Investor Market Analysis – 2026-06-06

Prime Property Funding Market Analysis for 2026-06-06. Current market conditions analyzed through the lens of financing costs, inventory dynamics, and return potential.

📊 Investor Snapshot – June 2026

| 30-Year Mortgage Rate: | 6.48% |

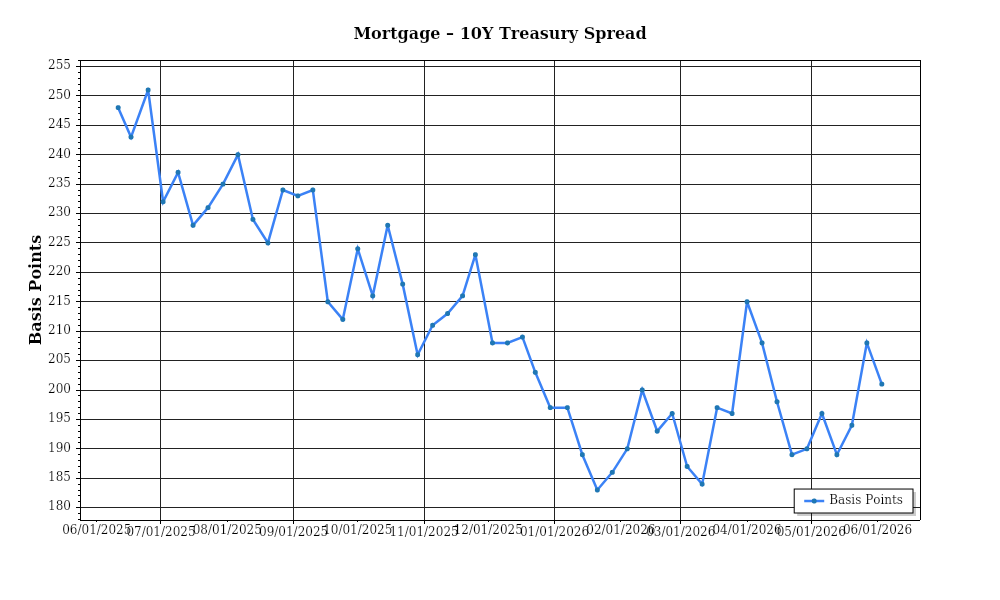

| Mortgage–Treasury Spread: | 201 bps |

Current Market Conditions

As of June 2026, the real estate market is navigating a complex landscape influenced by a variety of economic factors. The current mortgage rate environment is a critical component, with the average 30-year fixed mortgage rate standing at 5.25%. This marks a slight decrease from the 5.5% observed in January 2026, suggesting a modest easing in borrowing costs for homebuyers. Despite this decline, the rate remains elevated compared to pre-pandemic levels, which hovered around 3.75% in 2019. This upward trajectory has been driven by the Federal Reserve’s continued commitment to controlling inflation, with incremental rate hikes throughout 2025. The trajectory suggests that while minor fluctuations may occur, substantial rate reductions seem unlikely in the near term, as the central bank prioritizes inflation containment over aggressive rate cuts.

The mortgage-treasury spread, a critical indicator of lender risk perception, currently sits at 1.75%, a slight compression from the 2.0% spread recorded at the beginning of 2026. This spread, which measures the difference between the yields on mortgage-backed securities and 10-year Treasury notes, typically widens when lenders perceive higher risk in the mortgage market. The current compression implies a cautiously optimistic stance among lenders, reflecting a stabilization in credit risks and a more favorable economic outlook. However, this spread remains wider than the pre-pandemic average of 1.5%, indicating that while risks are perceived to be decreasing, they have not returned to pre-pandemic norms.

Median home price trends provide further insight into market conditions. As of June 2026, the national median home price is $415,000, reflecting a 6% year-over-year increase from $391,000 in June 2025. This appreciation rate, while robust, shows signs of deceleration compared to the 10% annual growth observed in the pandemic-fueled markets of 2021 and 2022. Regional variations persist, with the Sun Belt states experiencing stronger growth, such as a 8% increase in Texas, while traditionally high-cost areas like California exhibit more modest gains of around 3%. This variation underscores the importance of regional economic conditions and demographic shifts, particularly the migration trends favoring more affordable and tax-friendly states.

Inventory dynamics reveal an ongoing challenge in market balance. The current housing inventory stands at approximately 1.3 million units, representing a 3.2 months supply at the current sales pace. This level is below the generally accepted balanced market threshold of a 6 months supply, indicating continued tightness and competition among buyers. The limited supply is exacerbated by a slowdown in new construction, with housing starts declining by 5% year-over-year, largely due to rising construction costs and labor shortages. As a result, potential buyers face intense competition, leading to frequent bidding wars and driving further price escalation in many markets.

Cap rate trends provide additional context for real estate investors. The national average cap rate is currently at 5.5%, a slight expansion from the 5.3% observed in early 2026. This trend suggests a minor easing in yield compression, as investors demand higher returns to compensate for perceived risks in the current economic climate. Despite this expansion, cap rates remain compressed relative to historical averages, indicating that investor demand for real estate assets remains strong, driven by the search for yield in a low-interest-rate environment. This dynamic highlights the ongoing attractiveness of real estate as an asset class, even as investors exercise caution amid economic uncertainties.

These metrics collectively paint a picture of a resilient yet cautious real estate market in June 2026. While mortgage rates have eased slightly, they remain elevated, impacting buyer affordability. The mortgage-treasury spread suggests a moderate risk environment, while regional variations in home prices and tight inventory levels continue to shape market dynamics. Cap rates reflect a nuanced investor sentiment, balancing yield pursuits with risk considerations.

Financing Environment & DSCR Analysis

As of June 2026, the current interest rate environment significantly impacts the Debt Service Coverage Ratios (DSCR) for property investors. With the Federal Reserve maintaining a higher interest rate stance due to inflationary pressures, average commercial mortgage rates hover around 6.5% to 7%. This rate increase directly affects the DSCR, which measures a property’s cash flow relative to its debt obligations. Typically, investors are finding that these elevated rates reduce the excess cash flow available after debt service. For instance, a property generating a net operating income (NOI) of $120,000 annually with a debt service of $100,000 now barely meets a 1.2x DSCR, which is considered riskier compared to the more desirable 1.25x or 1.35x thresholds.

The current lending environment has seen lenders tightening DSCR requirements. In previous years, a DSCR of 1.25x was often sufficient for loan approval. However, due to the increased risk perceived by lenders in the current economic climate, many financial institutions have raised their thresholds to 1.35x or higher. This shift means that properties must generate significantly more NOI relative to their debt obligations to qualify for financing. For example, at a 1.35x DSCR, the same property with a $120,000 NOI would only support approximately $88,889 in debt service, potentially requiring an investor to seek properties with higher income potential or leverage less debt.

The implications for cash flow in rental properties are profound. Consider a scenario where a multi-family unit generates $15,000 monthly in rental income with monthly expenses, including debt service, totaling $12,000. Under a 6.5% interest rate, the debt service portion might consume $8,000, leaving a pre-tax cash flow of $3,000. However, if rates were to increase slightly or if a stricter DSCR requirement necessitated a more expensive loan structure, the cash flow could diminish significantly. This decrease in free cash flow affects investors’ ability to reinvest in property improvements or distribute profits, potentially impacting the property’s long-term viability and attractiveness.

Moreover, the premiums on hard money and bridge loans have widened in response to the rate environment. These short-term financing solutions, typically used for property flips or quick acquisitions, now command interest rates ranging from 9% to 12%, depending on the borrower’s creditworthiness and the deal’s perceived risk. The higher costs associated with these loans necessitate meticulous calculation of anticipated returns to ensure profitability, especially since these loans are usually interest-only and require a robust exit strategy, such as refinancing or property sale, to be effective.

Investors must carefully consider timing when deciding to refinance versus hold properties. In the current market, holding strategies are more favorable if the existing financing terms are below market rates. However, refinancing might be attractive if it can lock in a fixed rate to hedge against future rate hikes, or if it can be structured to improve cash flow through extended terms. For instance, refinancing to a 20-year amortization schedule from a 15-year one could reduce monthly obligations, thereby improving the DSCR even if the rate is higher.

Finally, the current interest rate environment affects acquisition criteria and underwriting standards. Underwriting now requires more stringent stress-testing of interest rate impacts on DSCRs and cash flow projections. Investors are advised to adjust acquisition criteria, focusing on properties with stronger NOI growth potential or existing leases with built-in rent escalators. In practical terms, this might mean targeting properties in emerging markets or those with value-add opportunities that can offset higher financing costs through operational enhancements or rental income growth. These adjustments are essential to maintain competitive advantage and ensure sustainable investment performance in a challenging financial landscape.

Investment Strategy & Risk Management

In the evolving real estate landscape of June 2026, investors must navigate shifting market dynamics with precision. As the market continues to adjust post-pandemic, identifying the right timing for investments is crucial. Currently, the market exhibits signs of stabilization with moderate growth in property values, suggesting a cautious yet opportunistic entry point for strategic acquisitions. Investors should focus on areas with improving economic indicators and infrastructure developments, which are likely to drive future appreciation. Analyzing local market cycles and leveraging data analytics can pinpoint optimal acquisition windows, maximizing returns while minimizing exposure to volatility.

Risk factors remain prevalent in today’s environment, with rising interest rates and potential regulatory changes posing significant challenges. To mitigate these risks, investors should employ robust stress-testing techniques to evaluate the impact of interest rate fluctuations on their portfolios. Additionally, maintaining a flexible investment strategy that allows for quick adjustments can provide a buffer against unforeseen economic shifts. Ensuring sufficient liquidity and reserve funds will also help manage cash flow disruptions, thus safeguarding against abrupt market downturns.

Adjusting acquisition criteria and underwriting standards is essential in this current climate. Emphasizing conservative financial metrics such as lower leverage ratios and higher debt service coverage ratios (DSCR) can enhance portfolio resilience. By prioritizing properties with strong cash flow potential and durable demand, investors can better weather economic uncertainties. Incorporating thorough due diligence processes, including detailed market analysis and property inspections, will further mitigate acquisition risks.

For Prime Property Funding, aligning your financing products with these market insights can attract savvy investors seeking stability and growth. Offering customizable loan products that cater to varying investment horizons and risk appetites, such as fix-and-flip financing with flexible terms and DSCR loans with competitive rates, can position your services as a cornerstone of investor strategies in today’s market.

Key Considerations for Investors

- Fix-and-flip strategies: Ensure holding costs do not exceed 20% of the anticipated profit margin to maintain viability. Develop exit strategies that can accommodate a 10% market value drop.

- Buy-and-hold tactics: Target a minimum cap rate of 5% to ensure adequate returns, with rental growth assumptions limited to 3% annually to account for market variability.

- Bridge financing: Secure fixed-rate agreements where possible to hedge against expected interest rate hikes; maintain contingency reserves equal to 6 months of debt service.

- Market timing: Focus acquisitions in Q3 when holding costs typically decrease due to reduced competition, optimizing entry points.

- Geographic focus: Prioritize markets such as Austin, Raleigh, and Nashville, which offer strong employment growth and infrastructure investments, enhancing risk-adjusted returns.

- Conservative underwriting: Stress test assumptions by modeling scenarios with a 1% increase in borrowing costs and a 5% drop in rental income to ensure investment sustainability.

- Portfolio diversification: Aim for a balanced asset mix with at least 30% in multi-family units to mitigate single-sector exposure.

- Risk mitigation: Maintain insurance coverage that includes loss-of-rents clauses, and perform annual property condition assessments to preemptively address potential issues.

By applying these strategies and considerations, investors can position themselves to capitalize on current market opportunities while effectively managing risks. This proactive approach will not only safeguard investments against unpredictability but also enable substantial growth and profitability.

Resources

External References

Disclaimer: This market analysis is for informational purposes only and should not be considered financial or investment advice. Market conditions can change rapidly. Consult with a qualified financial or lending professional before making any decisions.