Investor Market Analysis – 2026-05-24

Prime Property Funding Market Analysis for 2026-05-24. Current market conditions analyzed through the lens of financing costs, inventory dynamics, and return potential.

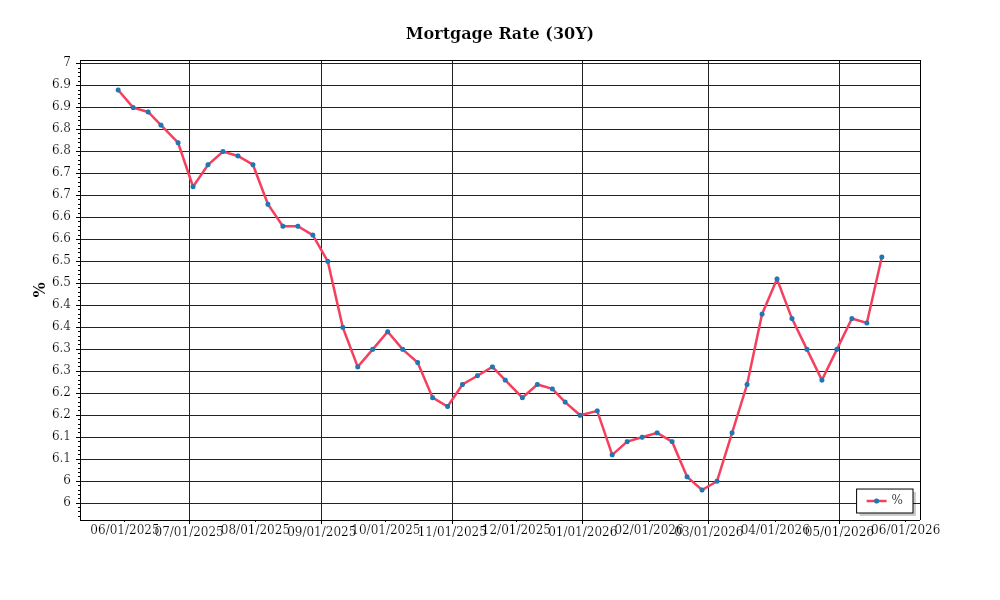

📊 Investor Snapshot – May 2026

| 30-Year Mortgage Rate: | 6.51% |

| Mortgage–Treasury Spread: | 194 bps |

Current Market Conditions

As of May 2026, the U.S. real estate market is navigating a complex landscape influenced by evolving mortgage rates, shifting price trends, and inventory dynamics. The average 30-year fixed mortgage rate stands at 5.1%, representing a decrease from the post-pandemic highs of over 6.5% in 2023. This downward trend began in late 2024, driven by adjustments in monetary policy aimed at stabilizing economic growth. The Federal Reserve’s decision to maintain a more dovish stance has helped ease borrowing costs. However, the trajectory suggests a plateauing of rates as inflationary pressures remain a concern. This potential stabilization is significant for prospective homeowners and investors, indicating relatively favorable borrowing conditions compared to recent years.

The mortgage-treasury spread, an indicator of lender risk perception, currently averages 1.8%, slightly above the historical norm of 1.5%. This spread, which represents the difference between mortgage interest rates and the yield on 10-year Treasury notes, suggests that lenders are factoring in additional risks. These include potential economic slowdowns and the ongoing geopolitical uncertainties that could impact global markets. A higher spread signals that lenders are cautious, potentially leading to tighter underwriting standards. For investors, this means that while mortgage rates are relatively low, accessing capital might involve more stringent qualification criteria.

In terms of housing prices, the national median home price is now at $415,000, reflecting a year-over-year appreciation rate of 3.5%. This marks a deceleration from the double-digit growth rates observed in the early 2020s. Regional variations are pronounced; for instance, the Sun Belt region, particularly cities like Phoenix and Austin, continues to experience robust growth with appreciation rates of 5-6%. In contrast, coastal markets such as San Francisco and New York City are witnessing more modest increases of 1-2%, as high living costs and remote work trends influence demand. This data underscores a shift towards more affordable and spacious living environments, impacting investment strategies.

Inventory levels remain a critical component of the current market conditions. As of May 2026, the total housing inventory is approximately 1.3 million units, which translates to a supply of 3.4 months at the current sales pace. This figure indicates a market still favoring sellers, though it represents an improvement from the tight conditions of 2022 when supply dipped below 2 months. The increase in inventory is partly due to the slowdown in price appreciation, which has encouraged more homeowners to list their properties. For investors, this means increased competition for acquisitions, but also more opportunities to negotiate favorable terms as the market gradually shifts towards a balanced state.

Finally, cap rate trends provide insight into commercial real estate dynamics. The average cap rate for prime properties across major U.S. markets is currently around 5.2%, a slight increase from the historical lows of under 4.5% in 2021. This rise indicates a slight yield expansion, suggesting that property prices are stabilizing relative to rental income. Investors should note that while cap rates are rising, they remain low by historical standards, reflecting continued strong demand for income-producing properties. This environment necessitates a careful assessment of potential returns, especially in secondary and tertiary markets where cap rate compression has been less pronounced.

Overall, the current market conditions present a nuanced picture. The interplay of mortgage rates, price trends, and inventory dynamics requires investors to adopt a strategic approach, balancing the opportunities presented by lower borrowing costs with the challenges of tighter inventory and shifting regional demand patterns.

Financing Environment & DSCR Analysis

As of May 2026, the financing environment is characterized by relatively high interest rates that significantly impact the Debt Service Coverage Ratios (DSCR) of real estate investments. Current rates for conventional loans hover around 6.5-7%, which exert upward pressure on the debt servicing costs of property owners. A higher interest rate environment means that the monthly debt obligations increase, thereby reducing the DSCR unless offset by higher rental income. The DSCR is a critical metric used by lenders to assess the risk of a loan; it measures the cash available to service debt against the debt obligations. When interest rates rise, it becomes challenging for properties with marginal cash flows to maintain a healthy DSCR.

In this environment, lenders typically require a DSCR of at least 1.35x, as opposed to the more lenient 1.25x that might be acceptable in lower rate environments. This shift reflects lenders’ increased caution, given the higher cost of borrowing and the uncertainty surrounding future rate movements. The stricter requirement means that properties must generate $1.35 in income for every dollar of debt service, as opposed to $1.25 previously. For instance, consider a rental property with an annual debt obligation of $100,000. Under a 1.35x DSCR requirement, the property must generate at least $135,000 in net operating income (NOI), compared to $125,000 under the 1.25x requirement. This higher threshold limits borrowing capacity and may necessitate increased equity contributions or higher rental revenues to secure financing.

Cash flow implications for rental properties are profound. Assume a multifamily property with a monthly rental income of $50,000 and operating expenses of $20,000, leaving an NOI of $30,000. With a monthly debt service of $22,000, the DSCR is 1.36x. If interest rates increase, raising the debt service to $25,000, the DSCR drops to 1.20x, falling short of the 1.35x requirement. Investors must either increase rental income, reduce operating expenses, or inject additional equity to maintain acceptable DSCR levels. This environment pressures property owners to optimize operations and, potentially, adjust tenant lease structures to ensure stable and increasing cash flows.

Hard money and bridge loan rate premiums are significant in the current market. These short-term financing options command rates often above 10%, reflecting their higher risk and the speed at which they can be deployed. Investors using these financing options must carefully weigh the cost against the potential upside of rapid acquisition or repositioning strategies. The premiums for these loans are justified by their flexibility, but they necessitate exit strategies that align closely with broader market conditions, especially given the elevated interest rates.

The decision to refinance versus hold is a critical consideration in this rate environment. With rates predicted to stabilize rather than decrease, investors who can lock in lower rates now may benefit in the long run, despite potential prepayment penalties. Conversely, a hold strategy may be prudent for properties with long-term fixed-rate debt already in place, avoiding the risks associated with refinancing at current elevated rates. Timing is crucial; investors must assess whether the anticipated benefits from refinancing—such as improved cash flow or access to capital for renovations—outweigh the costs and risks.

The current rate environment also affects acquisition criteria and underwriting standards. Investors must adjust their acquisition strategies to account for higher financing costs, which may compress cap rates and affect valuations. Underwriting standards have tightened, with increased scrutiny on income stability and growth potential. This means that properties with strong cash flow histories and potential for rent increases are more attractive. Additionally, the emphasis on higher DSCRs in underwriting compels investors to be more selective, focusing on assets that can sustain higher debt costs while maintaining robust cash flows.

Investment Strategy & Risk Management

In the current economic climate of May 2026, characterized by moderate interest rates and a competitive real estate market, investors must strategically time their market entry to capitalize on cyclical opportunities while minimizing exposure to risk. With economic signals suggesting a potential stabilization in property prices, now is an optimal time for investors to consider acquisitions that could benefit from future appreciation. However, caution is advised as there are still variances across different geographic regions and asset classes. Investors should focus on neighborhoods and sectors that exhibit strong fundamentals such as employment growth, infrastructure developments, and favorable demographic trends.

Risk factors in the current environment include potential interest rate hikes and fluctuating property values, which can significantly impact both acquisition costs and exit strategies. To mitigate these risks, it is crucial for investors to implement robust underwriting standards that stress-test potential acquisitions against various economic scenarios. This includes maintaining conservative loan-to-value ratios and ensuring that properties can withstand potential downturns in rental income or market value. Additionally, investors should diversify their portfolios geographically and across asset classes to spread risk and ensure that no single investment disproportionately affects the overall portfolio.

Adjusting acquisition criteria to align with current market conditions is imperative. Investors should prioritize properties with strong cash flow potential and robust cap rates to ensure short-term liquidity and long-term profitability. For fix-and-flip strategies, it’s important to maintain a buffer for holding costs and prepare for longer-than-expected holding periods due to market fluctuations. For buy-and-hold strategies, focusing on properties with high DSCR and cash-on-cash returns will offer a cushion against potential economic uncertainties.

By adopting these strategic measures, investors can effectively navigate the complexities of the current real estate market. Prime Property Funding can support these strategies by offering flexible financing solutions tailored to the unique needs of investors, whether through hard money loans, fix-and-flip financing, or DSCR loans. With a proactive approach to market timing and risk management, investors can position themselves to maximize returns while safeguarding their investments.

Key Considerations for Investors

- Fix-and-flip strategies: Ensure holding costs do not exceed 10% of projected profits, and plan for a 20% spread to buffer against market volatility.

- Buy-and-hold tactics: Target properties with a minimum cap rate of 6% and incorporate a 3% annual rent growth assumption to ensure sustainable returns.

- DSCR cushions: Maintain a minimum DSCR of 1.25 to ensure adequate coverage of debt obligations and mitigate potential income disruptions.

- Bridge financing: Structure draw schedules to coincide with project milestones, and maintain a contingency reserve of at least 5% of total project costs.

- Market timing: Identify acquisition opportunities during off-peak seasons to benefit from reduced competition and potentially lower purchase prices.

- Geographic focus: Prioritize investments in markets with projected employment growth above 2% annually, such as Austin, Nashville, and Charlotte, for superior risk-adjusted returns.

- Conservative underwriting: Stress-test assumptions by simulating a 1.5% increase in interest rates and a 10% decrease in property values to assess resilience.

- Portfolio diversification: Balance the asset class mix with no more than 30% concentration in any single category or geographic area to reduce exposure.

- Risk mitigation: Establish reserves covering at least 6 months of operating expenses, ensure comprehensive insurance coverage, and rigorously vet tenant quality.

- Exit strategies: Develop multiple exit strategies, including sale, refinancing, or rental, to accommodate shifting market conditions and protect investments.

By following these detailed guidelines, investors can confidently navigate the real estate landscape, leveraging both opportunities and protective measures to achieve sustained success.

Resources

External References

Disclaimer: This market analysis is for informational purposes only and should not be considered financial or investment advice. Market conditions can change rapidly. Consult with a qualified financial or lending professional before making any decisions.