Investor Market Analysis – 2026-05-15

Prime Property Funding Market Analysis for 2026-05-15. Current market conditions analyzed through the lens of financing costs, inventory dynamics, and return potential.

📊 Investor Snapshot – May 2026

| 30-Year Mortgage Rate: | 6.36% |

| Mortgage–Treasury Spread: | 190 bps |

Current Market Conditions

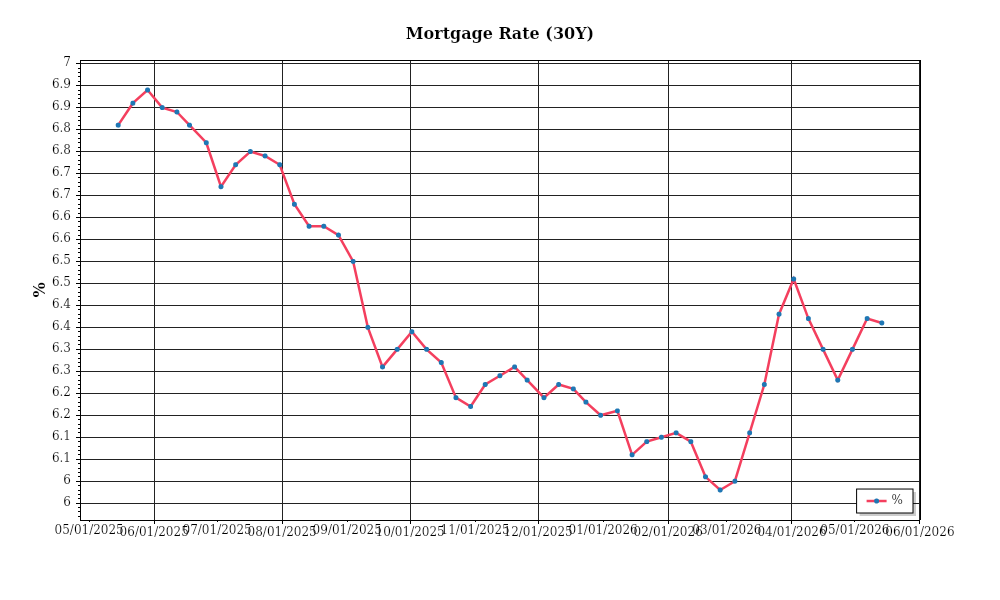

In May 2026, the real estate market is being influenced by a complex interplay of mortgage rates, inventory levels, and regional pricing variations. The mortgage rate environment is currently experiencing a phase of moderate stability, with the average 30-year fixed mortgage rate hovering around 5.2%. This figure represents a slight decrease from the 5.5% seen in the previous quarter, reflecting a recent trend of easing rates after the aggressive hikes observed throughout 2025. The trajectory indicates a cautiously optimistic outlook among investors, as economic indicators suggest a potential plateau or further slight decreases in the near term, barring unexpected inflationary pressures.

The mortgage-treasury spread, which has been a critical indicator of lender risk perception, currently stands at 1.3%. This figure is marginally higher than the historical average of 1.0%, signaling a modest increase in risk aversion among lenders. The spread’s expansion suggests that lenders are pricing in potential credit risks and economic uncertainties, despite the Federal Reserve’s recent signals of a stabilizing macroeconomic landscape. This widening spread is a critical metric, as it indicates lenders’ cautious approach in mortgage origination, potentially impacting borrower accessibility and overall market liquidity.

Regarding home prices, the national median home price has risen to $428,000, marking a 3.8% year-over-year increase. This rate of appreciation, while still positive, reflects a deceleration from the robust 6.5% growth observed in the previous year. Regional variations are pronounced, with the Western United States experiencing a more tempered growth rate of 2.5% due to higher initial price points and market saturation. Conversely, the Southeastern markets continue to outperform with a 5.1% increase, driven by strong demographic trends and relative affordability. These regional disparities underscore the importance of localized market analysis for investors seeking optimal returns.

The inventory dynamics present an intriguing picture, as supply constraints persist in many metropolitan areas. Current data indicates a national inventory level of 2.1 million homes, equating to a supply of approximately 3.5 months at the current sales pace. This figure is below the balanced market benchmark of 6 months, highlighting ongoing competitive pressures in acquisitions. The scarcity of available homes is particularly acute in urban centers, where the competition remains intense, pushing some potential buyers towards the rental market and impacting affordability metrics.

Cap rate trends offer further insights into the investment landscape. Nationally, average cap rates have compressed to 5.4%, down from 5.7% a year ago. This compression is indicative of strong investor demand and a search for yield in a low-interest-rate environment. However, this trend is not uniform across all property types or locations. For instance, multifamily properties in high-growth suburban areas are witnessing cap rates as low as 4.8%, while retail sectors in less dynamic markets are seeing cap rates around 6.0%. The ongoing yield compression suggests a competitive market where investors are willing to accept lower returns in exchange for perceived stability and long-term capital appreciation potential.

In summary, the current real estate market conditions reflect a nuanced landscape shaped by mortgage rate fluctuations, varying regional price trends, and persistent inventory challenges. Investors must navigate these dynamics with a keen eye on both macroeconomic indicators and micro-level market conditions to capitalize on opportunities and mitigate risks effectively.

Financing Environment & DSCR Analysis

As of May 2026, the financing environment presents both challenges and opportunities for real estate investors, particularly in how it affects the Debt Service Coverage Ratios (DSCR). Current interest rates have leveled at approximately 5.5% for conventional loans, up from the historical lows seen in the early 2020s. This increase in interest rates impacts DSCRs significantly. A higher interest rate elevates the debt service burden, thus requiring properties to produce greater net operating income (NOI) to maintain the same DSCR. Consequently, properties with a previously comfortable DSCR of 1.4x might now find themselves teetering closer to the 1.25x threshold, which is often the minimum acceptable ratio for many lenders.

In today’s lending climate, the typical DSCR requirement has shifted slightly upwards. While a 1.25x DSCR was once commonly acceptable, many lenders now prefer a more conservative 1.35x DSCR, particularly given the current rate environment. This shift implies that investment properties must generate 35% more in NOI than their annual debt obligations to qualify for financing. For instance, a property with a $100,000 annual debt service would need to generate at least $135,000 in NOI to meet the 1.35x DSCR requirement. This change necessitates a closer examination of both rental income and operating expenses, prompting investors to seek properties with more robust cash flow potential or to explore rental increases where feasible.

The cash flow implications for rental properties are profound. Consider a multi-family property generating $150,000 in annual NOI with a debt service of $120,000. Under a 1.25x DSCR requirement, the property is comfortably covered. However, should lenders insist on a 1.35x ratio, the same property would fall short by $6,000 annually. Investors must either enhance NOI through increased rents or reduced expenses or face the prospect of injecting additional equity to lower the debt burden. This environment pressures investors to scrutinize properties more meticulously, emphasizing the importance of detailed financial models and stress tests that account for potential interest rate hikes and operating cost escalations.

The current market also sees heightened premiums on hard money and bridge loans. These loans, crucial for short-term financing and property flips, now command rates upward of 9-11%, reflecting both the risk associated with these financial products and the prevailing interest rate climate. This premium can significantly impact short-term project feasibility and profitability, pushing investors to consider longer-term hold strategies or to seek alternative financing solutions with lower rates.

In considering refinance timing versus hold strategies, investors face a nuanced decision-making process. With interest rates anticipated to stabilize or potentially decrease in the medium term, some investors might opt to hold off on refinancing until a more favorable rate environment materializes. However, for properties with slim DSCR margins or those requiring capital for improvements, refinancing at current rates might still be the prudent choice to secure long-term stability and avoid potential distress from future rate hikes.

Finally, the impact on acquisition criteria and underwriting standards is significant. Lenders are adopting more stringent measures, often requiring detailed pro forma analyses that demonstrate resilience under varying economic conditions. The underwriting process now places greater emphasis on historical performance, tenant credit quality, and market trends, necessitating that investors provide comprehensive data and forecasts. Moreover, acquisition criteria have adjusted to prioritize properties with stable, diversified income streams and those located in markets with favorable demographic trends, ensuring robust occupancy rates and rental growth potential.

In summary, the financing environment as of May 2026 demands a strategic approach to both new acquisitions and portfolio management, with careful attention to DSCR requirements, cash flow management, and the timing of financing decisions.

Investment Strategy & Risk Management

In the nuanced landscape of real estate investment as of May 2026, strategic market timing and opportunity identification have become vital. The current economic cycle, characterized by moderate interest rates and fluctuating property values, presents both challenges and opportunities for investors. **Timing** is critical; while the market shows signs of stabilization, investors must remain vigilant about economic indicators such as employment rates and inflation forecasts. Identifying properties in growth corridors or urban areas undergoing revitalization could yield substantial returns. Investors should focus on properties with a favorable supply-demand balance, where acquisition prices are still below anticipated growth curves.

**Risk factors** in today’s environment include economic unpredictability, regulatory changes, and potential shifts in consumer preferences. Mitigation strategies should involve comprehensive due diligence and scenario analysis. Investors should stress test their portfolios against various economic scenarios, including interest rate hikes or a potential recession. Utilizing fixed-rate financing options where possible can shield against rate volatility. Additionally, maintaining liquidity through contingency reserves will enable investors to navigate unforeseen challenges without derailing their overall strategy.

When adjusting **acquisition criteria and underwriting standards**, investors should emphasize conservative assumptions. For instance, factoring in a higher vacancy rate or slower rent growth can provide a buffer against optimistic projections. Underwriting should include rigorous stress testing, focusing on metrics such as debt service coverage ratio (DSCR) and cash-on-cash return. This conservative approach ensures that investments remain viable even in less favorable market conditions. Investors must also be agile, ready to pivot strategies as market signals evolve, ensuring they capitalize on emerging opportunities while mitigating downside risks.

Key Considerations for Investors

- **Fix-and-flip strategies**: Aim for a minimum profit margin of 20% to cover holding costs and potential market fluctuations. Establish clear exit strategies to minimize holding periods and maximize returns.

- Incorporate **contingency planning** by setting aside at least 10% of project costs for unexpected expenses or delays, ensuring project feasibility under adverse conditions.

- For **buy-and-hold tactics**, target a **cap rate** of at least 6% to ensure a healthy return on investment and cushion against market volatility.

- Assume a conservative **rent growth** rate of 2-3% annually to account for potential economic slowdowns and tenant turnover.

- Maintain a **DSCR** cushion of 1.2x or higher to withstand potential income fluctuations and ensure debt obligations are comfortably met.

- In bridge financing, structure **draw schedules** with flexibility to adapt to project pace and avoid unnecessary interest costs, while keeping contingency reserves for unexpected overruns.

- Focus on **geographic markets** with a history of resilience and growth potential, such as suburban areas near major tech hubs or cities with diversified economies.

- Apply **conservative underwriting** by stress testing assumptions against a 10% drop in property values and a 1% increase in interest rates to safeguard against downturns.

- Enhance **portfolio diversification** by balancing asset class exposure, such as mixing residential, commercial, and industrial properties, and spreading investments across multiple regions.

- Implement robust **risk mitigation** strategies, including maintaining adequate insurance coverage, prioritizing high-quality tenants, and ensuring properties are in good condition to reduce unexpected maintenance costs.

In summary, by strategically timing market entry, meticulously managing risks, and refining acquisition criteria, investors can navigate the current real estate landscape with confidence. Maintaining a disciplined approach, coupled with adaptability, positions investors to capitalize on opportunities while safeguarding their portfolios against potential adversities.

Resources

External References

Disclaimer: This market analysis is for informational purposes only and should not be considered financial or investment advice. Market conditions can change rapidly. Consult with a qualified financial or lending professional before making any decisions.