Investor Market Analysis – 2026-05-17

Prime Property Funding Market Analysis for 2026-05-17. Current market conditions analyzed through the lens of financing costs, inventory dynamics, and return potential.

📊 Investor Snapshot – May 2026

| 30-Year Mortgage Rate: | 6.36% |

| Mortgage–Treasury Spread: | 189 bps |

Current Market Conditions

As of May 2026, the real estate market is navigating through a complex landscape influenced by several economic factors, with mortgage rates being a significant determinant. The average 30-year fixed mortgage rate currently stands at 5.7%, slightly down from 5.9% in April 2026, marking a subtle yet noteworthy decline. This decrease follows a broader trend seen over the past six months, where rates have fluctuated within the 5.5% to 6.0% range. The Federal Reserve’s cautious stance on interest rates, coupled with moderate inflation rates, has contributed to this stabilization. Analysts project that mortgage rates may continue to hover around this level for the remainder of the year, barring any significant economic disruptions. This environment provides a mixed bag for investors—while lower rates can enhance purchasing power, they also compress potential yields on investments.

Understanding the mortgage-treasury spread is crucial for assessing lender risk perception. Currently, the spread between the 30-year fixed mortgage rate and the 10-year Treasury yield is approximately 2.0%, a slight contraction from 2.3% observed in early 2026. This tightening indicates a reduction in perceived risk by lenders, potentially due to stabilizing economic indicators and improved borrower credit profiles. Historically, a narrower spread suggests lenders are more confident in the economic outlook, reducing the risk premium required for mortgages. For investors, this contraction hints at a more competitive lending environment, which could lead to more favorable borrowing conditions but also signals a cautionary note on risk assessments.

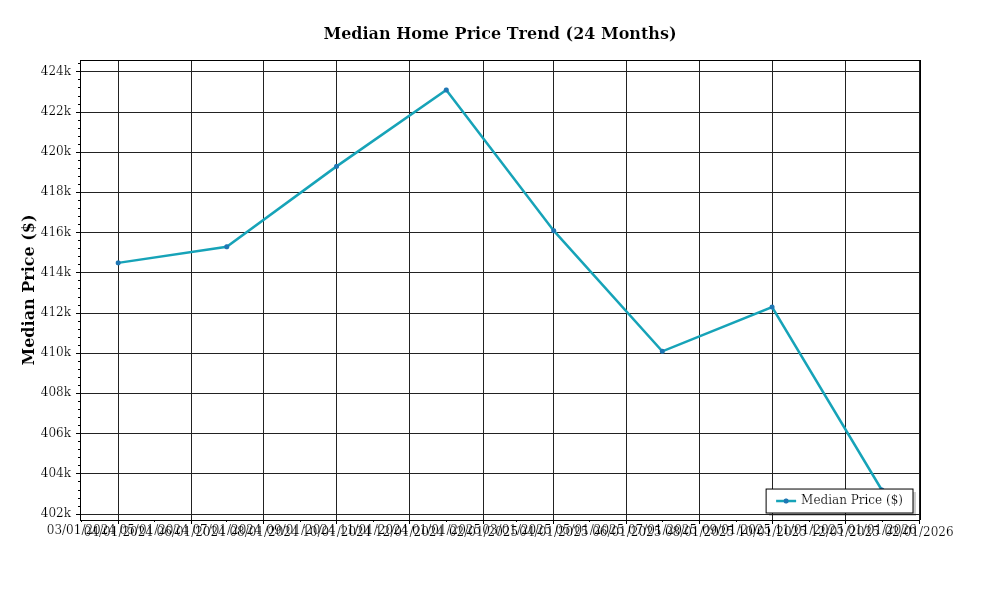

The median home price in the United States has seen a significant increase, currently at $425,000, reflecting a year-over-year appreciation rate of 8.2%10% year-over-year. In contrast, the Midwest has seen more modest increases, averaging around 4.5%. The appreciation is driven by persistent demand, especially in urban areas with limited supply, and a steady influx of high-income earners into tech-centric regions. For investors, this data underscores the potential for capital gains in certain markets, though it also elevates the entry cost, which could affect long-term ROI calculations.

Inventory dynamics continue to challenge market equilibrium. Nationwide housing inventory is currently estimated at 3.4 months of supply, significantly below the balanced market benchmark of 6 months. This shortage is most acute in suburban markets, where supply has dwindled to 2.8 months. The competitive environment is further evidenced by the average days on market, which has decreased to 28 days from 35 days at the beginning of the year. This constrained supply, coupled with robust demand, particularly from millennial buyers, underscores a seller’s market, driving up prices and creating challenging conditions for acquisitions. Investors need to be strategic in their acquisitions, with an emphasis on emerging suburbs where supply constraints might ease in the future.

Cap rate trends provide additional insights into the real estate investment landscape. Currently, cap rates for multifamily properties average at 4.8%, down from 5.1% in May 2025. This compression is indicative of heightened demand and competition amongst investors, largely fueled by the relative safety and stable returns of real estate compared to volatile equities. However, the compression also implies reduced future yield potential, compelling investors to focus on value-add opportunities or markets with higher growth potential. In contrast, industrial properties have seen a slight cap rate expansion to 5.6%, driven by increased supply chain resilience demands, offering a more attractive yield for risk-tolerant investors. These shifts highlight the importance of sector-specific strategies in optimizing investment portfolios.

Financing Environment & DSCR Analysis

In May 2026, the prevailing interest rates present a complex landscape for real estate investors, directly impacting the Debt Service Coverage Ratios (DSCR). As interest rates hover around 5.75% for standard commercial loans, up from the previous few years, this increase exerts pressure on DSCR calculations. The DSCR, which measures the cash flow available to pay current debt obligations, becomes tighter as borrowing costs rise, necessitating higher rental incomes to maintain the same coverage ratios. For instance, a property generating $150,000 in annual net operating income (NOI) with $120,000 in annual debt service would previously have a DSCR of 1.25x. However, with increased rates, the debt service amount could rise to approximately $132,000, reducing the DSCR to 1.14x, potentially falling below lender thresholds.

In this environment, lenders typically require a DSCR of 1.35x to provide a buffer against income fluctuation and interest rate risks. This is a shift from the 1.25x threshold that was more common when rates were lower. The increased requirement means that properties must generate higher NOI or have lower financing amounts to meet this stricter standard. Consequently, investors must either enhance property income streams or re-evaluate acquisition prices to ensure compliance with these tighter lending standards.

The cash flow implications for rental properties are significant. With higher interest obligations, cash flow margins become slimmer. For example, consider a multi-family property with an NOI of $200,000. Under previous conditions with a DSCR requirement of 1.25x, the maximum allowable annual debt service would be $160,000. At the current 1.35x requirement, the allowable debt service drops to approximately $148,148, assuming all other factors remain constant. This change either necessitates a reduction in loan amount or an increase in down payment, both of which affect the overall investment return. Investors must strategically enhance rental income, possibly by upgrading units to justify rent increases or by exploring additional revenue streams such as parking fees or amenity charges.

For those seeking alternative financing options, hard money and bridge loans present an enticing albeit costly choice. These short-term financing solutions carry a premium, with rates often 200-300 basis points higher than conventional loans, currently ranging between 8% and 10%. While these loans offer flexibility and speed, the cost can significantly affect project profitability unless the investor has a clear exit strategy, such as a quick property flip or leasing turnaround.

When considering refinancing versus holding strategies, the timing plays a crucial role given the current rate environment. Refinancing to lock in current rates could be beneficial if future rate hikes are anticipated. However, this strategy might not be optimal if rates are projected to stabilize or decrease. The decision hinges on the investor’s cash flow projections and exit strategy. A hold strategy might be more prudent if the investor anticipates stable long-term income streams and rates, thus avoiding the costs associated with refinancing.

Finally, the impact on acquisition criteria and underwriting standards is pronounced. With higher DSCR requirements, cap rates are under pressure to adjust, influencing property valuations and acquisition bids. Underwriting standards have tightened, with lenders scrutinizing income stability, historical vacancy rates, and market trends more rigorously. Investors must adapt by conducting detailed market analyses, focusing on properties with strong, reliable cash flows, and considering geographic diversification to mitigate localized economic risks. This meticulous approach ensures that investments meet the stricter financial covenants imposed by current lending conditions.

Investment Strategy & Risk Management

In the dynamic real estate landscape of 2026, investors must be astute in their market timing and opportunity identification. The post-pandemic recovery has led to fluctuating demand, and with interest rates showing signs of stabilization, strategically timing acquisitions is crucial. Investors should remain vigilant for opportunities in transitional neighborhoods where property values have not yet peaked. A focus on pre-emptive acquisitions before anticipated interest shifts can yield significant returns. Additionally, leveraging data-driven market analyses to identify emerging trends and undervalued areas will enhance the identification of lucrative opportunities.

Risk management in the current environment requires a nuanced approach given the uncertainties in interest rates and potential economic fluctuations. Investors should brace for volatility by diversifying across asset classes and geographies. Implementing risk mitigation strategies such as maintaining higher liquidity reserves and securing fixed-rate financing options can shield against market downturns. Enhancing due diligence processes, particularly concerning tenant quality and property condition, is essential to minimize exposure to unforeseen risks.

Adjusting acquisition criteria and underwriting standards in light of these market conditions involves a more conservative approach. Investors need to stress-test assumptions, particularly regarding **rent growth** and **cap rate** targets, to ensure investments remain viable under adverse scenarios. Underwriting should incorporate a **DSCR cushion** of at least 1.25 to safeguard against fluctuations in rental income. Additionally, acquisition criteria should prioritize properties with strong **cash-on-cash returns**, aiming for a minimum threshold of 8% to justify the investment risk.

For Prime Property Funding, aligning financing products with these strategies can enhance client satisfaction and retention. Offering flexible draw schedules and emphasizing bridge financing solutions with defined exit strategies can provide investors with the agility needed in this market. By adopting these strategies, investors can navigate the challenging landscape with increased confidence.

Key Considerations for Investors

- Prioritize **fix-and-flip** properties with clear value-add potential and set aside at least 10% of the project budget for **contingency planning** to cover unexpected costs.

- Aim for a **cap rate** of at least 6% for **buy-and-hold** properties in suburban markets, adjusting for urban properties where higher appreciation potential exists.

- Incorporate a **DSCR cushion** of 1.25 or higher to ensure stability in rental income amidst potential economic fluctuations.

- Ensure **cash-on-cash returns** of at least 8% to justify the investment risk, accounting for both current income and appreciation potential.

- Leverage **bridge financing** with fixed rates to mitigate the risk of rising interest rates, and maintain a **contingency reserve** of 5-10% to manage unexpected costs.

- Identify **acquisition opportunities** in markets with high growth potential but manageable **holding costs**, such as emerging suburban areas experiencing demographic shifts.

- Focus on geographic markets offering the best **risk-adjusted returns**, such as cities with strong job growth and infrastructure development.

- Implement **conservative underwriting** practices by stress testing rent growth assumptions and market value projections to withstand economic uncertainties.

- Diversify the investment **portfolio** by balancing asset classes (residential vs. commercial) and geographic locations to reduce overall risk.

- Strengthen **risk mitigation** strategies by maintaining reserves equivalent to three months of operating expenses and ensuring comprehensive insurance coverage is in place.

Embrace these strategies with a proactive mindset, and seize the opportunities that align with your investment goals. By remaining informed and adaptable, investors can confidently navigate the evolving real estate market landscape of 2026.

Resources

External References

Disclaimer: This market analysis is for informational purposes only and should not be considered financial or investment advice. Market conditions can change rapidly. Consult with a qualified financial or lending professional before making any decisions.