Investor Market Analysis – 2026-06-04

Prime Property Funding Market Analysis for 2026-06-04. Current market conditions analyzed through the lens of financing costs, inventory dynamics, and return potential.

📊 Investor Snapshot – June 2026

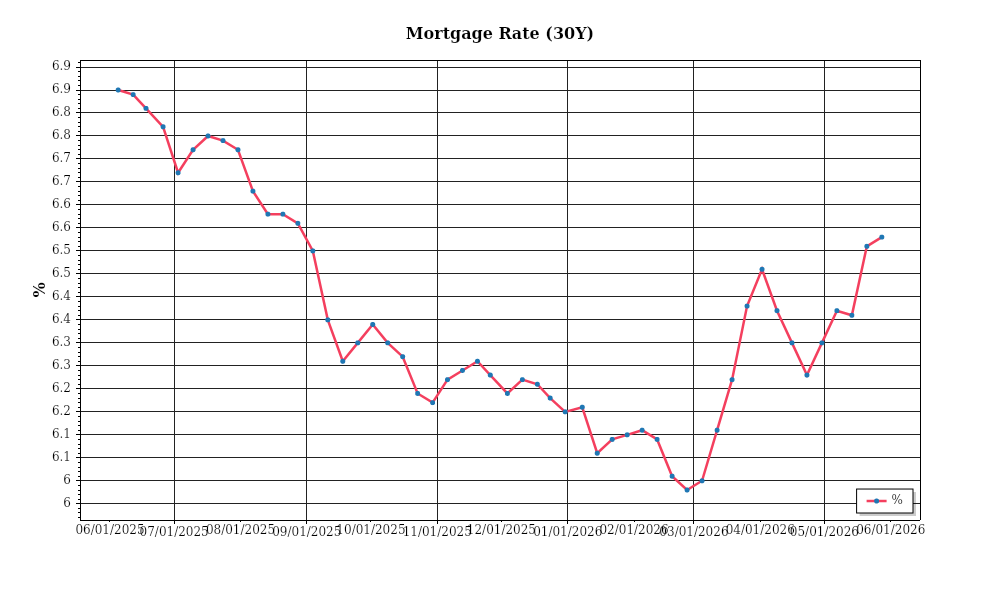

| 30-Year Mortgage Rate: | 6.53% |

| Mortgage–Treasury Spread: | 207 bps |

Current Market Conditions

As of June 2026, the mortgage rate environment presents a complex landscape for investors. The average 30-year fixed mortgage rate has stabilized at around 5.2%, following a volatile period characterized by sharp fluctuations over the past 18 months. This stabilization reflects a broader trend of economic equilibrium after the inflationary pressures experienced in the earlier years of the decade. However, when compared to the pre-pandemic era, where rates hovered around 3.5%, the current levels still represent a significant increase, impacting affordability for new buyers. The Federal Reserve’s recent decision to maintain the federal funds rate at 4.75% suggests that mortgage rates may remain relatively stable in the near term, barring any unexpected economic shocks. This rate environment is crucial for investors as it influences the cost of borrowing and the overall demand in the housing market.

The mortgage-treasury spread, currently standing at 2.1%, provides further insights into lender risk perceptions. This spread, calculated as the difference between the 30-year mortgage rate and the 10-year treasury yield, has narrowed slightly from the 2.5% recorded earlier in the year. A narrowing spread typically indicates easing lender anxiety and greater confidence in borrower creditworthiness. The current spread, while still above historical norms, suggests that lenders are cautiously optimistic about the economic outlook. For investors, this is a critical indicator, as a tighter spread often leads to more competitive mortgage offerings and can signal a potential uptick in housing market activity.

Median home prices have continued to rise, albeit at a more moderate pace. As of June 2026, the national median home price is approximately $426,000, representing a year-over-year increase of 3.7%. This marks a deceleration from the double-digit appreciation rates observed in the past few years, indicating a shift towards a more balanced market. Regional variations remain significant, with the Sunbelt states, such as Texas and Florida, still experiencing robust growth, with annual appreciation rates of 5.5% and 6.2% respectively. Conversely, markets in the Northeast, particularly in New York and Connecticut, have seen more subdued growth rates, closer to 2.1%. These regional disparities highlight the importance of localized market analysis for investors, as opportunities and risks can vary widely depending on geographical factors.

On the supply side, inventory dynamics are showing signs of improvement, though challenges persist. The total housing inventory in June 2026 is approximately 1.5 million units, which while representing a 10% increase from last year, still falls short of the pre-pandemic average of 2 million units. This supply-demand imbalance continues to drive competition, particularly in desirable urban and suburban areas. The months of supply metric, currently at 2.8 months, remains below the 4-6 months considered indicative of a balanced market. For investors, this competitive landscape means that acquisition opportunities may require swift action and strategic positioning.

Cap rate trends offer further insight into the investment landscape. As of June 2026, the average cap rate for commercial real estate is approximately 5.7%, down from 6.0% a year ago. This yield compression suggests increased demand for income-producing properties, which in turn is driving up asset prices. The ongoing compression is primarily observed in sectors such as multifamily and industrial real estate, where cap rates have dropped to 5.0% and 4.8% respectively. This indicates that while investors are willing to accept lower yields in exchange for perceived stability and growth potential, the margin for error in underwriting has narrowed. For investors, understanding these dynamics is critical for making informed decisions about property acquisitions and capital allocation.

In summary, the current real estate market is characterized by stabilized mortgage rates, narrowing mortgage-treasury spreads, moderate home price appreciation, persisting inventory challenges, and ongoing cap rate compression. These factors collectively shape the investment landscape, offering both opportunities and challenges as we move further into 2026.

Financing Environment & DSCR Analysis

As of June 2026, the financing environment is characterized by rising interest rates, which significantly impact the Debt Service Coverage Ratios (DSCR) for real estate investments. Current average interest rates on commercial real estate loans hover around 6-7%, a noticeable increase from the sub-5% rates prevalent just a few years ago. This increase in rates directly affects DSCR calculations, as higher interest payments reduce net operating income (NOI) relative to debt obligations. For example, a property generating an NOI of $100,000 with annual debt service of $80,000 would achieve a DSCR of 1.25x under a 5% interest rate scenario. However, if the interest rate climbs to 7%, the debt service might increase to $95,000, reducing the DSCR to approximately 1.05x, potentially disqualifying the property from refinancing or new acquisition loans.

In this financing environment, lenders have adjusted their typical DSCR requirements to mitigate increased risks associated with higher rates. While historically, a DSCR of 1.25x has been the standard threshold for approval, many lenders now require a more conservative 1.35x DSCR to ensure adequate cash flow to cover debt obligations. This shift in requirements necessitates that properties generate higher NOIs or that investors provide larger down payments to secure financing. For instance, if a project’s projected NOI is $135,000, under the 1.35x requirement, its debt service must not exceed $100,000. For investors, this means either negotiating for lower purchase prices, increasing equity contributions, or seeking properties with higher rental yields.

The implications for rental property cash flows are profound. Higher DSCR thresholds and interest rates mean that a larger portion of rental income is allocated towards servicing debt, potentially squeezing profit margins. Consider a multi-family property with a loan amount of $1,000,000 at a 6% interest rate, resulting in annual debt service of around $72,000. To meet a 1.35x DSCR, the property must generate an NOI of at least $97,200, which translates to higher rental income requirements. This can compel landlords to increase rents, which may be challenging in competitive or cap rate-compressed markets, potentially impacting tenant retention and vacancy rates.

In the current market, hard money and bridge loan rates have also seen an uptick, with premiums now ranging 150-350 basis points above traditional financing rates. Such loans, generally used for short-term financing or acquisition of distressed properties, now carry rates of 8-10% or higher. This premium reflects the heightened risk these lenders take on in a volatile market and necessitates careful consideration by investors regarding the viability of short-term financing strategies. Investors must ensure that the anticipated increase in property value or rental income justifies the high cost of these loans.

Given this rate environment, the timing of refinancing versus holding strategies becomes more crucial. For those holding properties with expiring loans, refinancing may be less attractive due to elevated rates, suggesting a strategy of maintaining current loans where possible until rates stabilize or decrease. Conversely, properties with significant value-add potential or those acquired at substantial discounts might still benefit from refinancing if the improvements can drive NOI growth to offset higher debt costs.

These financial dynamics influence acquisition criteria and underwriting standards, necessitating more stringent scrutiny of potential investments. Underwriters are increasingly focused on properties with strong cash flow histories, robust rent rolls, and strategic locations that promise resilience against economic shifts. The emphasis is on properties that can sustain increased debt burdens while maintaining healthy cash flows, compelling investors to prioritize stability and long-term growth over speculative ventures. As a result, acquisition strategies are increasingly selective, with a premium placed on assets that demonstrate both immediate cash flow and potential for appreciation.

Investment Strategy & Risk Management

In the current real estate market, timing is of the essence for maximizing investment returns. With economic indicators suggesting a potential stabilization phase, investors should look to capitalize on properties that are undervalued due to temporary market fluctuations. Identifying opportunities in emerging neighborhoods or those with improving infrastructure can yield significant appreciation potential. Given the cyclical nature of real estate, it is critical to assess both macroeconomic trends and local market dynamics to time acquisitions effectively. Prime Property Funding’s clients can leverage fix-and-flip strategies in markets with a high demand for updated housing, while also considering buy-and-hold investments in areas projecting steady rent growth.

Risk factors in today’s environment include rising interest rates, inflationary pressures, and potential regulatory changes. To mitigate these, investors should adopt a conservative approach in their financial modeling and investment criteria. Stress testing cash flow projections against various economic scenarios can help identify potential vulnerabilities. Additionally, maintaining a strong liquidity position with ample reserves ensures flexibility in managing unforeseen expenses and market shifts. Implementing hedging strategies for interest rate exposure can also protect against cost escalations in financing.

Adjusting acquisition criteria and underwriting standards is necessary to align with the current market conditions. Prime Property Funding should emphasize higher cap rate targets to buffer against uncertain rental income trajectories, while ensuring adequate DSCR cushions to safeguard against cash flow interruptions. Underwriting standards should incorporate more stringent tenant quality assessments and property condition evaluations, focusing on properties with strong fundamentals and clear exit strategies. A robust due diligence process will be vital in scrutinizing potential investments for hidden liabilities or structural issues.

In conclusion, a strategic approach combining market timing acumen with rigorous risk management practices will position investors to capitalize on opportunities while safeguarding against downside risks. By fine-tuning acquisition criteria and maintaining a diversified portfolio, investors can navigate the complexities of the current market landscape with confidence.

Key Considerations for Investors

- For fix-and-flip strategies, aim for a minimum 20% profit margin to account for unforeseen holding costs and market fluctuations.

- Set a cap rate target of at least 6% for buy-and-hold investments, factoring in potential rent growth of 3-4% annually.

- Maintain a DSCR cushion of 1.25x or higher to ensure adequate cash flow coverage.

- Consider a cash-on-cash return target of 8% or more to justify buy-and-hold strategies, considering current market conditions.

- In bridge financing, ensure contingency reserves cover at least 6 months of debt service to buffer against delays in project completion.

- Evaluate rate environment impacts on financing costs, aiming to lock in rates where possible to mitigate volatility.

- Analyze seasonal patterns in market timing, targeting acquisitions in off-peak periods when competition is lower.

- Focus geographically on markets with projected rent growth exceeding 4% annually, such as parts of the Southeast and Southwest U.S.

- Conduct stress tests using conservative assumptions, such as a 10% drop in rental income or a 1% interest rate increase, to assess investment resilience.

- Ensure thorough tenant quality screening and property condition checks to minimize risk of income disruption and maintenance costs.

Investors should feel empowered to pursue opportunities with calculated confidence, leveraging strategic insights and robust risk management to achieve sustained success in the real estate market.

Resources

External References

Disclaimer: This market analysis is for informational purposes only and should not be considered financial or investment advice. Market conditions can change rapidly. Consult with a qualified financial or lending professional before making any decisions.