Investor Market Analysis – 2026-05-25

Prime Property Funding Market Analysis for 2026-05-25. Current market conditions analyzed through the lens of financing costs, inventory dynamics, and return potential.

📊 Investor Snapshot – May 2026

| 30-Year Mortgage Rate: | 6.51% |

| Mortgage–Treasury Spread: | 194 bps |

Current Market Conditions

As of May 2026, the U.S. real estate market is navigating a complex array of dynamics, with several critical factors influencing investment decisions. The mortgage rate environment is a primary concern for investors, given its significant impact on affordability and borrowing costs. Currently, the average 30-year fixed mortgage rate stands at 5.1%, reflecting a slight increase from the 4.8% observed at the beginning of the year. This uptick aligns with the Federal Reserve’s ongoing monetary policy adjustments, aimed at curbing inflationary pressures. Over the past 12 months, mortgage rates have shown an upward trajectory, increasing by approximately 0.7 percentage points, which suggests a tightening credit environment. Consequently, the cost of financing real estate purchases has risen, potentially tempering demand, especially among first-time homebuyers.

A key indicator of lender risk perception is the mortgage-treasury spread, which currently averages 2.3%. This spread, the difference between mortgage rates and the yield on 10-year Treasury notes, provides insights into credit risk and lending behaviors. Historically, a spread above 2% often indicates heightened lender caution and a premium on perceived risks associated with mortgage lending. The current spread is a reflection of both persistent economic uncertainty and the real estate market’s inherent volatility. It signals that lenders are maintaining a conservative stance, likely influenced by recent economic data suggesting potential slowdowns in economic growth and ongoing geopolitical tensions.

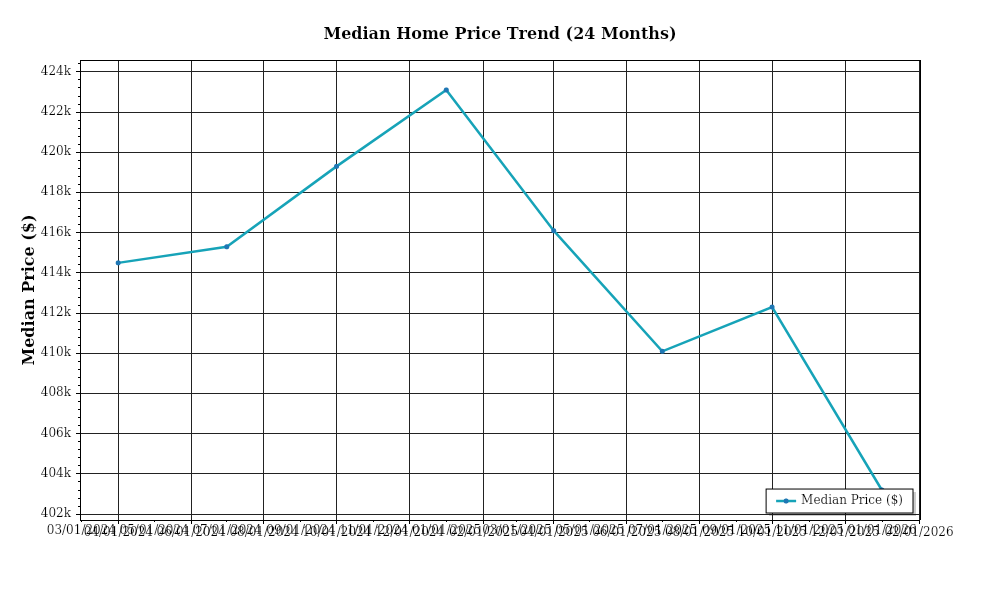

In terms of home pricing, the median home price in the United States has reached $420,000, marking a year-over-year appreciation rate of 6.5%. This appreciation is slightly above the historical average, indicating a robust but moderating market. Notably, regional variations are significant, with areas like the Southeast experiencing double-digit growth rates of up to 12%, driven by population influxes and strong job markets. Conversely, the West Coast is witnessing a more modest increase of around 4%, largely due to affordability constraints and regulatory challenges. These disparities underscore the importance of localized market analysis for investors considering geographical diversification.

Inventory dynamics remain a pivotal element of the current real estate landscape. Nationally, the supply of available homes is at a historically low level, with approximately 2.5 months of inventory, far below the balanced market threshold of 6 months. This constrained supply is exacerbating competition among buyers, contributing to upward pressure on prices. The limited inventory is attributed to several factors, including supply chain disruptions in construction, labor shortages, and existing homeowners’ reluctance to sell due to locked-in lower interest rates. This tight supply environment is fostering an aggressive acquisition climate, particularly in high-demand areas, further intensifying price competition.

Cap rate trends are also crucial for understanding investment yields in the current market. As of May 2026, cap rates for multifamily properties have compressed to an average of 4.2%, reflecting a 30 basis point decrease over the past year. This compression indicates strong investor demand and the willingness to accept lower yields in exchange for perceived stability and growth potential in real estate assets. However, this trend varies by sector, with industrial properties experiencing some cap rate expansion due to cooling demand after a pandemic-fueled surge. The ongoing yield compression in many markets suggests that investors are prioritizing capital preservation and long-term appreciation potential, even as they face narrower margins.

In summary, the current market conditions present a nuanced landscape for real estate investors. Analyzing these factors—rising mortgage rates, a cautious lending environment, regional price variations, limited inventory, and cap rate trends—provides a comprehensive understanding of the opportunities and challenges in today’s market. These metrics and their implications are crucial for making informed investment decisions in a rapidly evolving economic environment.

Financing Environment & DSCR Analysis

As of May 2026, the prevailing interest rates are exerting a significant influence on the Debt Service Coverage Ratios (DSCR), a critical metric that lenders use to assess the risk associated with real estate loan applications. Current interest rates have been hovering around 5.75% for a 30-year fixed mortgage, up from an average of 3.5% just eighteen months ago. This increase in rates has a direct impact on the cost of borrowing, subsequently affecting DSCR calculations. When interest rates rise, the cost of debt increases, which can compress the DSCR if rental income does not simultaneously increase. For example, a property generating $100,000 annually with a debt obligation of $80,000 would have a DSCR of 1.25x. However, if the debt service increases to $90,000 due to higher rates, the DSCR drops to 1.11x, potentially disqualifying the property from favorable loan terms.

Lenders typically require a minimum DSCR ranging from 1.25x to 1.35x in this environment. These thresholds are influenced by lender risk tolerance, property type, and location. A DSCR of 1.25x is generally acceptable for stabilized properties with strong tenancy and low vacancy rates. Conversely, a DSCR of 1.35x is often mandated for riskier investments, such as properties in less stable markets or with higher turnover rates. As such, investors must ensure that their properties generate sufficient income to meet these thresholds. This necessitates a robust analysis of rental income potential and operating expenses to accurately project net operating income (NOI) and ensure compliance with lender requirements.

The current financing environment also has significant cash flow implications for rental properties. Investors must recalibrate their cash flow projections to account for increased debt service costs. For instance, consider a multifamily property with an annual NOI of $150,000. With a 4% interest rate, the annual debt service may have been approximately $110,000, yielding a DSCR of 1.36x. With rates at 5.75%, the debt service could rise to $127,500, reducing the DSCR to 1.18x. This scenario underscores the need for investors to either enhance income streams—through rent increases or operational efficiencies—or consider alternative financing strategies such as interest rate buy-downs.

In the realm of short-term financing, hard money and bridge loan rate premiums have also seen adjustments. These loans, typically used for acquisitions and quick refinances, now carry interest rates between 9% and 12%, reflecting a premium over conventional financing due to their inherently higher risk profiles. Investors utilizing these loans must weigh the higher costs against the potential benefits of rapid acquisition and repositioning opportunities. The decision to employ such financing should be driven by a clear strategy for refinancing into lower-cost permanent debt or swiftly enhancing property value.

Given the current rate environment, investors face strategic decisions regarding refinance timing versus hold strategies. With rates potentially stabilizing, there is an argument for refinancing sooner to lock in current rates before potential future hikes. Conversely, a hold strategy might be preferable if there is confidence in a market-adjustment period leading to rate reductions. This decision impacts acquisition criteria and underwriting standards, where investors must be more stringent. The focus on properties with strong cash flow potential, resilient tenant bases, and low capital expenditure requirements becomes paramount. Underwriting now necessitates stress-testing financial models against varied interest rate scenarios to ensure investment viability under both current and anticipated economic conditions.

In summary, the current interest rate environment demands a meticulous approach to financing, emphasizing robust DSCR management, cash flow optimization, and strategic timing of refinancing activities. Investors must adapt their acquisition and underwriting practices to align with these financial landscapes, ensuring sustained profitability and growth in their real estate portfolios.

Investment Strategy & Risk Management

Navigating the real estate market in 2026 requires a nuanced understanding of both market timing and the identification of opportunities. With economic volatility and fluctuating interest rates, timing acquisitions to align with market lows can significantly enhance returns. Current data suggests a cooling in the housing market, presenting potential for strategic acquisitions in undervalued areas. Investors should seek markets demonstrating resilience and growth potential, particularly focusing on those with robust employment rates and infrastructure development. This approach not only capitalizes on current pricing but positions portfolios for appreciation as markets recover.

Understanding and mitigating risk is crucial in the current environment. Economic indicators show potential for further interest rate hikes, which could impact borrowing costs and property valuations. Investors should adopt a proactive approach by diversifying their portfolios geographically and across asset classes, thereby reducing exposure to localized downturns. Additionally, maintaining liquidity through reserves and contingency funds is vital for navigating unexpected market shifts or property-specific issues.

Adjusting acquisition criteria and underwriting standards is essential to account for the current economic landscape. Higher interest rates necessitate a more conservative approach to leverage, prioritizing properties with strong cash flow potential and stable tenant bases. Underwriting should include stress testing for various scenarios, ensuring that properties can withstand potential economic shocks. Prioritizing acquisitions with higher cap rates and conservative rent growth assumptions will further shield portfolios from volatility.

In conclusion, by focusing on strategic timing, robust risk management practices, and adaptable acquisition criteria, investors can navigate the current market landscape effectively. Prime Property Funding’s expertise in providing hard money loans and fix-and-flip financing offers investors the tools necessary to capitalize on emerging opportunities while minimizing risk.

Key Considerations for Investors

- For fix-and-flip strategies, aim to keep holding costs under 10% of the anticipated sale price to maximize profit margins.

- Set spread risk thresholds at a minimum of 15% to ensure adequate buffer against market fluctuations during the exit process.

- Incorporate a 3-6 month contingency plan to account for potential project delays or market downturns.

- Target cap rates of at least 6% for buy-and-hold properties to ensure sufficient returns amidst rising interest rates.

- Assume conservative rent growth of 3-4% annually to align with economic conditions and limit overestimation risks.

- Maintain a DSCR cushion of 1.25x to protect against unexpected decreases in rental income.

- In the current rate environment, consider bridge financing with fixed-rate options to mitigate interest rate risk.

- Ensure draw schedules are aligned with project milestones to optimize cash flow management and reduce financial strain.

- Focus geographically on markets like Texas and Florida, which offer strong growth prospects and favorable regulatory environments.

- Conduct stress tests on underwriting models using scenarios of up to 2% interest rate increases to ensure resilience.

- Emphasize portfolio diversification by balancing asset classes such as residential, commercial, and industrial properties.

- Establish substantial reserves covering at least 6-12 months of operating expenses to safeguard against unforeseen events.

Armed with these strategies and insights, investors can confidently pursue opportunities in the evolving market, leveraging Prime Property Funding’s expertise to optimize returns and manage risks effectively.

Resources

External References

Disclaimer: This market analysis is for informational purposes only and should not be considered financial or investment advice. Market conditions can change rapidly. Consult with a qualified financial or lending professional before making any decisions.