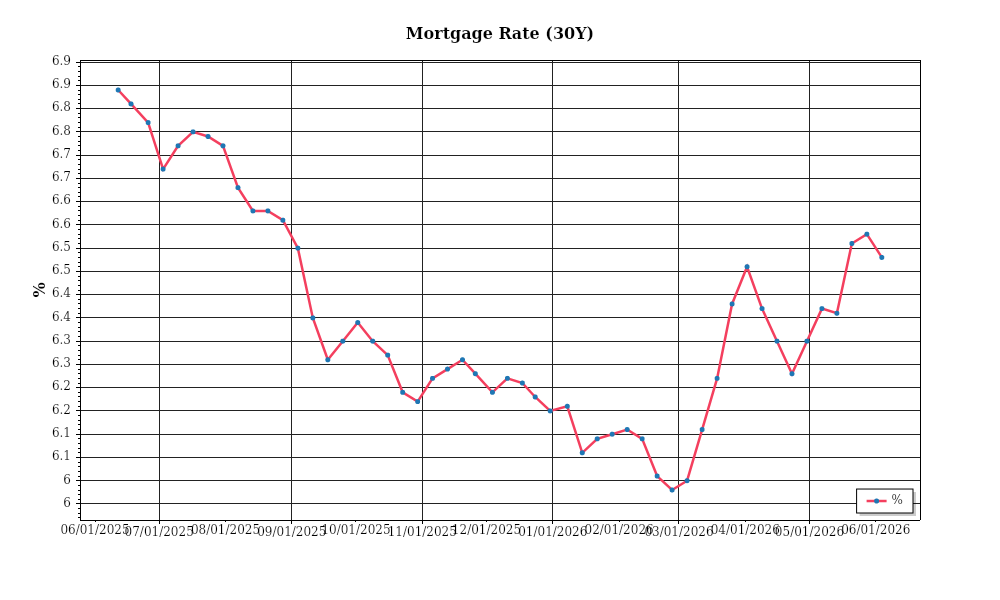

| 30-Year Mortgage Rate: | 6.48% |

| Mortgage–Treasury Spread: | 195 bps |

Current Market Conditions

As of June 2026, the real estate market operates within a complex landscape characterized by several key financial metrics and trends. The mortgage rate environment currently exhibits a moderately elevated stance, with the average 30-year fixed mortgage rate hovering around 5.8%. This is a slight increase from the 5.5% recorded in January 2026, reflecting a consistent upward trajectory over the past six months. This rise is partially attributed to the Federal Reserve’s recent monetary policy decisions aimed at curbing inflationary pressures. As inflation remains above the target rate, the trajectory of mortgage rates is expected to continue on this upward path, albeit at a slower pace, influenced by anticipated stabilization in broader economic conditions.

The mortgage-treasury spread serves as a critical indicator of lender risk perception, currently standing at 1.85%. This spread has narrowed from 2.1% in early 2026, suggesting a decline in perceived risk among lenders. The contraction in the spread indicates growing confidence in the housing market’s resilience, despite broader economic uncertainties. The reduction can be attributed to stabilizing economic indicators and improving borrower credit profiles. However, this spread remains above pre-pandemic levels, highlighting persistent caution in the lending environment. A continued decrease in the spread could signal further lender confidence, potentially leading to more favorable borrowing conditions.

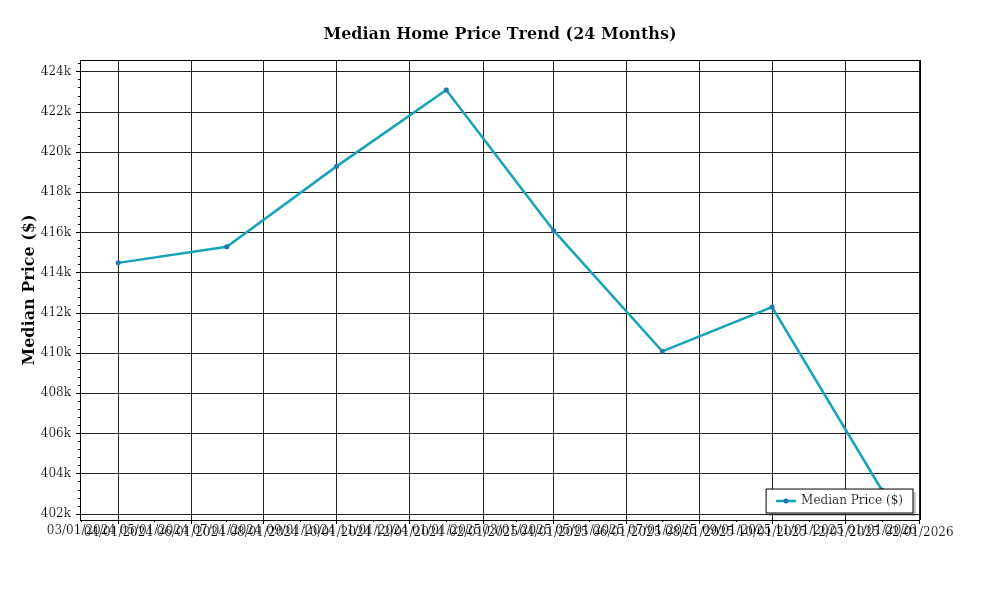

Median home price trends reveal a nationwide appreciation, with the median home price reaching $410,000 in June 2026, representing a 6.2% increase year-over-year. This appreciation rate is a deceleration from the double-digit growth rates observed during the pandemic-induced housing boom. Regional variations are significant, with the West Coast continuing to experience robust growth. For instance, cities like San Francisco and Seattle have recorded appreciation rates of 8.5% and 7.9% respectively. In contrast, the Midwest shows more modest increases, with cities like Chicago witnessing a 4.1% rise. These disparities are largely influenced by differences in local economic conditions, employment growth, and demographic shifts.

Inventory dynamics reveal a market grappling with limited supply. Current housing inventory levels are at 2.8 months of supply, significantly below the balanced market benchmark of 6 months. This low inventory level is indicative of a seller’s market, characterized by intense competition for available properties. The shortage is exacerbated by supply chain disruptions and labor shortages in the construction sector, which have slowed new home builds. Consequently, buyers face heightened competition, often resulting in bidding wars and further pressure on home prices. The imbalance between supply and demand underscores the need for increased housing production to alleviate market pressures.

Cap rate trends in the commercial real estate sector reflect a nuanced picture of yield dynamics. The average cap rate has expanded slightly to 5.3%, up from 5.1% at the beginning of 2026. This marginal expansion suggests a period of yield stabilization following years of compression driven by historically low interest rates. The expansion is largely attributed to rising borrowing costs and investor demand for higher returns in an environment of increased economic uncertainty. Notably, the industrial real estate segment continues to attract significant investor interest, maintaining lower cap rates due to strong demand for logistics and warehouse spaces. Conversely, the retail sector experiences higher cap rates as it navigates ongoing challenges related to e-commerce competition and changing consumer behavior.

In summary, the current real estate market is shaped by varying forces, including rising mortgage rates, a narrowing mortgage-treasury spread, and regional disparities in home price appreciation. Limited inventory levels continue to fuel competitive conditions, while cap rates reflect broader economic influences and sector-specific dynamics. Understanding these factors is crucial for investors as they navigate the evolving landscape and assess opportunities within the real estate market.

Financing Environment & DSCR Analysis

As of June 2026, the financing environment presents a complex landscape for real estate investors. Current interest rates, hovering around 6.5% for conventional loans, significantly impact the Debt Service Coverage Ratio (DSCR), a critical metric used by lenders to assess the risk associated with lending. The increase in interest rates over the past year has led to higher monthly debt obligations, squeezing the DSCR for many properties. For instance, a property with an annual net operating income (NOI) of $120,000 and a debt service of $100,000 would have a DSCR of 1.2, falling below the preferred threshold in most lending scenarios. This environment necessitates a closer examination of cash flows to ensure compliance with lender requirements.

In this climate, the typical DSCR requirements range from 1.25x to 1.35x. The 1.25x threshold represents a minimum level of comfort for risk-averse lenders, while more conservative financial institutions might demand a DSCR closer to 1.35x to mitigate the risk associated with rising interest rates and potential market volatility. For example, to achieve a 1.35x DSCR on the previously mentioned property, the NOI would need to increase to $135,000, assuming the debt service remains constant. This higher requirement pressures investors to either enhance operational efficiencies to boost income or seek properties with stronger initial cash flows.

In terms of cash flow implications for rental properties, rising interest rates present a dual challenge of increased financing costs and potentially stagnant rental income growth in some markets. Consider a multi-family rental property with a monthly rental income of $10,000 and operating expenses of $4,000, leaving an NOI of $6,000. With a loan amount of $800,000 at a 6.5% interest rate on a 30-year amortization, the monthly debt service is approximately $5,060. This results in a DSCR of 1.19, which falls short of even the lower 1.25x requirement. Investors must either increase rents, if market conditions allow, or renegotiate terms to maintain positive cash flow and remain attractive to lenders.

Exploring hard money and bridge loan rate premiums, these typically exceed conventional loan rates by 3-5%, given their short-term nature and higher risk profile. Presently, hard money loans might command rates upwards of 9-11%, while bridge loans are slightly lower, typically ranging from 8-10%. These financing tools are crucial for investors looking to capitalize on quick acquisitions or property renovations. However, the premium rates necessitate careful calculation to ensure the anticipated property value increase or rental income boost justifies the initial higher cost of capital.

In deciding between refinance timing versus hold strategies, the current rate environment suggests a cautious approach. Investors considering refinancing must weigh potential savings from securing a fixed-rate mortgage at current rates against the possibility of rate decreases in the future. Those holding properties with existing favorable terms might prefer to wait, especially if they anticipate stabilization or reduction in rates over the next 12-24 months. On the other hand, those with adjustable-rate mortgages or nearing maturity dates might find refinancing advantageous to lock in rates before potential further hikes.

The current financing environment significantly impacts acquisition criteria and underwriting standards. Investors are advised to adopt stringent criteria, focusing on properties with existing strong cash flows or demonstrable potential for income growth. Underwriting standards have tightened, with lenders scrutinizing income stability, property condition, and market dynamics more meticulously to ensure that properties meet the elevated DSCR thresholds. This necessitates thorough due diligence and potentially adjusting investment strategies to align with lender expectations and maintain investment viability.

## Investment Strategy & Risk Management

In the current real estate landscape, strategic timing and proactive opportunity identification are quintessential for investors aiming to capitalize on market cycles. With recent interest rate fluctuations and a shifting economic backdrop, discerning the optimal entry and exit points has never been more crucial. Investors should prioritize data-driven decision-making, leveraging market analytics to identify undervalued properties and emerging neighborhoods. The timing of acquisitions should align with economic indicators that suggest a favorable buying environment, such as lower-than-average property prices or an uptick in rental demand.

Despite the potential for lucrative returns, the current environment presents several risk factors that require careful mitigation. Interest rate volatility remains a significant concern, affecting both acquisition costs and profitability margins. Investors must employ hedging strategies and consider fixed-rate financing options to safeguard against rate hikes. Moreover, the supply chain disruptions and labor shortages observed in construction and renovation projects necessitate contingency planning and flexible project timelines. By incorporating buffer periods and cost overruns into their financial models, investors can better navigate these uncertainties.

Adjusting acquisition criteria and underwriting standards is pivotal in this context. The emphasis should be on conservative valuation approaches, ensuring that purchase prices align with realistic market valuations. Investors are advised to stress test their financial assumptions under various scenarios, accounting for potential declines in property values or rental incomes. Diversifying investment portfolios across different asset classes and geographic areas can help mitigate localized market risks and balance exposure. In particular, Prime Property Funding should focus on markets with strong economic fundamentals and favorable demographic trends, which tend to offer more stable, risk-adjusted returns.

Prime Property Funding’s role in providing hard money loans, fix-and-flip financing, and DSCR loans positions it well to support investors in capitalizing on current opportunities. By maintaining stringent underwriting standards and a robust risk assessment framework, the company can ensure that it extends credit to projects with the highest likelihood of success. Encouraging clients to maintain adequate reserves and insurance coverage, prioritize tenant quality, and ensure property condition are key strategies for enhancing the resilience of investment portfolios.

### Key Considerations for Investors

– **Fix-and-flip strategies**: Aim for a minimum gross profit margin of 20% to cover holding costs and spread risks. Implement a thorough exit strategy by setting a target timeline of 6-12 months for project completion and sale.

– **Buy-and-hold tactics**: Target a cap rate of at least 6% in high-demand urban areas, with rent growth assumptions not exceeding 3% annually to avoid optimistic forecasting. Maintain a DSCR cushion of 1.25x to ensure sufficient cash flow coverage.

– **Bridge financing**: In the current rate environment, lock in rates early and establish a detailed draw schedule with contingency reserves of at least 10% of project costs to cover unforeseen expenses.

– **Market timing**: Focus acquisitions during off-peak seasons, such as late fall and winter, to benefit from lower competition and potentially reduced prices.

– **Geographic focus**: Prioritize investment in secondary markets with job growth exceeding 2% annually, which often offer better risk-adjusted returns compared to saturated primary markets.

– **Conservative underwriting**: Stress test investment assumptions by simulating a 10% drop in property values and a 20% increase in interest rates to gauge resilience under adverse conditions.

– **Portfolio diversification**: Maintain a balanced asset class mix, with no single asset comprising more than 25% of the portfolio, ensuring geographic spread across at least three distinct regions.

– **Risk mitigation**: Establish reserves covering at least six months of operating expenses and ensure comprehensive insurance policies are in place. Prioritize high-quality tenants to minimize vacancy risks and maintain property conditions to preserve asset value.

By adhering to these strategic considerations and maintaining a proactive stance on risk management, investors can navigate the complexities of the current market with confidence and precision, ensuring sustainable growth and resilience in their real estate portfolios.

Resources

External References

Disclaimer: This market analysis is for informational purposes only and should not be considered financial or investment advice. Market conditions can change rapidly. Consult with a qualified financial or lending professional before making any decisions.