Investor Market Analysis – 2026-05-12

Prime Property Funding Market Analysis for 2026-05-12. Current market conditions analyzed through the lens of financing costs, inventory dynamics, and return potential.

📊 Investor Snapshot – May 2026

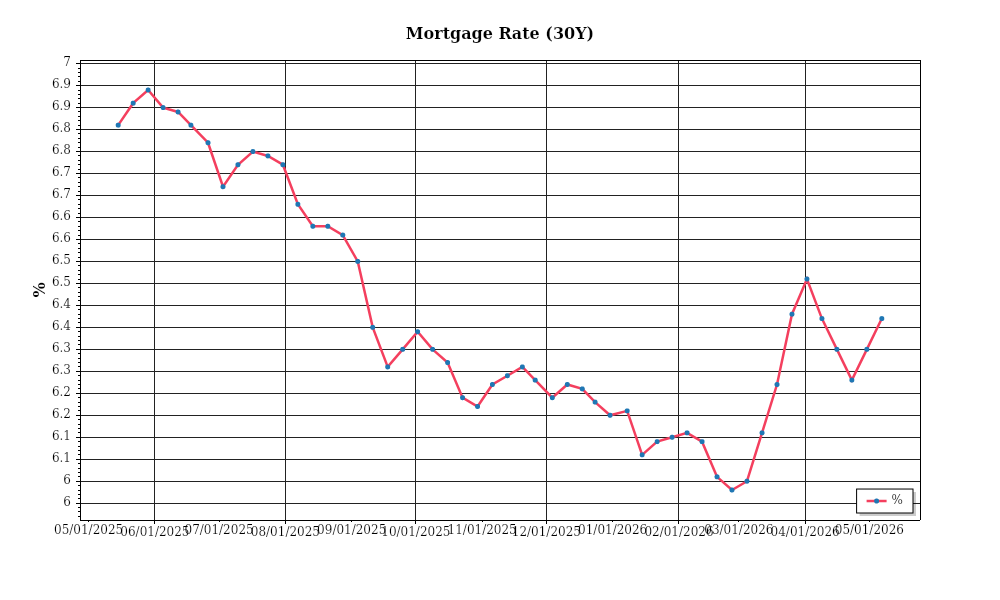

| 30-Year Mortgage Rate: | 6.37% |

| Mortgage–Treasury Spread: | 199 bps |

Current Market Conditions

As of May 2026, the real estate market is navigating through a complex landscape characterized by fluctuating mortgage rates, variable home price trends, and shifting inventory dynamics. The current mortgage rate environment is a critical factor influencing market activity. The average 30-year fixed mortgage rate stands at 5.2%, reflecting a subtle increase from 4.9% recorded in January 2026. This upward trend is primarily driven by the Federal Reserve’s monetary policy adjustments aimed at curbing inflation, which has hovered around 3.8% annually. The trajectory of mortgage rates appears to be slightly upward, with the possibility of reaching the 5.5% threshold by the end of the year, contingent on further economic indicators. This environment suggests a moderation in borrowing costs compared to the previous year when rates averaged 3.7%, thereby impacting buyer affordability and potentially cooling overheated markets.

The spread between mortgage rates and 10-year U.S. Treasury yields has recently widened to 2.3%, up from 2.0% earlier in the year. This spread is an essential indicator of lender risk perception and the premium investors demand for holding mortgage-backed securities over relatively risk-free government bonds. The widening spread suggests increased economic uncertainty and heightened risk aversion among lenders, possibly due to geopolitical tensions and volatile global markets. Such a trend could indicate tighter lending standards and a more cautious approach by financial institutions, potentially leading to a further slowdown in mortgage origination volumes.

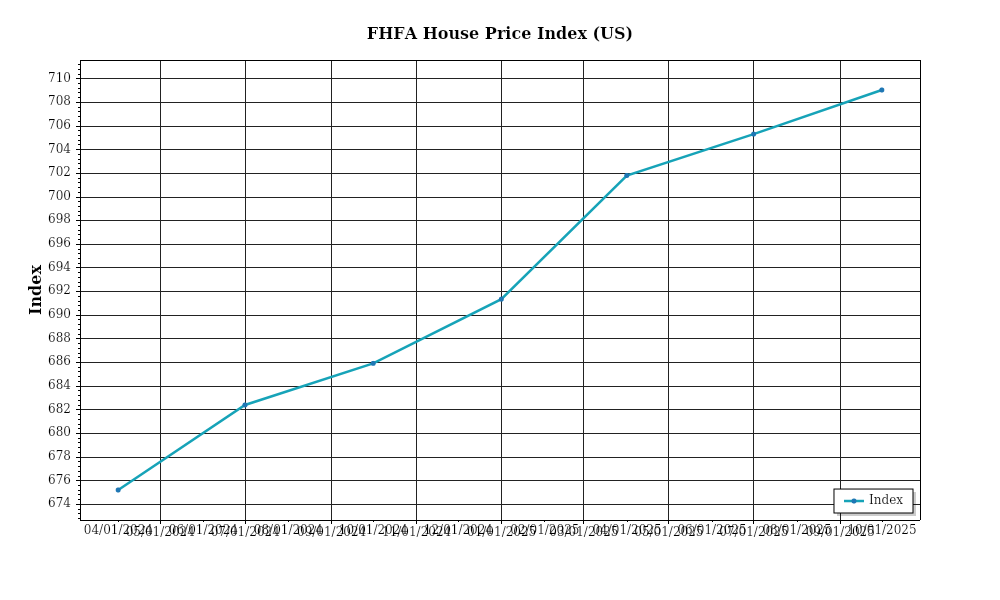

Turning to home price trends, the national median home price has reached $426,000, marking a 4.5% year-over-year appreciation rate. However, this figure represents a deceleration from the double-digit growth rates observed in the previous two years. Regional variations are notable; the Sun Belt states, such as Florida and Texas, continue to experience robust demand and price growth, with median prices climbing by 6.8% and 7.2%, respectively. Conversely, markets in the Northeast, particularly New York and New Jersey, show signs of stagnation, with prices rising by a modest 2.1%. This disparity underscores the influence of migration patterns and remote work trends, which continue to shape regional real estate dynamics.

Inventory levels remain a critical factor in assessing market balance. The current inventory of unsold homes is approximately 1.3 million units, equivalent to a 3.4-month supply at the current sales pace. This figure is indicative of a seller’s market, albeit less severe than the 2.1-month supply recorded during the pandemic-driven housing boom. Competition for acquisitions remains fierce, particularly in desirable suburban markets, where multiple offers and bidding wars are still common. However, there is a gradual increase in new listings, suggesting a slow rebalancing and potential easing of upward price pressures as more sellers enter the market.

Cap rate trends provide additional insights into the real estate investment landscape. The national average cap rate for commercial properties has compressed to 5.1%, down from 5.4% at the beginning of the year. This compression reflects sustained investor demand amidst limited supply and historically low interest rates. However, the ongoing rise in borrowing costs could prompt a gradual expansion of cap rates if property values do not keep pace with interest rate increases. Such a shift could alter yield expectations and investment strategies, particularly in markets where cap rates have reached historic lows.

Overall, the current market conditions present a nuanced picture characterized by rising interest rates, regional price disparities, and competitive inventory dynamics. While these factors suggest a moderation in market activity, investor sentiment remains cautiously optimistic, driven by a resilient economy and underlying demand fundamentals.

Financing Environment & DSCR Analysis

The current interest rate environment as of May 2026 presents a unique set of challenges and opportunities for real estate investors, particularly in relation to debt service coverage ratios (DSCR). With prevailing rates hovering around 6.5% for conventional loans, the impact on DSCRs is significant. Higher interest rates increase monthly debt obligations for borrowers, thereby reducing the DSCR. For instance, a property generating a net operating income (NOI) of $120,000 annually with a loan carrying an annual debt service of $100,000 would achieve a DSCR of 1.20x. However, with the current rate hike, the annual debt service might rise to $110,000, lowering the DSCR to approximately 1.09x. This decrease challenges investors to either increase property income or reduce expenses to maintain lender-required DSCR levels.

In today’s market, lenders are increasingly adopting stricter DSCR requirements, often demanding a minimum of 1.35x compared to the pre-pandemic standard of 1.25x. This shift reflects lenders’ heightened risk aversion in the face of economic uncertainties and inflationary pressures. For an investor to meet a 1.35x DSCR on the same property example, the NOI would need to increase to $148,500, assuming the same debt service cost. Investors must, therefore, strategize on enhancing property income, either through rental increases or operational efficiencies, to satisfy these more stringent requirements.

Cash flow implications for rental properties are profound under these conditions. Consider a multifamily property with a monthly gross rental income of $15,000. If operating expenses are $5,000, the NOI stands at $10,000. Assume a monthly debt service of $8,000, resulting in a DSCR of 1.25x. If rates drive the debt service up to $9,000, the DSCR drops to 1.11x, below the acceptable threshold. This scenario compels investors to either boost rental income through market adjustments or explore value-add renovations to increase property appeal and justify higher rents. Alternatively, reducing operational costs could also aid in realigning the DSCR to acceptable levels.

Beyond conventional financing, the current market conditions are also affecting hard money and bridge loan rate premiums. These loans, often used for short-term financing during property acquisitions or renovations, carry interest rates approximately 3-5% higher than conventional loans, with current rates ranging from 9.5% to 12%. The premium reflects the higher risk and shorter loan durations associated with these financial products. For investors considering such options, the increased cost must be weighed against potential property appreciation or income gain post-renovation or market repositioning.

Given the current rate environment, investors face critical decisions regarding refinance timing versus hold strategies. With predictions suggesting potential rate stabilization or even reductions in the next 12-18 months, some investors may opt to hold their current financing arrangements, especially if locked in at lower rates. Others may consider refinancing to access equity or improve cash flow despite potential rate hikes, if longer-term savings are anticipated. A strategic evaluation of market trends and property performance projections is essential to making informed decisions.

Finally, these financial dynamics significantly impact acquisition criteria and underwriting standards. The heightened DSCR requirements, coupled with increased borrowing costs, necessitate more conservative purchase price offers and stricter underwriting standards. Properties must demonstrate robust and sustainable cash flows to qualify for financing. Investors must perform rigorous due diligence, focusing on market trends, rental demand, and expense management to ensure property acquisitions align with adjusted financial benchmarks in this evolving landscape.

## Investment Strategy & Risk Management

In the current market environment, strategic timing and opportunity identification are crucial for maximizing returns in real estate investments. As of May 2026, the real estate market exhibits cyclical patterns that savvy investors must navigate carefully. Investors should consider the potential for price corrections in overheated markets while also identifying undervalued properties in emerging areas. The key is to leverage data analytics and local market insights to time acquisitions during periods of low demand and capitalize on lower purchase prices and financing costs. Monitoring economic indicators, such as employment rates and consumer spending, can help predict market shifts and optimize entry and exit points.

Risk factors in the current environment include rising interest rates, inflationary pressures, and regulatory shifts. To mitigate these risks, it is essential to adopt a robust risk management strategy. Investors should stress-test their portfolios against various economic scenarios, ensuring that properties can withstand adverse conditions. Implementing hedging strategies, such as interest rate swaps or caps, can protect against rate hikes. Additionally, maintaining liquidity through contingency reserves will provide a buffer against unexpected expenses and market volatility. Diversifying investments across asset classes and regions also reduces exposure to localized downturns.

Adjusting acquisition criteria and underwriting standards is imperative in this environment. Investors should prioritize properties with strong fundamentals, including location, tenant quality, and potential for value-add improvements. Underwriting should incorporate conservative assumptions regarding rent growth and vacancy rates, with a focus on maintaining healthy debt service coverage ratios (DSCR). Employing a rigorous due diligence process to assess property condition and market dynamics will further safeguard investments. By taking a disciplined approach, investors can enhance their ability to identify properties that offer the best risk-adjusted returns.

Prime Property Funding positions itself as a leader in providing tailored financing solutions for real estate investors. By aligning strategies with current market conditions, investors can capitalize on opportunities while mitigating inherent risks. Confidence in decision-making arises from a deep understanding of market dynamics and a commitment to rigorous analysis and prudent management practices. With the right strategies, investors can navigate the complexities of the 2026 real estate market, achieving both growth and stability in their portfolios.

### Key Considerations for Investors

– **Fix-and-flip strategies**: Maintain **holding costs** below 10% of the project’s total budget to ensure profitability even during delays. Aim for a **spread** of at least 30% between purchase and expected resale price.

– **Exit timing**: Plan for property dispositions in Q2 or Q4, aligning with seasonal market upticks to maximize sale prices.

– **Buy-and-hold tactics**: Target properties with a **cap rate** exceeding 6% in stable markets and 7% in emerging markets to secure favorable returns.

– **Rent growth assumptions**: Use a conservative annual **rent growth** estimate of 3% to account for economic fluctuations.

– **DSCR cushions**: Ensure a minimum **DSCR** of 1.25 to provide a buffer against potential income disruptions.

– **Bridge financing**: Negotiate **draw schedules** that align with project milestones to optimize cash flow and reduce interest expenses.

– **Exit strategies**: Develop multiple exit strategies, including refinancing and sale, to provide flexibility in changing market conditions.

– **Geographic focus**: Invest in secondary markets with robust economic growth, focusing on areas with population growth exceeding 2% annually.

– **Conservative underwriting**: Incorporate **stress testing** for vacancy rates of up to 10% in underwriting to anticipate potential downturns.

– **Portfolio diversification**: Balance your portfolio with a mix of **asset classes** and geographic locations to mitigate localized risks and capitalize on diversified growth.

By employing these strategies, investors can confidently navigate the evolving real estate landscape, leveraging Prime Property Funding’s expertise to achieve success.

Resources

External References

Disclaimer: This market analysis is for informational purposes only and should not be considered financial or investment advice. Market conditions can change rapidly. Consult with a qualified financial or lending professional before making any decisions.